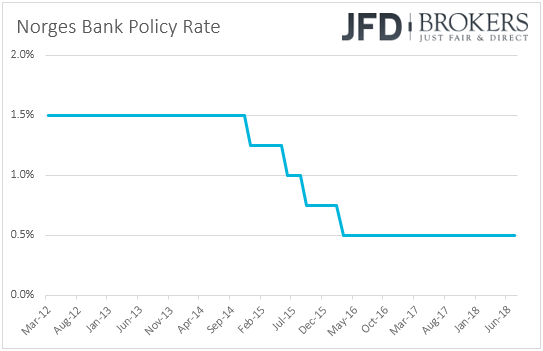

This week, we have only one central bank deciding on monetary policy: the Norges Bank. Expectations are for the Bank to keep interest rates unchanged, but to keep the door wide open for a hike in September. In the UK, we get jobs, inflation and retail sales data. We get inflation figures from Canada as well.

Monday appears to be a relatively quiet day as no major events or indicators are on the agenda.

On Tuesday, during the Asian morning, we get China’s fixed asset investment, retail sales and industrial production, all for July. Expectations are for fixed asset investment to have risen 6.0%, the same pace as in June, while both industrial production and retail sales are expected to have accelerated to +6.3% yoy and 9.2% yoy, from 6.0% and 9.0% respectively.

During the European morning, Germany’s final CPIs for July, the nation’s preliminary GDP for Q2, as well as the ZEW survey for August are coming out. The final inflation prints are expected to confirm the preliminary estimates, while the preliminary growth estimate is expected to show that Eurozone’s largest economy accelerated to +0.4% qoq in Q2 from +0.3% in Q1. As far as the ZEW survey is concerned, the current conditions index is forecast to have ticked down to 72.3 from 72.4, while the expectations one is anticipated to have risen to -20.1 from 24.7.

We get GDP data from the Eurozone as a whole as well. Specifically, the 2nd estimate of the bloc’s GDP for Q2 is due to be released. As it is usually the case, it is expected to confirm the 1st estimate and show that the Euro area economy slowed to +0.3% qoq from +0.4% in Q1. Eurozone’s industrial production is also due to be released.

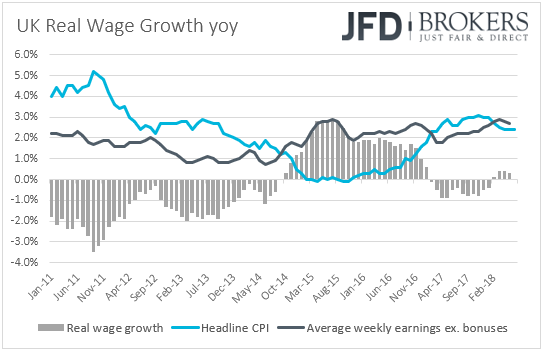

From the UK, we have the employment report for June. Expectations are for the unemployment to have remained unmoved at its 42-year low of 4.2%, while average weekly earnings, both including and excluding earnings, are expected to have risen at the same rates as in May (2.5% yoy and 2.7% yoy, respectively).

According to the IHS Markit/REC Report on Jobs for the month, inflation of salaries for permanent-placed staff held close to a three-year high, while temporary pay rates stood near their two-year peak. So, having this in mind, we see the risks surrounding the earnings forecasts as tilted to the upside.

On Wednesday, Asian time, Australia’s wage price index for Q2 is coming out. The forecasts suggest that Australian salaries accelerated to +0.6% qoq from +0.5% in Q1, which will keep the yoy rate unchanged at +2.1%. However, bearing in mind that the Labor costs sub index of the NAB business survey rose only 0.8% qoq in June, compared to 0.9% qoq in March, we believe that the risks surrounding the quarterly forecast are shifted somewhat to the downside.

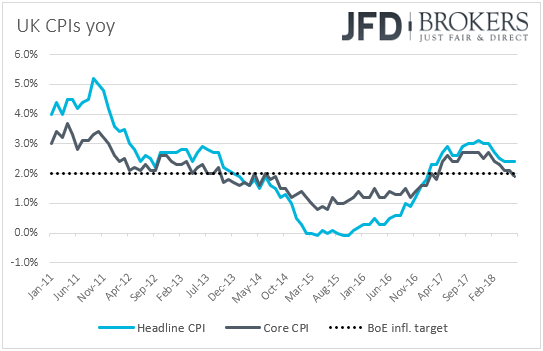

As for the European day, the UK CPI data for July are due to be released. The headline rate is expected to have ticked up to +2.5% yoy from +2.4%, while the core rate is forecast to have remained unchanged at +1.9% yoy. Although accelerating headline inflation, especially if preceded by accelerating wages on Wednesday, could help the wounded pound recover some of its recently lost ground, we doubt that it could spark speculation with regards to another BoE rate hike by the end of this year, especially if the core rate stays below the Bank’s target of 2%.

