Risk appetite improved during the US session following a report that the Fed is considering whether to adopt a wait-and-see stance after hiking at its upcoming meeting. Oil prices slid yesterday after Saudi Energy Minister said that a cut of 1mn bpd would be enough. As for today, besides headlines surrounding the OPEC meeting, investors are likely to pay attention to the US jobs data as well.

Risk Sentiment Improves, Oil Slides as OPEC Decision Looms

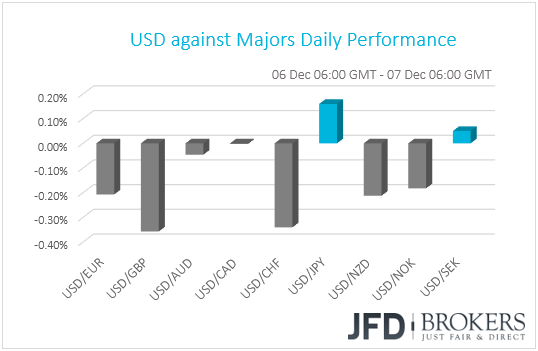

The dollar traded lower against most of the other G10 currencies yesterday. It lost the most ground against GBP, CHF and NZD, while it gained only against JPY. The greenback traded virtually unchanged against AUD, CAD, SEK.

Although not so clear by the FX market performance, the broader market sentiment switched back to ‘risk on’ at some point yesterday. The safe-haven JPY traded on the back foot, but CHF was among the main gainers. The NZD dollar managed to outperform its US counterpart, but the other commodity-linked currencies, AUD and CAD, failed to do so. This may have been due to individual stories weighing on these currencies (see below).

The change in market sentiment was more evident by the performance of the equity markets. Major EU equity indices closed again in negative territory as the arrest of Huawei’s CFO may have kept investors concerned over fresh tensions between US and China. US indices opened well in the red as well but rebounded and closed well off their lows after the Wall Street Journal reported that Fed officials are considering whether to adopt a wait-and-see approach after possibly raising interest rates at their upcoming gathering. Both the S&P 500 and Dow Jones closed slightly in the red, while Nasdaq managed to end the US session in positive territory.

Back to the currencies, the Australian dollar came under some selling interest after the RBA Deputy Governor Guy Debelle said that although the next move in monetary policy is more likely to be up than down, such a move is still some way off. Even though this is something the market agrees with, Debelle also suggested that there is “still scope for further reduction in the policy rate” should the economic outlook deteriorates. Following the somewhat upbeat tone in Tuesday’s RBA meeting statement, the talk over a rate cut may have come as a disappointment to AUD-traders and thus the Aussie slid on the remarks. That said, the currency rebounded later in the day to finish virtually unchanged against the greenback.

The Canadian dollar also failed to gain against its neighboring dollar, perhaps due to a combination of a dovish BoC on Wednesday as well as the slide in oil prices yesterday. Oil prices came under selling interest following comments by Saudi Energy Minister Khalid al-Falih, who said he hoped that members could conclude something by the end of Friday. He also noted that "If everybody is not willing to join and contribute equally, we will wait until they are." With regards to the amount that could be agreed, he noted that options include cuts of 500k to 1.5mn bpd, but he added that 1mn bpd would be enough.

OPEC’s decision to wait for Russia to join discussions today, as well as talks around a cut of 1mn bpd may have disappointed investors, who, up until yesterday, had the 1mn figure as their lower end of their expectations range. Investors are likely to stay on guard today, awaiting to see whether Russia will join any accord, and if so, what will be the amount of the agreed cut. Given that the consensus may now have changed to 1mn bpd, anything above that may prove supportive for oil prices. On the other hand, a smaller cut could disappoint further, and prices are likely to extend their slide. Still, the big letdown would be no cuts at all, which could cause oil prices to fall sharply.

Brent Oil – Technical Outlook

Brent oil traded lower yesterday, breaking below the support (now turned into resistance) territory of 60.90. However, the slide was stopped slightly above the 58.00 barrier, and then the price rebounded again. The black liquid continues to trade below the short-term downtrend line taken from the peak of the 9th of October, which, at least from a technical standpoint, keeps the near-term outlook negative. However, as we noted yesterday, bearing in mind that the upcoming directional move is likely to depend on the OPEC+ outcome, we prefer to adopt a neutral stance for now.

A below-consensus production cut by OPEC and its allies could encourage the bears to push the price below the key support zone of 58.00 and perhaps aim for the psychological zone of 55.00, also marked by the low of the 6th of October 2017. Another dip below that level could extend the slide towards the low of the 9th of September last year, at around 53.00. Now, in case producers decide not to cut output, Brent could slide below those levels.

