Market sentiment improved somewhat yesterday afternoon, with the commodity currencies AUD and NZD gaining the most against USD. As for today, we have two G10 central banks deciding on interest rates: The Bank of Canada and the Riksbank. Expectations are for the BoC to hike, but for the Riksbank to stay on hold.

Risk Sentiment Improves Somewhat, but Concerns Remain

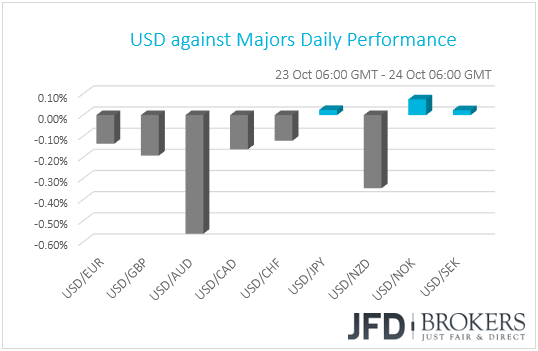

The dollar traded lower against most of the other G10 currencies on Tuesday. It lost the most ground against the commodity currencies AUD and NZD, while it gained fractionally only against NOK. The greenback traded virtually unchanged against JPY and SEK.

The comeback of AUD and NZD combined with the fact that JPY surrendered earlier gains to trade virtually unchanged against the US currency suggest that some risk appetite kicked in at some point during the day. Indeed, even though major EU and US indices ended their sessions in the red, US markets rebounded and closed well off their lows, while today, Japan’s Nikkei 225 and China’s Shanghai Composite Index closed in the green. Having said that though, we believe that it is too early to assume that the bad days are behind us. The drivers of the recent risk-off episodes are still in the front seat: Uncertainty surrounding Brexit and Italy, the US-China trade war, as well as expectations of more rate hikes by the Fed.

Speaking about Brexit, the pound spiked up yesterday following reports that the EU could offer Theresa May a UK-wide customs union in order to get closer in reaching an accord. However, although the British currency ended the day in positive territory versus its US counterpart, it quickly reversed the report-related gains, a move suggesting that the market remains skeptical as to whether any deal could get approved by May’s colleagues back in the UK. As we noted yesterday, recent developments suggest that the closer PM May gets in finding common ground with the EU, the harder it becomes for any accord to be approved back home.

Moving to Italy, the European Commission rejected the nation’s budget plans and asked the government to submit a new proposal within three weeks or face sanctions. The Commission noted that Rome would have to cut the structural deficit by 0.6 points rather than increase it as in the current draft, while Italy’s PM said he expected “frank and constructive” talks, adding that the budget deficit target of 2.4% “won’t be touched at the moment.” Although ahead of the decision a report suggested that Italy was ready to adjust its plans should markets react negatively, the fact that the EU asks for a 0.6-point reduction makes the case of an accord a hard task. Thus, we maintain our view that any gains in the euro, as well as in Italian assets, are likely to remain short lived, unless we see handshakes.

DAX Cash Index – Technical Outlook

During the European afternoon, the DAX cash index showed some good strength, where the bulls managed to lift it from its lows near 11225. At the time of this analysis, the German cash index is balancing slightly below its key resistance at 11450, which if broken, could lift the index a bit higher. But all this could still be seen as a correction, given that DAX remains below its short-term downside resistance line taken from the peak of the 4th of October.

For now, we will consider a possibility for DAX to move a bit higher, especially if it break above the 11450 zone, marked by the lows the 11th, 15th and 22nd October. This way, we could then target the aforementioned downside resistance line, which could be a good area for the bears to step in again and pull the price back down again. If the 11450 hurdle gets broken again, this time from above, then we could see the index traveling all the way towards the 11225 barrier, marked by yesterday’s low.

On the other hand, if the above-mentioned short-term downside line does not stop the price acceleration, then a break of it could lead to a test of the 11680 area, which held DAX from moving higher on the 22nd of October. If that area eventually gets broken, this is where could start getting more comfortable with the upside. We will then aim for a possible test of the 11855 obstacle, or even the psychological 12000 area again.

