Market sentiment was hurt yesterday following a report that the US President plans to proceed with tariffs on USD 200bn worth of Chinese goods as soon as next week. The dollar and the yen strengthened, while equity indices slid. As for today, attention is likely to turn back to NAFTA talks as the deadline nears.

USD and JPY Strengthen as Trump Hurts Risk Sentiment

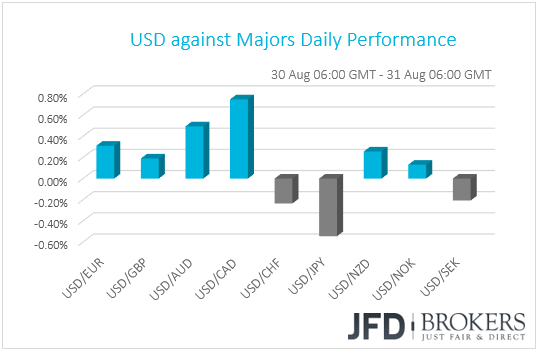

The dollar traded higher against most of its G10 counterparts yesterday. It gained the most against CAD, AUD and EUR in that order, while it lost ground versus JPY, CHF and SEK.

Once again, the main driver of the greenback was a change in the broader market sentiment, and this is evident by the strengthening of the other currency that tends to attract safe-haven flows when investors get nervous, the yen.

Risk appetite was hurt yesterday following a report, citing six people familiar with the matter, that US President Donald Trump wants to proceed with imposing tariffs on USD 200bn worth of Chinese goods as soon as the public-comment period ends next week. The report also noted that tariffs could be enacted in instalments. On top of this report, overnight, the President threatened to pull the US out of the WTO if the Organization doesn’t “shape up”.

Although Trump’s plans for imposing duties on USD 200bn Chinese imports are not something new, the fact that he is in a hurry to do so may have weighed on expectations that the two nations could eventually work things out. Last week, low-level talks did not bear fruit but reports that the two countries are working on a road map that would eventually lead to top-level meetings had been keeping investors’ hopes alive.

As for our view, even if the US proceeds with the tariffs as early as next week, we don’t expect this to result in a major turmoil. This round of tariffs is something that investors have already noted on their agendas, and we think that there is little of it left to be discounted. Even the threat of pulling the US out of the WTO is not new. Reports back in June suggested that Trump already expressed such a desire to top White House officials. We believe that for fear and anxiety to surge notably, we may need to get something new, something unplanned, something to catch the market off guard. Off course the measures could have a serious impact on the global economy in the longer run, but let’s not forget that market participants are probably trying to figure that out now.

Tumbling emerging market currencies may have also added to the dollar’s boost. The Argentine peso continued to plummet on concerns that Argentina could soon default, after the government asked for the early release of a USD 50bn loan from the IMF on Wednesday. Yesterday, Argentina's central bank decided to raise interest rates to 60% from 45%, but even after that, the peso continued to fall.

The Turkish lira kept drifting lower as well following reports that a Deputy Governor of the Turkish central bank decided to resign. The lira’s slide was revived on Monday as Turkish markets reopened following last week’s holidays. This shows that market participants remain concerned over the US-Turkey standoff, as well as over President Erdogan’s influence on monetary policy.

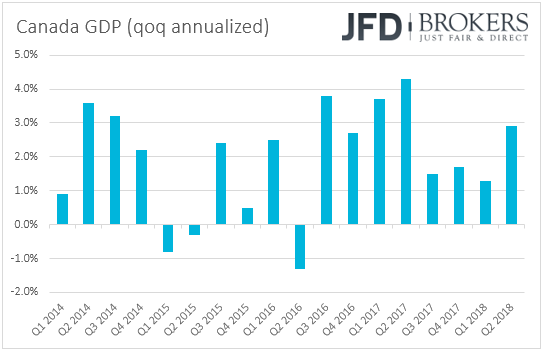

Back to the G10s, the Canadian dollar was the main loser yesterday, following the release of Canada’s GDP data for Q2. The data showed that the economy grew at an annualized qoq rate of 2.9%, falling just shy of the 3.0% estimate. June’s monthly rate fell to 0.0% from 0.5% in May. Although the quarterly data suggests the fastest pace in one year, this may have not been enough to bolster expectations that the BoC will proceed with hiking rates next week. That said, given that Canada’s latest economic data have been more than encouraging, we believe that the Bank remains on track for hiking at least once more this year. If economic indicators keep coming out on the bright side, this may be the case in October.

As for today, CAD-traders are likely to turn their attention back to NAFTA talks as the deadline nears. Despite some issues remaining on the table, there is still optimism over the matter. Overnight, Canada’s Foreign Minister Chrystia Freeland said that there is progress and that they will keep working towards sealing a deal. Even President Trump said, “I think we are close to a deal”.