On the other hand, a more-than-anticipated cut may wake up the bulls, who could start driving the battle higher. However, we would like to see a clear break above the 64.75 zone before we start examining the case of a near-term trend reversal. Such a move may confirm the break above the aforementioned trendline and could pave the way for the 67.80 zone, the break of which could trigger extensions towards 69.30.

US Employment Report Enters the Limelight

Apart from headlines surrounding the OPEC gathering, today, market participants are likely to focus on the US employment data for November as well. Expectations are for NFPs to have risen 200k, which is less than October’s 250k, but still a decent number consistent with further tightening of the labor market. Yesterday, the ADP figure came in below expectations, which may have raised some speculation that the NFP may miss its forecast as well. That said, we repeat once again that the correlation between the two time-series at the time of the release has been very low in recent years. Thus, we would not pay much emphasis on the ADP print.

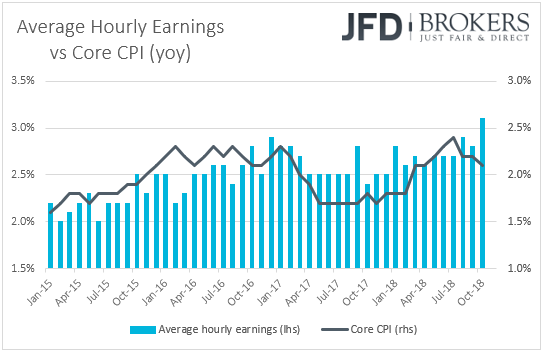

The unemployment is expected to stay at 3.7%, its lowest since 1969, while average hourly earnings are anticipated to have accelerated somewhat on a monthly basis, to +0.3% mom from +0.2%. Barring any revisions to the prior prints, this is likely to keep the yoy rate unchanged at +3.1%. Overall, the forecasts point to a strong report, with wage growth suggesting that inflation could still accelerate in the months to come, at least in core terms. The headline figure may be weighed down by the slide in oil prices.

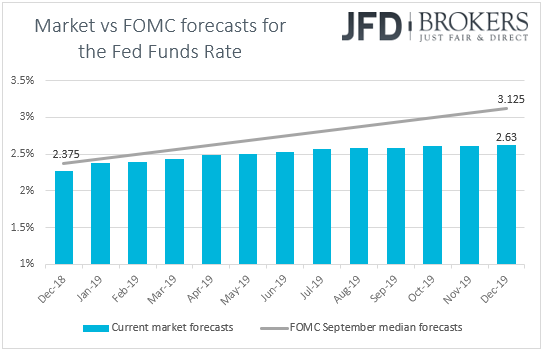

Last week, Fed chair Powell’s dovish remarks prompted market participants to price out their expectations with regards to the number of interest rate hikes the Fed may deliver next year, despite staying overly optimistic that a December move remains firmly on the cards. The minutes of the latest FOMC meeting confirmed investors’ choice, with a few participants expressing uncertainty about the timing of future rate increases, and many arguing for placing more emphasis on the evaluation of incoming data. Yesterday’s Wall Street Journal report encouraged investors to push further back their rate path expectations. According to the Fed fund futures, the market now assigns an 75 chance for a December hike, but sees only 1 hike throughout 2019. A few weeks ago, that number was around 2.

Thus, although a strong employment report could push that number slightly higher and thereby support the dollar, we see it highly unlikely for investors to revive expectations of 2 hikes in 2019. The big question is: How many hikes will the new “dot plot” reveal at the upcoming Fed meeting? The September plot suggested 3 rate increases next year, but this seems as a very unlikely case now. Will the new one matches market expectations of 1 hike, or will we see just a downside revision to 2? The first case is likely to confirm further investors’ view, supporting further equity markets and bringing the dollar under renewed selling interest. On the other hand, although still a downside revision, projections of 2 hikes in 2019 would still be well above market consensus and may result in the opposite market reaction.

