Market sentiment took a 180-degree turn yesterday, perhaps due to the lack of clarity around the US-China ceasefire, as well as recession fears due to the inversion of the US Treasury yield curve. The pound traded in a rollercoaster manner, to eventually end the day lower against the dollar, driven once again by Brexit related headlines. As for today, CAD-traders are likely to turn their attention to the BoC monetary policy decision.

Sentiment Gets Hit Due to Trade Doubts and Yield Curve Inversion

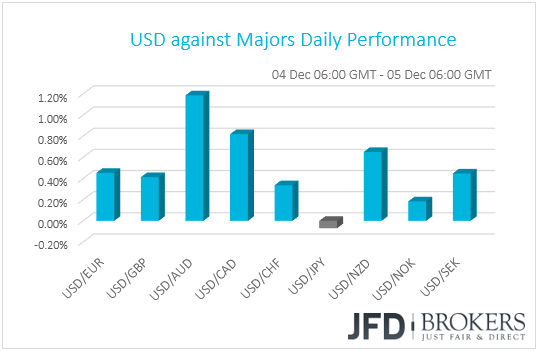

The dollar rebounded and outperformed all but one of the other G10 currencies on Tuesday. The only currency that managed to resist the dollar’s strength, and actually gained somewhat against it, was the safe-haven yen. The biggest losers were the commodity-linked currencies AUD, CAD and NZD, with the former getting a strong hit overnight due to Australia’s worse-than-expected GDP data for Q3.

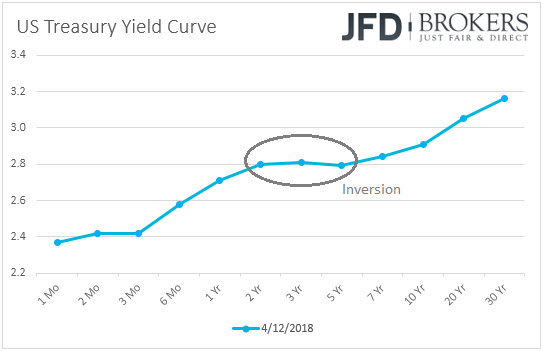

Following the boost in risk appetite due to the outcome of the Trump-Jinping meeting in Buenos Aires, the FX performance pattern suggests a switch back to “risk off”. Indeed, major EU and US equity indices ended Tuesday’s session in the red, with CBOE VIX, the so-called fear index, surging 26.6%. The negative sentiment rolled over into the Asian morning Wednesday as well, with Japan’s Nikkei 225 and China’s Shanghai Composite closing 0.59% and 0.61% down respectively. The catalyst behind the switch may be a combination of doubts around the US-China trade saga, as well as fears of a recession due to the inversion of the 2yr/5yr and 3yr/5yr parts of the US Treasury yield curve.

Getting the ball rolling with the US-China sequel, as we noted yesterday, the lack of clarity in the two nation’s statements after the Trump-Jinping meeting suggests that they still have a long way to go before they seal a final accord. US President Trump’s comments that he could enact fresh tariffs if the two sides are not able to resolve their differences did not help either. All this adds validity to our view that the outcome of the meeting in Buenos Aires was nothing major to cheer about.

Now moving to the Treasuries, the 5yr-2yr and 5yr-3yr yield spreads dipped into negative territory, while the 10yr-2yr difference hit its lowest level since July 2007. An inversion of the 2yr/10yr part of the US Treasury yield curve is seen by the market as a precursor to a recession, given that most of the times this has happened, a US recession followed.

With short-term yields driven up by the Fed’s hikes, but the long-dated ones kept at low levels perhaps due to investors’ concerns over an economic slowdown, this could result in a vicious cycle and thereby, a recession could become a self-fulfilling prophecy. Concerns over economic growth lead to a flattening curve, which in turn sparks more fears over economic growth. In any case, no one can say for sure that we are standing on the edge of a cliff.

