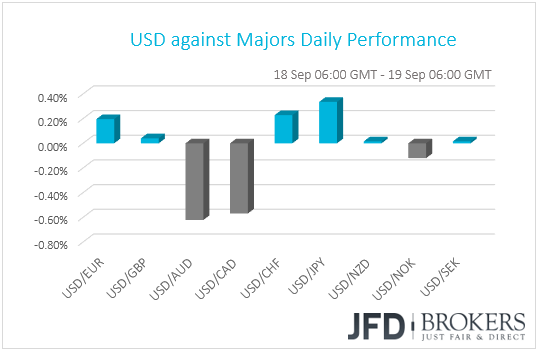

The Aussie was the biggest gainer and the yen was the main loser against the greenback yesterday, as the financial community continued to shrug off the latest escalation in the US-China trade saga. As for today, pound traders are likely to focus on the UK CPIs for August, but most importantly on the informal EU summit in Austria, where Brexit is expected to take center stage.

AUD Gains, JPY Loses as Investors Take the US-China Dispute in Stride

The dollar traded mixed against the other G10 currencies on Tuesday. It gained against JPY, CHF and EUR in that order, while it underperformed versus AUD, CAD and NOK. The greenback traded virtually unchanged against GBP, NZD and SEK.

The weakening of the yen and the strengthening of the Aussie suggest that market participants continued to shrug off the latest escalation in the US-China trade dispute. This is evident by the performance of the equity markets as well. Major EU and US indices ended their trading in positive territory, with the only exception being UK’s FTSE 100, while during the Asian session Wednesday, Japan’s Nikkei 225 and China’s Shanghai Composite Index closed 1.08% and 1.14% up.

On Monday, the US announced that it will proceed with the new round of tariffs on USD 200bn worth of Chinese goods at a 10% rate, effective on the 24th of September, while yesterday, China retaliated with 5-10% tariffs on USD 60bn worth of US imports, a lower rate range than the 10-20% initially planned. China's measures will also go into effect on the 24th of September.

Investors may have taken the escalation in their stride given that all this was flagged ahead of the official announcements, and because both nations decided on lower tariff-rates than they initially planned. On top of that, the fact that China remains willing to send a representative, even a lower level official, to the US for talks may have also helped to keep risk appetite supported.

Back to the currencies, although the yen was the main underperformer against the greenback, it did not react to the BoJ decision overnight. The Bank decided to maintain its policy unchanged via a 7-2 vote and maintained the view that Japan’s economy is expanding moderately. What’s more, it reiterated that it intends to maintain the current extremely low levels in interest rates for an extended period of time.

Apart from the Aussie, the Loonie gained notably as well, perhaps due to the spike in oil prices which came following reports that Saudi Arabia is now comfortable with Brent rising above USD 80 per barrel. Focus for CAD-traders now turns to NAFTA talks as Canada’s Foreign Minister Chrystia Freeland is back to Washington in order to resume talks with US Trade Representative Robert Lighthizer.

AUD/JPY – Technical Outlook

Finally, AUD/JPY broke through its short-term downwards moving trendline taken from the peak of the 19th of July, this way potentially abandoning the bearish case, at least for the short-run. We would now expect the pair to continue traveling higher, towards the August highs again. Even if there would be a correction to the downside, still, this could be seen as a good opportunity for the bulls to step in and drive AUD/JPY higher.

From the early hours of the Asian morning, AUD/JPY found good resistance near 81.50, which now becomes the level to monitor. A break and a close above that level could open the way towards the next resistance, seen around the 81.80 zone, which was the high of the 29th of August. If the bulls remain in control, a move above that 81.80 could really put the downside off the table, at least for the near-term, as this could lead to much higher levels. The next potential resistance level to keep an eye on could be the 82.65 hurdle, or even the 82.80 barrier, marked by the high of the 8th of August.

Alternatively, for us to switch back into the bear-mode, we would need to see a break and a close below the aforementioned downside trendline, where at the same, AUD/JPY would place itself beneath the 80.60 obstacle, marked by the high of the 17th of September. This is where the bears might find the pair interesting again and they could potentially pull it down even lower towards 79.95, or even the 79.77 level, which held the rate firmly from dropping lower on the 18th of September. Further declines could lead to a test of the 79.50 hurdle, marked by the inside swing highs of the 7th, 11th and the 12th of September. That is where the AUD/JPY could stall for a bit, until the bulls and the bears decide on who takes control from there.

![]()

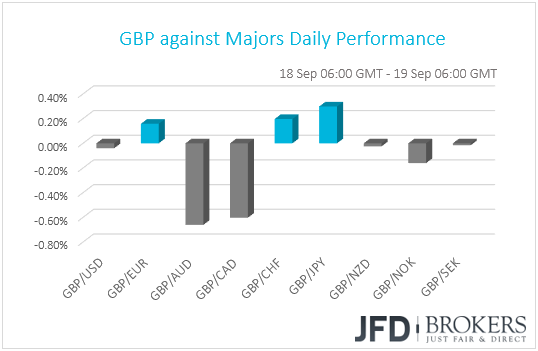

GBP-Traders Wait for UK CPIs and EU Summit

Given that the British pound traded virtually unchanged against its US counterpart, it performed in a similar fashion against the other G10 currencies. It gained the most against the safe-haven JPY, while it underperformed against AUD, CAD and NOK.

