The selling in the global equity markets continues. Investors are still hoping to see a good Christmas rally. But will that actually help? Brexit and Italy are in Focus again.

Markets in Turmoil Again

Once again, the indices have sold off and reached their October lows. Once more, the US indices have turned negative for the year, which now becomes a huge worry for all. But this should not be a surprise, as investors have been dumping US stocks for weeks now, because concerns over the performance of the global economy are greater than the feeling that everything would sort itself out. A big factor in all this, of course, is the US-China trade war, which had its negative effect on companies from both sides. Even major US technology companies, which are considered to be more resilient to shakes in the economy, are also taking a hit. The so-called FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) were seen as the thing-to-have in your portfolio, but as always, these companies also perform well mainly during the bull market. Nevertheless, these tech giants are still trying to stay afloat, at least for this year. But from that top 5, only Facebook and Google have wiped out their yearly gains so far. Of course, the year is not finished yet, so they could try and push back up, but for Facebook that could be a mission impossible, as for now, the recovery is nowhere in sight.

As we mentioned above, the weakening performance of the global economy, due to geopolitical tensions, together with the fear of rising interest rates is fuelling the sell-off. Investors are afraid of the potential fall in demand and that it will become more expensive for firms to run their day-to-day business with higher borrowing costs, which could result in lay-offs of workers.

In the middle of US-China trade disputes sits the European market, which is also taking a hit, as it is heavily reliant good trade relationships with both sides. Major European indices have been affected by the equity turmoil. But unlike the US indices, the European ones have already been sitting in the negative zone for the year. The FTSE 100 turned red around the end of August, DAX cannot get out of the negative zone since around the second half of June and the Euro Stoxx 50, like the FTSE 100, has also been in the red for the year from around August time. This is not mentioning the other big European indices like the CAC 40, the FTSE MIB and the rest that can’t get out of the yearly red as well.

But on a positive note, investors are now hoping that the late holiday rally would kick in and that the markets would recover at least some of the losses, or even close the year in the positive territory. Probably the tensed atmosphere in equities, for sure, will remain up until new year. The US dollar and the Japanese yen were among the big gainers, as investor started jumping into those currencies in order to find value.

Carney and May Were In The Spotlight Yesterday

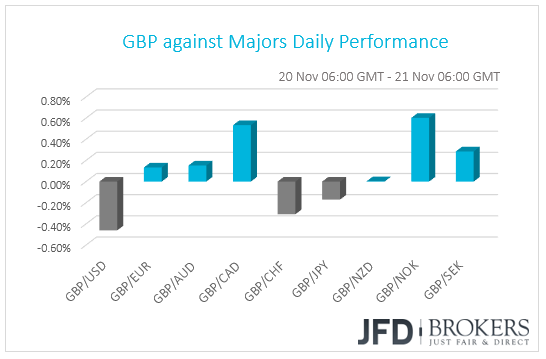

The Bank of England Governor Mark Carney delivered his testimony on the November Inflation Report in front of the Parliament’s Treasury Committee. Carney said that there won’t be much stability in the British pound, at least in the near term, due to the Brexit uncertainty, as this could increase the currencies amplitude against its other major counterparts. The Governor also said that because of the messy Brexit, the Bank fears that there could be a supply shortage, which could drive prices higher. In this case, the BoE will have to adjust the interest rate accordingly, which means raising it.

Yesterday, Theresa May flew to Brussels for a scheduled meeting for today with the European Commission President Jean-Claude Juncker. The meeting, of course, is around the rough Brexit deal, which the British Prime Minister is hoping to finalise. The meeting is set to start in the afternoon local time, which will be heavily monitored.

In Other Today’s News

during the US session, we get durable goods orders for October. Expectations are for headline orders to have declined 2.5% mom after rising 0.7% in September, while core orders, which exclude to volatile items of transportation, are forecast to have accelerated to +0.4% mom from +0.1%. That said, such prints will drive both the headline and core yoy rates lower, something supported by the slide in the New Orders sub-index of the ISM manufacturing PMI for the month. Existing home sales for October, as well as the final UoM consumer sentiment index for November, are also due to be released.

On the political front, the EU Commission will announce its decision over Italy’s resubmitted budget plan. Last week, Italy submitted its plans, keeping the growth and deficit forecasts untouched, something that makes another rejection by the Commission the most likely outcome. The question now is whether the EU will indeed proceed with imposing sanctions to the nation.

AUD/JPY – Technical Outlook

As always, our favourite market sentiment pair that we like to monitor is AUD/JPY, which sold off yesterday, together with the equity markets. Looking at the 4-hour chart, the pair started forming lower lows and lower highs, which indicates that AUD/JPY could be set for a further decline. For now, even though we are seeing a small recovery, still, this might just be considered as a correction before another leg of selling. Hence why we will stay bearish, at least in the short run.

Yesterday, the pair found good support near 81.30, which also coincides with the 200 EMA. AUD/JPY is rebounding right now, but as mentioned above, this could be a temporary move. If the pair struggles to overcome the 81.75 barrier, this could invite the bears to the table and push AUD/JPY back down to test the 81.30 level again. A break of that level would signal that not all is good in the bull-bloc and a further rate depreciation could be inevitable. This is where we may target the 81.00 hurdle, a break of which could open the way towards the 80.60 zone, marked by the high of the 10th of October.

Alternatively, a push above the 81.94 obstacle could spark some hope among the bulls, who in their case, could lift AUD/JPY higher towards the 82.20 resistance area, which is near yesterday’s high. A break above could lead the pair towards its next potential resistance at 82.63, marked by Monday’s high. This is where the pair could stall, as it would also hit the short-term downside resistance line drawn from the peak of the 8th of November.

![]()

DAX – Technical Outlook

DAX, together with the other global indices, had sold off yesterday, reaching its October lows again. Looking at our daily chart, the German cash index manged to retrace back up slightly, but at the time of this analysis is getting held by the 11150 resistance area, which just yesterday was seen as a good potential area of support. We will remain somewhat bearish for the near term, especially if we see a violation of the psychological 11000 level.

Certainly, the near-term outlook doesn’t seem to be leaning to the positive side. Even if DAX manages to retrace back up a bit more, the weakness that currently surrounds the global equity markets could continue pressuring the index and the bears could take advantage of the higher price and drive DAX back down again. A break of the 11050 hurdle, or even the psychological 11000, could open the path towards another very important support zone at 10825, which acted as a strong resistance level way back in October of 2016, before it got broken in the beginning of December of the same year. The German index had a strong rally from there onwards.

On the other hand, if the index gets back above the 11425 hurdle, marked by Monday’s high, this could invite more bulls and DAX might travel higher to test the 11700 zone, marked by the high of the 2nd of November. If that level is no match for the bulls, a further price acceleration could lead towards the 11850 obstacle, or the index could even test the medium-term downside resistance line, taken from the high of the 14th of June, which could halt DAX there for a while.

![]()

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2018 JFD Brokers Ltd.