Market sentiment took a 180-degree turn yesterday, with equity indices turning down and safe havens taking the font seat, after US retail sales for December fell the most since September 2009. US President Trump’s decision to declare a national emergency in an attempt to fund his Mexican-border wall without congressional consent may have also weighed on market sentiment. In the UK, PM May suffered another defeat in Parliament, which, although symbolic, weakens her hand in last-ditch talks with EU officials. As for today, attention is likely to be on the conclusion of the US-China trade talks.

US Retail Sales Drop the Most Since 2009, UK PM May Defeated in Parliament

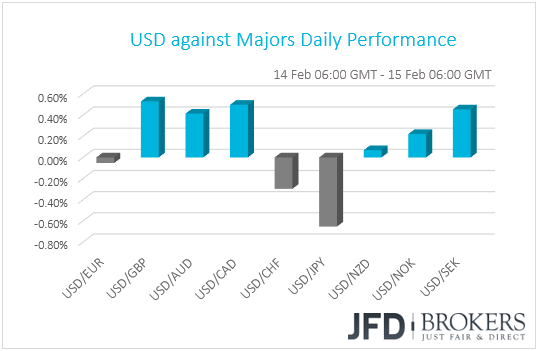

The dollar traded higher against the majority of the other G10 currencies. It outperformed GBP, CAD, SEK, AUD and NOK in that order, while it was lower versus the safe havens CHF and JPY. The greenback traded virtually unchanged against EUR and NZD.

The pattern suggests a switch to risk-off trading, something that was evident by the performance in the equity world as well. Most major EU bourses ended their trading in negative territory, while in the US, both the S&P 500 and the Dow Jones closed 0.27% and 0.41% down respectively. Nasdaq closed fractionally positive. The negative sentiment rolled over into the Asian morning Friday, with Japan’s Nikkei 225 and China’s Shanghai Composite sliding 1.13% and 1.37%.

The initial trigger for the 180-degree turn in risk appetite may have been the disappointing US retail sales for December. The release showed that headline sales tumbled 1.2% mom, the largest decline since September 2009, while core sales fell more, 1.8% mom, which is the biggest drop since December 2008. The forecasts were for a slowdown to +0.1% from +0.2% for the headline print, while core sales were expected to have stagnated.

The surprisingly weak numbers raised fresh concerns over the health of the world’s largest economy and led to downside revisions in estimates for Q4 GDP, with the Atlanta Fed GDPNow model suggesting a +1.5% qoq SAAR growth rate, well below the +2.7% projection just a week ago. What’s more, apart from a flight to safety, the disappointing report slashed investors’ few hopes with regards to a Fed hike by the end of the year and prompted them to increase their cut bets. According to the Fed funds futures, the chance for a hike by year end fell to 2% from 12% yesterday, while the probability for a cut rose to 13% from 6%.

Strangely though, the greenback ended the day on the front foot against most of its major peers, even though it slid at the time of the release. This may have been due to weakness in other currencies, or perhaps the greenback put on its safe-have suit. It could be a combination of both but bearing in mind that the DXY index ended the day virtually unchanged, we believe that it may be more of the former case.

The pound was the main loser, sliding after UK PM Theresa May suffered another defeat in Parliament yesterday. British lawmakers voted 303-258 against May’s request for support in seeking changes to the initial withdrawal agreement. Although a symbolic and not legally-binding vote, meaning it does not prevent May to return to Brussels and try to renegotiate, the defeat shows how hard is for any agreement to get through the UK Parliament and could make EU officials even less willing to listen to May’s proposals.

We are now back to square one we believe. The chances for May coming back with a broadly accepted accord on February 26th remain very slim in our view. We will have to wait for February 27th, when the Parliament may have the option to vote for legally binding amendments. Up until then, with no signs of how a no-deal Brexit can be averted, the pound is likely to stay under selling pressure.

The second loser in line was the Loonie, which weakened after Canada’s manufacturing sales for December tumbled 1.3% mom, instead of rising 0.3% as the forecast suggested. On top of that, November’s print was revised down to -1.7% mom from -1.4%. Although at its latest policy meeting the BoC kept the door wide open for more rate increase in the foreseeable future, signs of weakening economic activity may raise doubts amongst investors on that front.

GBP/USD – Technical Outlook

Yesterday, GBP/USD took another hit and broke below both, its key support area at 1.2850 and the short-term tentative upside support line drawn from the low of December 12th. The pair also continues to trade below its short-term downside resistance line taken from the high of January 31st. Even though GBP/USD could retrace back up, as long as it remains below both of the above-mentioned lines, we will continue targeting lower areas.