At the latest BoE meeting, policymakers decided to increase interest rates to +0.75%, but Carney’s comments at the press conference, as well as in an interview after the conference, suggested that the BoE is probably done hiking for this year. Based on the latest OIS data provided by the BoE, the market is not anticipating a full rate increase even by the end of next year. Specifically, a hike by December 2019 is around 85% priced in.

Later in the day, the US retail sales for July are due out. Expectations are for headline sales to have slowed to +0.2% mom from +0.5%, while core sales are anticipated to have risen 0.4% mom, which is the same pace as in June. The nation’s industrial and manufacturing production data for the month, as well as the Unit Labor Costs index for Q2 are also coming out.

On Thursday, during the Asian day, we have Australia’s employment report for July. Expectations are for the unemployment rate to have remained unchanged at 5.4%, while the net change in employment is expected to show that the economy gained 15k jobs during the month, compared to 51k in June.

As for the European day, the Norges Bank decides on interest rates. At their latest meeting, Norwegian policymakers decided to keep interest rates unchanged at +0.50% and noted that “the key policy rate will most likely be raised in September 2018”. On Friday, data showed that inflation accelerated more than expected in July, with the headline rate hitting +3.0% yoy and the core touching +1.4% yoy, both above the Bank’s projections for the month of +2.3% and +1.2% respectively.

That said, although inflation data is more than encouraging for Norges Bank officials, we don’t expect them to rush and hike at this meeting. After all, this will be one of the “smaller” meetings, which are not accompanied by updated economic projections and a press conference. We expect the Bank to maintain its upbeat tone and repeat that it is likely to push the hiking button in September.

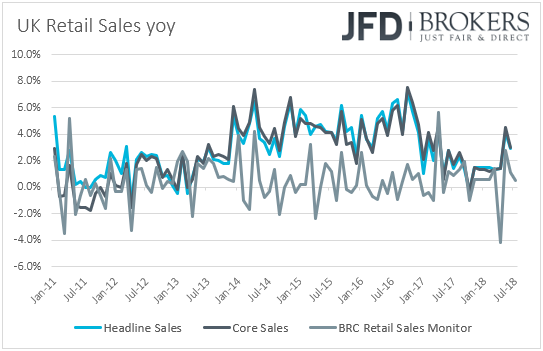

From the UK, we get retail sales for July. Expectations are for headline sales to have risen 0.2% mom after falling 0.5% in June, something that will drive the yoy rate up to +3.0% from 2.9%. Core sales are also expected to have rebounded on a monthly basis, to +0.1% mom from -0.6%. However, this will push the core yearly rate down to +2.8% from +3.0%. Bearing in mind that the BRC retail sales monitor showed that sales slowed to +0.5% from +1.1% in yearly terms, we view the risks surrounding the headline yoy rate as shifted to the downside as well.

As for the rest of Thursday’s indicators, Eurozone’s trade balance for June, as well as US building permits and housing starts for July are due to be released.

Finally, on Friday, Eurozone’s current account balance for June, as well as the bloc’s final inflation figures for July are coming out. No forecast is currently available for the current account data and as usual, the final CPI prints are expected to confirm their preliminary estimates.

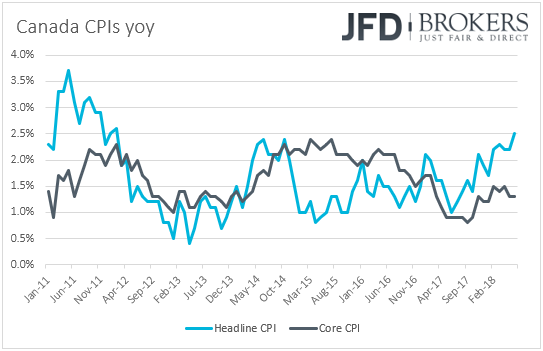

Later in the day, Canada’s inflation data for July are coming out. Expectations are for the headline rate to have ticked down to +2.4% yoy from 2.5% in June, while the core rate is forecast to have remained unchanged at +1.3% yoy. At its latest meeting, the Bank of Canada decided to raise interest rates to +1.50% from +1.25% as was expected, while in the accompanying statement officials maintain their hawkish stance, noting that they will continue to take a gradual approach on interest rates, guided by incoming data.

Since then, data have been encouraging. Headline inflation accelerated to 2.5% yoy in June from +2.2% in May, while May’s monthly growth rate jumped to +0.5% mom from +0.1%. The unemployment rate fell to 5.8% in July, while the net change in employment showed that the economy gained more jobs than it did in June. Thus, having all these in mind, even if the headline inflation rate ticks down, we don’t expect this to alter market expectations with regards to another BoC rate increase by the end of the year.

From the US, we have the preliminary UoM consumer sentiment index for August, which is expected to have risen to 98.1 from 97.9. The preliminary UoM 1- and 5-year inflation expectations for the month are also due to be released.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.