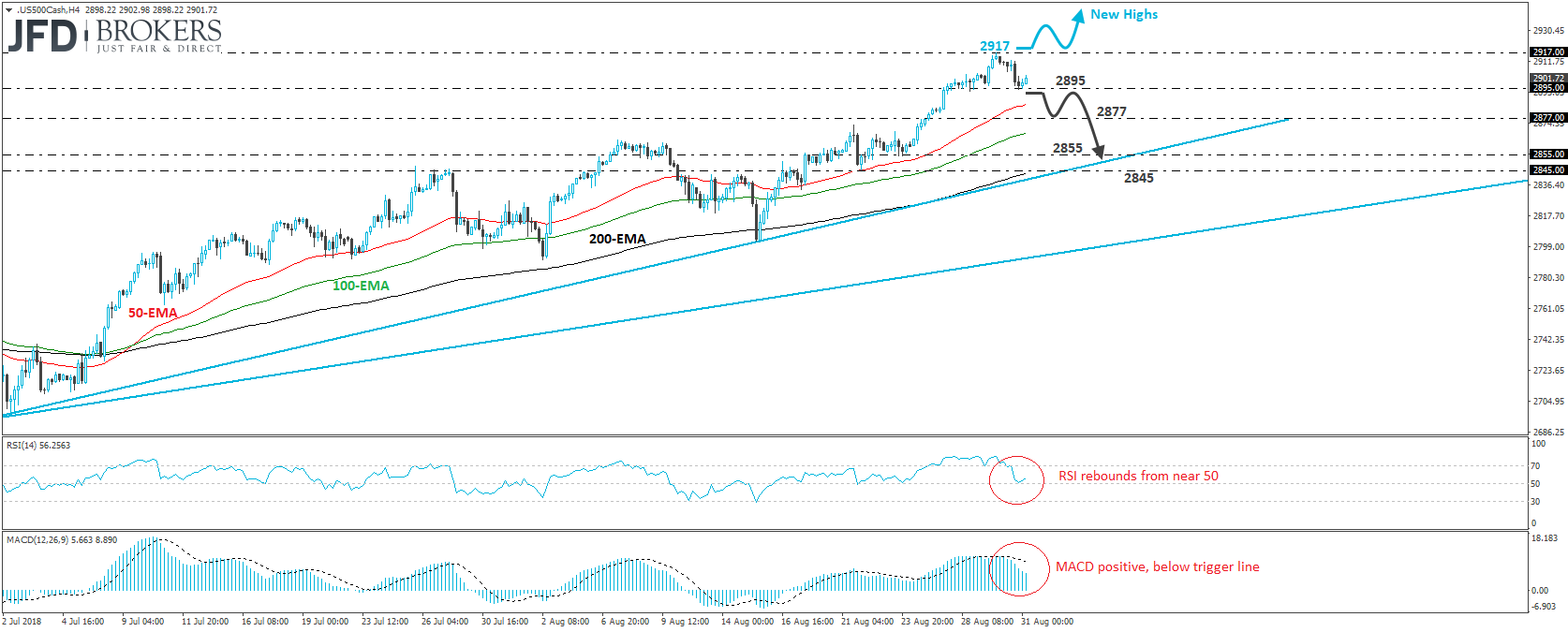

S&P 500 – Technical Outlook

The S&P 500 cash index traded lower yesterday, after it hit a new record high near 2917 on Wednesday. That said, the slide was stopped near the 2895 level. The price structure continues to suggest that the medium-term uptrend that started in April is intact and thus, we would expect the bulls to take the reins back some time soon.

If they manage to do that today, then we may see them aiming for another test near the index’s all-time high, at around 2917. If they prove strong enough to overcome it, then they would start exploring unknown territories and aim for new records.

Taking a look at our short-term momentum studies, we see that the RSI slid below 70, but then it rebounded from near its 50 line. The MACD, although below its trigger line, remains within its positive territory and shows signs that it could start bottoming soon as well.

On the downside, a clear and decisive break below 2895 could initially aim for January’s highs, at around 2877. Another break below that level could pave the way for the 2855 barrier, or the short-term uptrend line drawn from the low of the 28th of June. However, the near-term outlook would still be positive and thus, we would consider such a retreat as a corrective move.