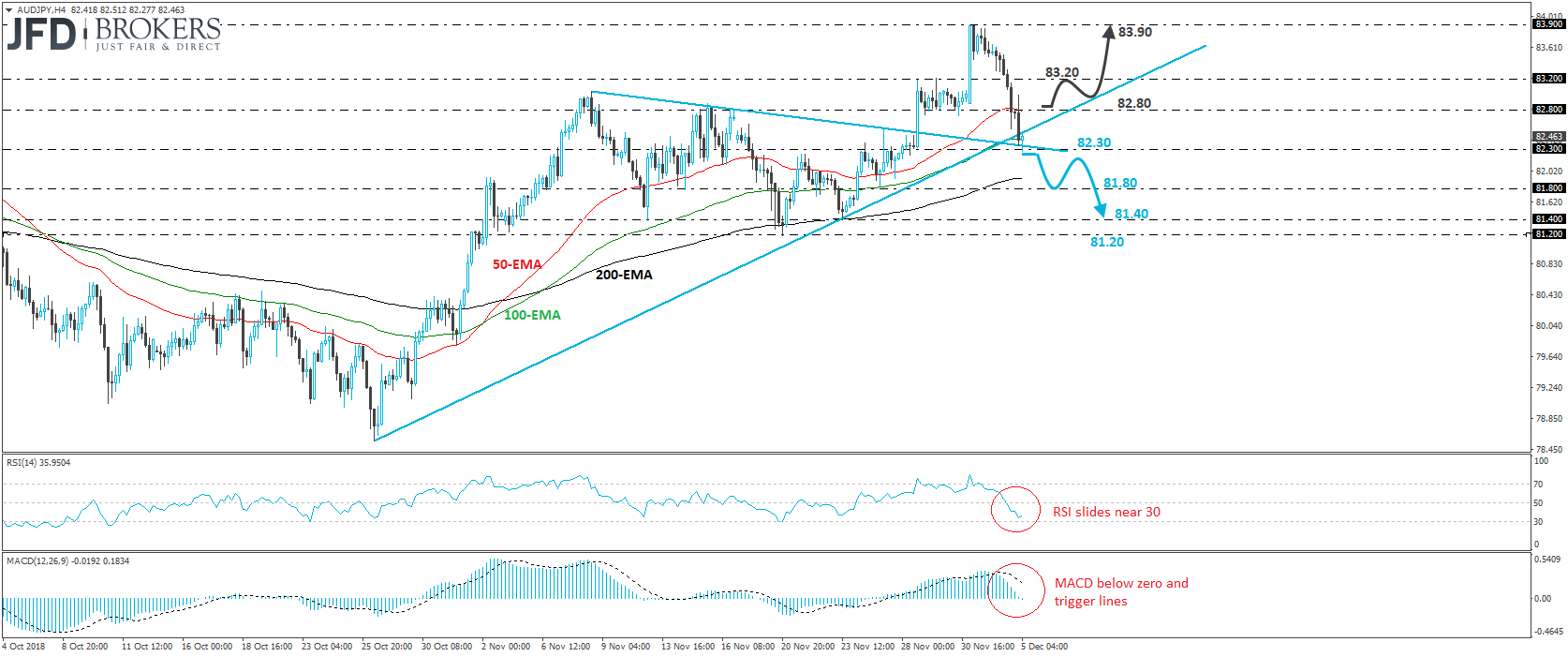

AUD/JPY – Technical Outlook

AUD/JPY tumbled yesterday, falling below the upside support line drawn from the low of the 26th of October. However, the slide was stopped by the crossroads of the 82.30 level and the prior downside resistance line taken from the peak of the 8th of November. Despite the dip below the upside line, the fact that the rate is still above the aforementioned downside resistance line make us adopt a neutral stance for now.

We would like to see a clear dip below 82.30 before we get confident on more bearish extensions. Such a dip would drive the rate back below the downside line drawn from the peak of the 8th of November and could initially aim for the low of the 27th of that month, at around 81.80. Another break below 81.80 could extend the slide towards the 81.40 zone, defined by the low of the 23rd of the month.

Looking at our short-term oscillators, we see that the RSI fell below 50 and edged south to hit support slightly above 30. The MACD, already below its trigger line, has just obtained a negative sign. These indicators detect negative momentum, but the fact that the RSI turned somewhat up from slightly above 30 enhances our choice to stand pat for now.

On the upside, we would like to see a clear move above 82.80 before we start examining higher levels. This could lead to a test near the 83.20 zone, the break of which may set the stage for extensions toward Monday’s peak, at around 83.90.

Pound Stays Brexit Driven, BoC Decides on Policy

The British pound ended the day on the back foot against the dollar, but for sterling traders, that wasn’t a one-way ride. Initially, the currency strengthened on easing concerns over a disorderly UK-EU divorce after a senior EU legal advisor said that the UK could change its mind over Brexit without the saying of other EU member states. However, the rally was stopped after Theresa May’s spokesman said that the government is not going to revoke its notice, with the pound taking the down road. The slide accelerated after May lost a vote on contempt of parliament for not releasing the full legal advice on Brexit, but the pound rebounded again somewhat following another vote which gives more power to Parliament if the vote on the 11th of December fails.

Although this suggests that a no-deal Brexit is now less likely, it also increase the chances for May’s Brexit plan to get defeated next week. With all this uncertainty surrounding the Brexit landscape, we expect more volatile swings in the pound, with any rebounds likely to stay limited and short-lived.

Moving to Canada, the Loonie was among the main losers yesterday, reversing all the gains it posted on Monday. On Monday, the Canadian currency surged, perhaps driven by the rebound in oil prices after Russia agreed to renew its cooperation with OPEC, something that increases the chances for a production cut at tomorrow’s OPEC+ meeting in Vienna.