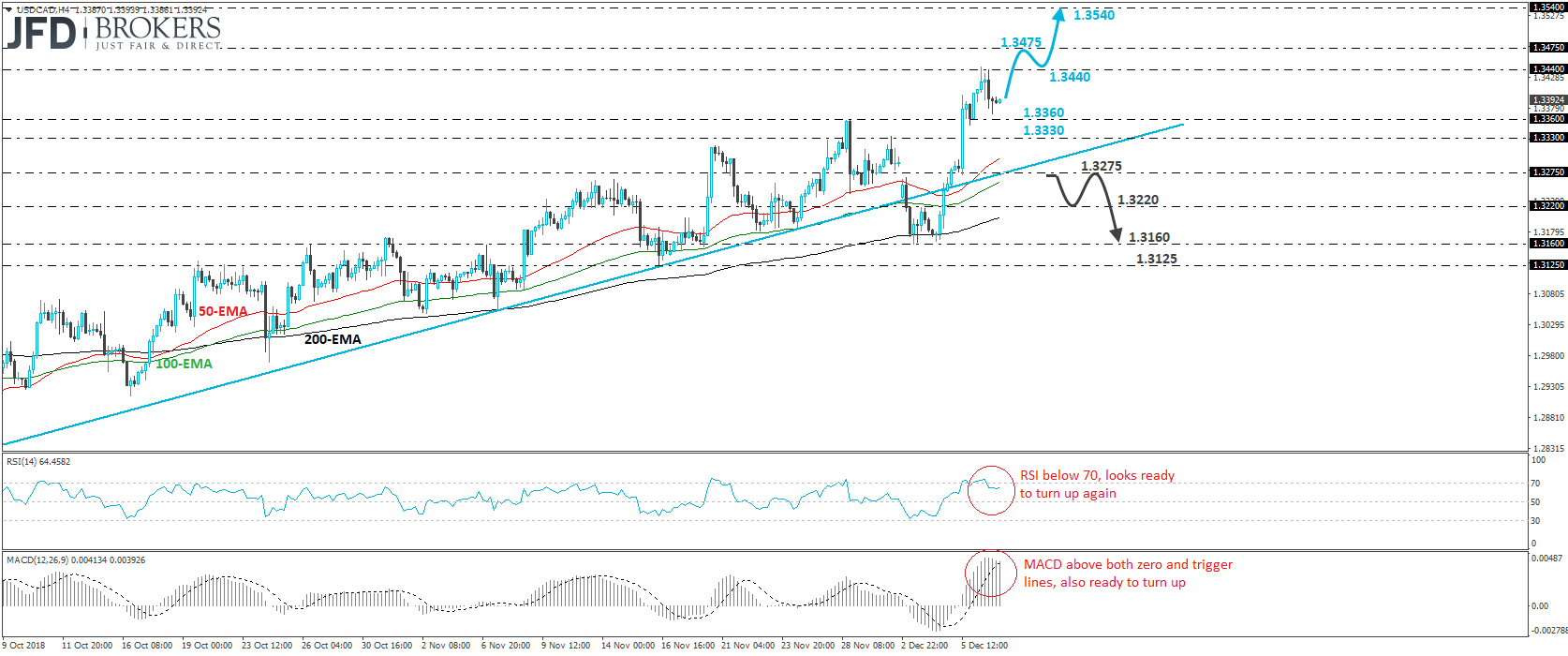

USD/CAD – Technical Outlook

USD/CAD skyrocketed on Wednesday following the dovish switch by the BoC, breaking two resistance (now turned into support) barriers in a row. The pair continued drifting north yesterday as well but hit resistance near 1.3440 and pulled back. On Tuesday, the pair emerged back above the uptrend line drawn from the low of the 1st of October, while Wednesday’s rally confirmed a forthcoming higher high on both the 4-hour and daily charts. In our view, these moves have changed the near-term picture back to a positive one.

If the bulls are strong enough to take the reins again soon, then we may see them aiming for another test near 1.3440, the break of which could extend the recovery towards the peak of the 12th of June 2017, at around 1.3475. Another break above 1.3475 may set the stage towards the 1.3540 area, defined by the highs of the 2nd and 8th of June last year.

Looking at our short-term momentum studies, we see that the RSI looks ready to turn up again, from slightly below its 70 line. The MACD lies well within its positive zone and, although it topped yesterday, it appears ready to turn north as well, from fractionally above its trigger line. These indicators support somewhat the case for USD/CAD to stage another positive leg in the short run.

On the downside, we would like to see a clear move below 1.3275 before we start examining whether the bulls have abandoned the battlefield. Such a dip could signal another break below the aforementioned uptrend line and may pave the way for the 1.3220 hurdle, defined by an intraday inside swing high formed on Monday. Another break below 1.3220 could open the path for the 1.3160 area, near the Monday’s and Tuesday’s lows.

As for the Rest of Today’s Events

Besides the US jobs data, we get employment numbers from Canada as well. Expectations are for the unemployment rate to have held steady at 5.8%, while the forecast of the net employment change has changed and now suggests that that the economy has gained slightly less jobs than in October (10.3k vs 11.2k). Following the dovish switch by the BoC, even if we see a somewhat better-than-expected report, we doubt that CAD-traders will be encouraged to place their January-hike bets back on the table. We expect them to stay focused on headlines surrounding the OPEC+ meeting in Vienna.

As for other data, we have Eurozone’s employment change data for Q3, as well as the bloc's final GDP print for the same quarter. In the US, the preliminary UoM consumer sentiment index for December is also coming out and is expected to decline to 97.1 from 97.5.

We also have one speaker on today’s agenda: Fed Board Governor Lael Brainard.

As for tonight, during the Asian morning Saturday, China’s trade balance for November is released. The forecasts suggest that the nation’s trade surplus increased to USD 36.2bn from 34.0bn, but both exports and imports are anticipated to have slowed on a yoy basis.

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.