As mentioned above, as small correction to the upside is possible, but if the rate gets held near the 1.2830 level, or even near the previously-mentioned 1.2850 barrier, this could invite the bears back to the table, who, in their case, could drive GBP/USD lower again. This is when we will target the 1.2773 obstacle again, a break of which could open the door towards lower levels, as such a move would confirm a forthcoming lower-low. We will then aim for the next key support zone, at 1.2710, which provided good support back on January 6th, 8th and 11th.

In order to shift our view to the upside, at least for the short-term, we would like to see a break above both aforementioned upside and the downside lines. This could attract even more bulls, who may push GBP/USD to test the high of January 13th, at 1.2955. We might see a small throwback, but if the bulls remain strong, they may take charge again and lift the pair above the 1.2955 barrier and push it further. GBP/USD could easily make its way to the psychological 1.3000 level, which is near the highs of February

![]()

Trump Decides to Declare National Emergency, US-China Talks to Conclude

Back to the broader risk environment, US President Trump’s decision to declare a national emergency in an attempt to fund his Mexican-border wall without congressional consent may have also weighed on market sentiment. Even though he agreed to sign a spending bill overwhelmingly passed yesterday in Congress, a move that would avert another government shutdown, his national emergency decision drew immediate criticism from Democrats, with the House of Representatives Speaker Nancy Pelosi keeping the door open to a legal challenge.

Now with regards to the US-China sequel, it’s the last day of this round of talks, with US representatives Mnuchin and Lighthizer scheduled to meet with China’s President Xi Jinping. According to White House economic adviser, there was no decision to extend the March 1st deadline, something that comes in contrast with Wednesday’s reports over a 60-day extension and puts more weight on today’s outcome. While Kudlow said, “The vibe in Beijing is good”, FT reported that both sides have made little progress, putting investors in a wait-and-see mode.

Remember that we’ve been repeatedly saying that we don’t expect a final accord at this round. We stick to our guns and we believe that this could happen at a Trump-Xi meeting, if today’s outcome keeps the prospect high. In any case, investors could still cheer positive remarks, as an upbeat result may revive hopes for an official and final deal soon. Equities are likely to regain some of yesterday’s lost ground, while safe havens are likely to retreat. On the other hand, anything confirming the headlines suggesting very little progress could raise doubts over a final accord, especially just after Kudlow’s remarks that the deadline will not be extended. Stocks may continue to slide, as investors continue to seek shelter in safe havens.

DJIA – Technical Outlook

The US equity markets took a hit yesterday, with the DJIA and S&P 500 closing slightly in the negative territory, whereas Nasdaq 100 managed to maintain some of its gains. Looking at the technical picture on the 4-hour chart of the Dow Jones Industrial Average cash index, we can see that the index is testing the short-term tentative upside line taken from the low of December 27th, but has now shifted slightly below the 25300 support area. For now, we will step aside and remain flat, until we see a clear confirmation break of one of our key levels.

If the price drops below the 25300 hurdle and travels lower, Dow may easily test the psychological 25000 mark again. This is where the index might meet the medium-term tentative downside resistance line, which is running from the highest point of October, and test it from above. If the DJIA struggles to fall below that zone, this could be quickly picked up by the bulls and we could see the price shifting back towards the 25300 obstacle, which if broken, could increase the chances of DJIA to re-test this week’s high, at around 25600.

Alternatively, if we see DJIA breaking below the aforementioned psychological 25000 barrier, this could raise concerns about the near-term upside scenario. But for a better confirmation of further downside, we would like to see a break below the 24850 hurdle, marked by the low of February 8th. This way, a further slide may bring the price down to the 24500 obstacle, a break of which could send the index lower towards the 24300 level, which is near the lows of January 23rd and 28th.

![]()

As for Today’s Events

During the European day, we get the UK retail sales for January. The forecasts suggest that both headline and core sales rose 0.2% mom after sliding 0.9% and 1.3% respectively. This is likely to drive both the yoy rates up, to +3.4% and +3.0%, from 3.0% and 2.6%. The case for rising yoy rates is supported by the BRC retail sales monitor for the month, the yoy rate of which surged to +1.8% from -0.7% previously. Eurozone’s trade balance for December is also coming out, but no forecast is currently available.

In the US, industrial and manufacturing production for January are due out, as well as the preliminary UoM consumer sentiment index for February. Both the industrial and manufacturing monthly rates are expected to have slid to +0.1% mom, from +0.3% and +1.1% respectively, while the UoM index is expected to have risen to 94.0 from 91.2.

As for the speakers, we have three on the agenda: Atlanta Fed President Raphael Bostic, Cleveland Fed President Loretta Mester, and ECB Supervisory Board member Ignazio Angeloni.

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

76% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.