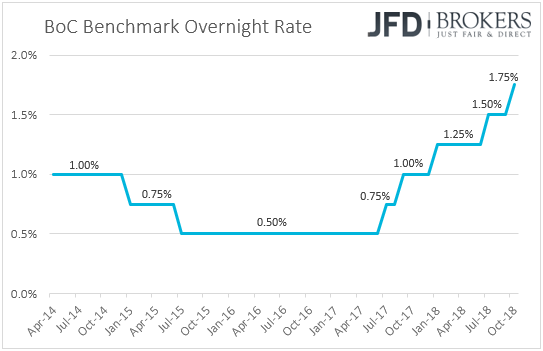

As for today, CAD-traders are likely to keep their gaze locked on the BoC policy meeting. Officials are expected to keep interest rates untouched after raising them to +1.75% at their latest meeting. If so, given that this will be one of the “smaller” meetings that are not accompanied by updated economic projections, neither a press conference, all the attention is likely to fall to the meeting statement.

At the previous gathering, apart from raising rates, officials removed from the accompanying statement the part saying that they will “take a gradual approach” with regards to future rate increases. In our view, this means that if data suggest so, interest rates can rise faster than previously anticipated.

Latest data showed that the unemployment rate declined to 5.8% in October from 5.9% in September, while inflation accelerated in both headline and core terms. However, Friday’s GDP data showed that the economy shrank 0.1% in September, which may have prompted market participants to take a few January-hike bets off the table. Thus, it would be interesting to see how upbeat (or not) the statement will be, and how this will shape expectations around the Bank’s next move.

GBP/CAD – Technical Outlook

GBP/CAD traded in a rollercoaster manner yesterday, and during the early European morning today, it is trading slightly below the 1.6890 resistance zone. Monday’s tumble and yesterday’s early rebound confirmed a lower low on the 4-hour chart, which, combined with the fact that the pair continues to trade below the downside line drawn from the high of the 14th of November, suggests that the near-term outlook is cautiously negative.

A dip back below 1.6820 could encourage the bears to take back the driver’s seat and initially aim for the 1.6760 zone. Another break below 1.6760 could target Monday’s low of 1.6720, the break of which would confirm a forthcoming lower low and may pave the way for the 1.6650 territory, defined by the lows of the 30th and 31st of October.

Shifting attention to our short-term momentum indicators, we see that the RSI exited its below-30 zone and moved towards its 50 line, while the MACD, although negative, lies above its trigger line and points up. Having these signs in mind, we remain cautious of some more recovery, but as long as such a recovery stays limited below the aforementioned downside line, we would still consider the short-term picture to be somewhat negative.

We prefer to wait for a clear break above 1.6945 before we assume that the bears have abandoned the battlefield. This may confirm a break above the downside line and could see scope for extensions towards the 1.7045 zone. Another break through the 1.7045 resistance may set the stage for the high of the 22nd of November, at around 1.7095.

As for the Rest of Today’s Events

During the European day, we get the final service-sector and composite PMIs for November from the European nations of which we get the manufacturing prints on Monday, as well as for the Eurozone as a whole. As usual, expectations are for a confirmation of the preliminary numbers. Eurozone’s retail sales for October are also coming out and are expected to have risen +0.2% mom after stagnating in September.

We get the November services PMI from the UK as well, which is expected to have risen to 52.5 from 52.2. This is the most important among the three UK PMIs, as the services sector accounts for near 80% of the nation’s total GDP. However, bearing in mind that pound traders have all their attention on the UK political scene, we expect the index to attract less attention than usual.

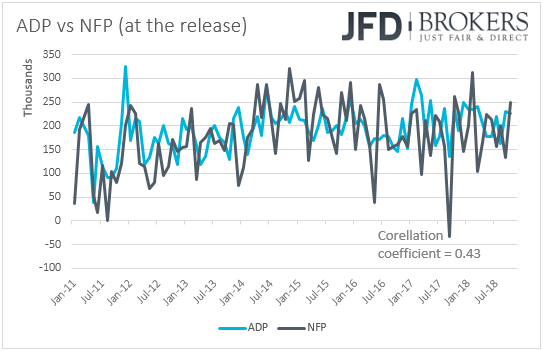

From the US, we get the ADP employment report for November. Expectations are for the private sector to have gained 196k jobs, less than the 227k in October. This could raise speculation that the NFP number, due out on Friday may also come below October’s print of 250k. Indeed, currently the NFP forecast is at 200k. However, we repeat to the umpteenth time that, even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are taken into account) has been very low in recent years. Taking into account data from January 2011, this correlation stands at 0.43. The final Markit services and composite PMIs for November, as well as the ISM non-manufacturing index for the month are also due to be released.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.