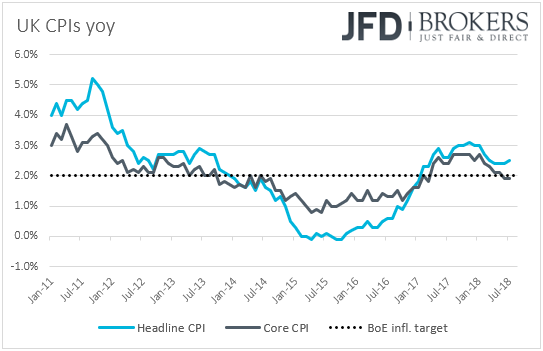

Today, the UK CPIs for August are due to be released. Expectations are for both the headline and core rates to have ticked down +2.4% yoy and +1.8% yoy, from +2.5% and +1.9% respectively. At last week’s policy meeting, the BoE kept rates unchanged at +0.75% and reiterated that an ongoing tightening of monetary policy over the forecast period would be appropriate, but any future rate increases are likely to be gradual and to a limited extend.

In our view, the key takeaway from this decision is that the Bank’s plans remain more or less the same as in August. The Bank is probably done hiking for this year and according to UK OIS forward curve, the next rate increase is almost fully priced in for November 2019. Thus, even if inflation does not slow as the forecasts suggest, we doubt that this could help drive forth expectations over the next rate increase. We believe that a notable acceleration is needed for something like that to happen.

GBP-traders may keep paying more attention to Brexit developments and specifically an informal EU summit in Austria scheduled to start today. Yesterday, UK PM Theresa May sounded optimistic, saying that “The withdrawal agreement is virtually agreed”, while EU chief negotiator Michel Barnier noted that the EU is ready to improve its proposal for the backstop on the Irish border. He also noted that the October summit, will be “the moment of truth”.

Having all these in mind, and also taken into account that the EU does not plan to issue a statement on Brexit at this meeting, we will focus on any headlines and comments in order to get a better idea of how close the two sides are in securing a deal. Remember that around three weeks ago, reports suggested that officials on both sides admitted that finding common ground by October was unlikely, and they would aim to finalize the terms of the divorce by November.

Thus, anything suggesting that a deal can be struck at the upcoming summit instead of November, may encourage more GBP-bulls to enter the action and drive the pound higher. On the other hand, headlines or remarks suggesting that the process remains frozen may push expectations for a deal to December or even revive fears that the two sides are unlikely to reach an accord. Something like that could prompt GBP-traders to liquidate long positions, with the pound likely to erase a decent a portion of its latest gains.

GBP/NZD – Technical Outlook

As we can see, since around the 10th of September, GBP/NZD has been trading sideways within a tight range. From the longer-term perspective, the pair looks slightly overbought, so there is a chance that we could see a bit of a corrective move to the downside in the short run. That said, we should understand the fact that, as long as GBP/NZD is within the boundaries of the aforementioned range, we have to remain cautious and wait for a confirmation break.

A break and a close below the lower side of the range could tempt the bears in driving the rate towards the 1.9755 obstacle, which was the peak of the 5th of September and also held the rate from falling on the 9th of September. If this time that line breaks, this could lead to further declines, where the 1.9650 zone could get tested. That area was marked by the inside swing high of the 6th of September.

The downside is currently supported by our oscillators. The RSI continues to slide and now has shifted below 50, still pointing down, this way showing its willingness to move lower. The MACD is also leaning to the downside, as it has moved lower away from its peak, seen on the 11th of September and still remains below the trigger line.

On the upside, a strong move through the 2.0030 level, which is the upper bound of the previously mentioned range, could indicate that the bulls are not willing to give up and the bears could start abandoning the field. The move could put the 2.0270 hurdle on the radar as it could be the next potential resistance for GBP/NZD. This has been the high of the 14th of June 2016. If that area is not able to withstand the pressure from the bulls, further acceleration of the rate could take the pair towards the 2.0400 barrier, marked by the inside swing low of the 23rd of June 2016.

![]()

As for the Rest of Today’s Events

Apart from the UK CPIs and the EU summit, we get the US building permits and housing starts, both for August, are coming out, as well as the nation’s current account balance for Q2.

With regards to the energy market, we get the Energy Information Administration inventory data for the week ended on the 14th of September. Expectations are for a 2.7mn barrels slide following a decline of 5.3bn barrels the week before. That said, yesterday, the API report showed a 1.25mn increase in inventories, and thus, we view the risks of the EIA data as skewed to the upside.

As for tonight, we get New Zealand’s GDP data for Q2. The forecast is for the qoq rate to have risen to +0.8% from +0.5%, but this could drive the yoy rate down to +2.5% from +2.7%. In any case, an acceleration to +0.8% in quarterly terms would be above the Bank’s latest estimate of +0.5% for the quarter and could ease some concerns with regards to a rate cut. At its August meeting, the Bank reiterated that the next move in interest rates could be up or down and pushed back the timing of when it expects rates to start rising, to September 2020 from 2019 previously.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.