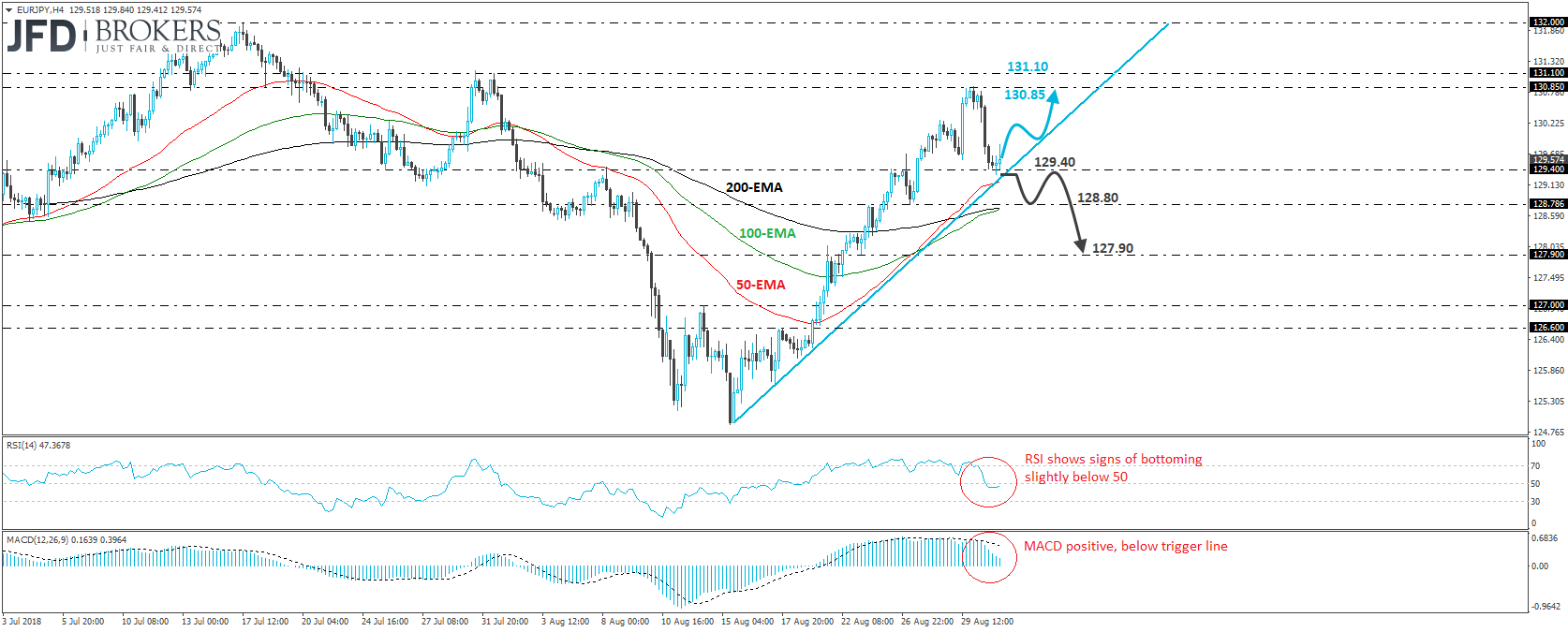

EUR/JPY – Technical Outlook

EUR/JPY tumbled yesterday to eventually hit support near 129.40, slightly above the short-term uptrend line drawn from the low of the 15th of August. In our view, given that the rate remains above that line, the short-term picture is cautiously positive.

If the bulls prove strong enough to jump into the action from current levels, then we would expect them to aim for another test at 130.85, near Wednesday’s peak, or near the 131.10 hurdle, a resistance defined by the highs of the 31st of July and the 1st of August.

Out short-term momentum studies support somewhat the notion for a potential recovery. The RSI has bottomed below its 50 line and appears able to move back above that equilibrium level, while the MACD, even though below its trigger line, is still above zero and shows signs that it could start turning up as well.

On the downside, we would like to see a clear dip below the 129.40 barrier and the aforementioned short-term uptrend line before we assume that the bulls have lost the battle. Such a break could initially aim for the 128.80 zone, the break of which could carry more bearish implications, perhaps towards our next support of 127.90.

As for Today’s Events

The calendar appears relatively light today, and thus we expect market participants to remain focused on headlines surrounding the trade front, and especially the NAFTA talks. as the deadline for a deal is tonight.

The only top-tier release today is Eurozone’s preliminary inflation data for August. Expectations are for both the headline and core rates to have remained unchanged at +2.1% yoy and +1.1% yoy respectively, something that is unlikely to alter market expectations with regards to the ECB’s future plans. Even a small upside surprise is doubtful to do that. At the press conference following the latest ECB meeting, President Draghi noted that according to money markets, expectations of the future rate path are very well aligned with the anticipation of the Governing Council, backing the market consensus for a hike in late 2019, and disappointing those expecting to get clues that summer months are also candidates for such a move. In our view the “at least through the summer of 2019” interest-rate guidance means that rates could start rising in September 2019 the earliest. Thus, even if inflation accelerates somewhat, there is not much room for hike expectations to come forth. Germany’s retail sales for July are due to be released as well.

From the US, we have the final UoM consumer sentiment index for August, which is expected to have been revised up to 95.5 from 95.3. The final UoM 1- and 5-year inflation expectations for the month are also coming out.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.