The pound remained supported yesterday after UK PM Theresa May survived the confidence vote called after her deal was defeated on Tuesday. Investors may now be eager to see what kind of a plan B May will bring back and whether MPs will support it. Elsewhere, market sentiment was somewhat hurt overnight following reports of investigations over whether Huawei has stolen trade secrets from US firms.

Pound Stays Strong After May Wins Confidence Vote

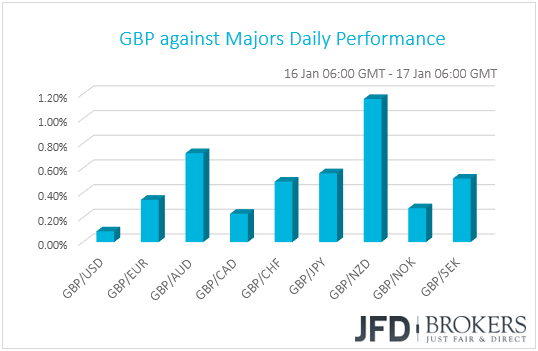

The pound traded higher against all but one of the other G10 currencies, with the dollar being the only one to resist, thereby keeping Cable virtually unchanged. The main losers were NZD, AUD and JPY in that order.

Twenty-four hours after the devastating defeat over her Brexit plan, UK Prime Minister Theresa May survived the confidence vote called after her deal was rejected. Specifically, MPs voted 325 – 306 in favor of May’s government. Just after the vote, May called lawmakers from across all the political spectrum to come together in order to reach consensus and figure out a viable plan. “Now MPs have made clear what they don’t want, we must all work constructively together to set out what parliament does want”, the PM said. That said, the leader of the Labour Party, Jeremy Corbyn, said that he won’t join any talks unless the case of a no-deal Brexit was off the table.

In our view, the rejection of May’s deal combined with yesterday’s results bring us back to square one. Now, we have to wait what kind of a plan B May will bring back to Parliament and whether there is any hope for MPs to support it. With EU officials repeating themselves, even yesterday, that they will not renegotiate, we find it hard for any significant amendments to be broadly accepted. As we already noted yesterday, still all scenarios are on the table, ranging from a hard Brexit to a no Brexit at all. That said, the outcome that everyone believes should be avoided is the case of a no-deal withdrawal.

Given that the confidence-vote result was the base-case scenario, the pound did not react much. It strengthened around 45 pips against the dollar, to give those gains back within the next few minutes. That said, the currency remained supported throughout the day, maybe due to talks that a no-deal Brexit should be avoided. Perhaps market participants believe that the UK will seek any other option rather than crashing out with no accord, from extending Article 50 to a second referendum, or even revoke the process altogether.

As for our view, it remains the same as yesterday. Further headlines suggesting that a no-deal exit is unlikely could keep the currency supported. On the other hand, anything pointing to no consensus of how to move forward could revive fears of a disorderly withdrawal and thereby, sterling could come under renewed selling interest.

EUR/GBP – Technical Outlook

This week, EUR/GBP has been trading south, as from the two currencies, the euro seems to be the weaker one. Last Friday, the pair exited the range, that it was trading in recently, through the lower bound of it, signalling the beginning of a small downtrend that could last for a while. The intraday spike up that we saw on Tuesday was driven by the UK Parliament vote, after which, the pair quickly resumed its drift lower. Such activity formed a short-term downside resistance line, drawn from the high of the 11th of January, which we will keep a close eye on. Looking at our oscillators, both are suggesting that the pair has now bottomed, but until they start firmly pointing higher, we will continue examining the downside.

A drop below the key support area at 0.8840, may clear the way for a further slide, where the next potential support zone could be seen at 0.8810, marked by the low of the 28th of November 2018. When that zone was tested back in November, EUR/GBP rebounded strongly from it. There is a chance to see a similar scenario playing out this time as well, where the pair might retrace back up a bit. But as long as the rate remains below the aforementioned short-term downside line, the previously-mentioned rebound could be seen as a correction and the bears may use this as a good opportunity to step in and drive EUR/GBP back down again. This is when we will aim for the 0.8810 obstacle again, a break of which could lead towards the 0.8774 hurdle, marked by the high of the 12th of November.

Alternatively, in order to consider the upside again, we would need to see a break of the previously-discussed downside line and also the rate jumping above the 0.8909 barrier, which is the intraday swing high of the 15th of January and the low of the 13th of the same month. This way EUR/GBP could target the 0.8945 resistance line, which is the lower bound of the above-mentioned range. If it fails to withstand the bull-pressure, this may place the rate back inside the range and could lead the pair to the 0.8985 level, marked by the high of the 15th of January.

![]()

Will Huawei’s Investigation Affect US-China Trade Talks?

Outside the Brexit land, the financial community continued trading in a somewhat risk-on mood. Although Aussie and Kiwi were the main losers among the major currencies yesterday, major EU and US indices ended their trading mostly in the green. The exception was UK’s FTSE 100, which closed 0.47% down. This may be due to the pound’s strength. Many companies of the index generate profits in other currencies, for example dollars. So, when the pound strengthens, these profits worth less in terms of pounds.

That said, risk appetite eased overnight, with Japan’s Nikkei 225 and China’s Shanghai Composite index ending their sessions 0.22% and 0.42% down respectively. This may have been due to headlines that US prosecutors are investigating whether Huawei stole trade secrets from US businesses. If this proves to be true, it could pour some cold water on expectations that China and the US are getting closer to end their trade conflict, which has been taking a toll on global growth, especially the Chinese economy. What’s more, the longest government shutdown in the US history continues, increasing the risks for the US economy to start feeling the heat.

As for our view, we will switch to flat for now with regards to the broader market sentiment. We prefer to wait and see whether the Huawei investigations will affect negotiations between China and the US. If not, further progress combined with Chinese officials’ willingness to support their economy with further simulative measures could boost again investors morale. The recent dovish shift by several Fed officials, including the leading hawk Esther George, is also a supportive factor. On the other hand, anything pointing that developments around the US-China trade standoff have changed course, as well as signs that the US shutdown have started leaving its marks on the US economy, may hurt risk appetite. This means that equity markets and the risk-linked currencies are likely to come under pressure, as investors seek shelter to safe havens, like the Japanese yen.

DAX – Technical Outlook

Since the end of December 2018, DAX had been on a gradual move higher, above a short-term upside support line. That said, from the middle of last week, the index started moving sideways, trading between the 10785 and 10950 levels. Overall, DAX also remains below its medium-term downside resistance line, taken from the end of September last year. For now, we will stay neutral and wait for the index to get out of the above-mentioned range and to break either the upside or the downside line.

If DAX manages to break the upper bound of the small range and gets above the downside resistance line, this could invite more buyers, who could elevate the price. At the same time, the index would be trading above the psychological 11000 barrier, which could open the path towards the next potential area of resistance at 11090, marked by the high of the 6th of December last year. If the price acceleration doesn’t end there, DAX could make its way to the 11270 hurdle, which is the high of the 5th of December of the same year.

On the downside, we will start examining areas that were last time seen in the beginning of January and the end of December, only if DAX breaks below the lower bound of the aforementioned range and pierces through the short-term upside line. This way, the path back down to the 10710 hurdle could be opened. The area acted as good support on the 7th of January, but if it fails to withhold the price from falling, the next support zone could be seen near the 10625 obstacle, a break of which could drag the index to the 10535 level, marked by the intraday swing high of the 3rd of January.

![]()

As for Today’s Events

During the European session, we get Eurozone’s final inflation data for December and as usual, the final prints are expected to confirm their preliminary estimates. Specifically, they are expected to confirm that headline inflation slowed to +1.6% yoy from +1.9%, and that the core rate remained unchanged at 1.0%.

In the US, housing starts, building permits and new home sales for the same month are coming out. Expectations are for housing starts and building permits to have declined, while new sales are anticipated to have increased. The Philly Fed manufacturing index for January and initial jobless claims for the week ended on the 11th of January are also coming out. The Philly Fed index is anticipated to have increased to 10.0 from 9.1, while initial jobless claims are expected to have risen slightly, to 219k from 216k the week before.

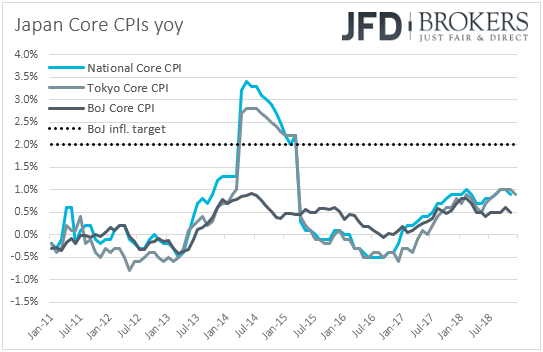

As for tonight, during the Asian morning Friday, we have Japan’s National CPIs for December. No forecast is available for the headline print, but the core rate is expected to have ticked down to +0.8% yoy from +0.9%. Both the more-forward-looking Tokyo CPIs for the month slowed, with the headline rate tumbling to +0.3% yoy from +0.8%, something which suggests that the headline National rate may fall notably as well. Further slowdown in Japan’s National inflation metrics could add more credence to our longstanding view that BoJ policymakers have still a long way to go before considering a meaningful step towards normalization, especially with the Bank’s own core CPI measure sitting at +0.5% yoy. The nation’s final industrial production print for November is also scheduled to be released.

We also have two speakers on today’s agenda: ECB Executive Board member Sabine Lautenschläger and Fed Board Governor Randal Quarles.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

68% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.