![]()

BoC Set to Hike, Riksbank Expected to Stand Pat

Apart from political developments, investors are likely to turn attention back to monetary policy today, as two G10 central banks decide on interest rates: The Bank of Canada and the Riksbank.

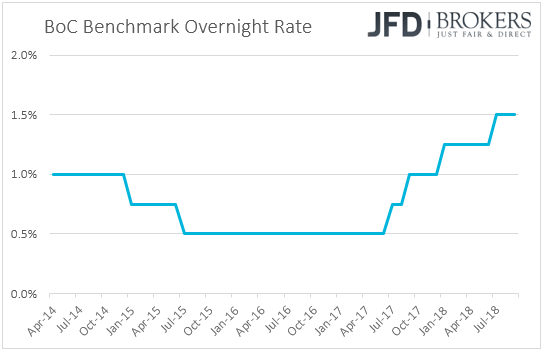

Kicking off with the Bank of Canada, expectations are for policymakers to raise the benchmark interest rate to +1.75% from 1.50%. This would be one of the bigger meetings and thus, given that a rate hike is widely anticipated, if it happens, the attention is likely to quickly turn to the accompanying statement, the updated economic projections and the press conference.

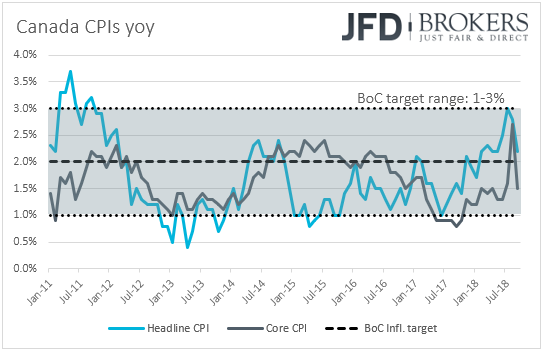

When they last met, Canadian policymakers remained willing to continue hiking rates if data continue to suggest so, but reiterated concerns over global trade tensions and the course of NAFTA negotiations. Since then, Canada and the US reached common ground over NAFTA, while data up until Friday were in support of a rate increase at today’s gathering. Nevertheless, on Friday, inflation data showed that the headline CPI rate dropped to +2.2% yoy from +2.8%, while the core rate slid to +1.5% yoy from 1.7%.

Even though officials themselves noted that they expected headline inflation to move back towards 2% in the months ahead, they believed that this would happen as the effects of past increases in energy prices dissipate. So, the fact that underlying inflation slowed as well suggests that this was not the case. Therefore, even if the Bank decides to raise rates by 25bps today, officials may strike a more cautious tone with regards to future hikes. For example, they could unearth the part saying that the “Governing Council will remain cautious with respect to future policy adjustments”, which was removed at the May meeting. This would characterize the decision as, what we call, a “dovish hike” and could bring the Lonnie selling interest.

Passing the ball to the Riksbank, at its previous meeting, the world’s oldest central bank kept interest rates on hold, noting that they will be held unchanged at the October gathering, and then raised either in December or February. Latest Swedish inflation data showed that both the CPI and CPIF rates rose by more than anticipated in September, but what’s more important in our view, is that the core CPIF metric, which excludes the volatile items of energy, accelerated to +1.6% yoy, its highest pace this year.

We believe that the better than expected inflation prints, and especially the strong rebound in the core CPIF rate, may have made a December hike even more likely and thus, it would be interesting to see whether the Bank will dismiss the February option, something that could prove positive for SEK. On the other hand, having in mind SEK’s surge after the inflation data, a reiteration that borrowing costs could rise either in December or February may disappoint those who brought forth their expectations, and the currency could tumble.

EUR/CAD – Technical Outlook

EUR/CAD is balancing slightly above its short-term tentative upside support line drawn from the low of the 3rd of October. Even though we saw the euro falling against the Canadian dollar since the beginning of this week, as long as the upside line remains intact, we will aim higher again in the short-term. Also, in support to the upside idea, the pair continues to form higher lows.

I nice good rebound from the aforementioned upside support line could lead EUR/CAD back up towards levels that recently acted as support and now could become resistance obstacles. The first one to watch there could be the yesterday’s high, at approximately 1.5053. If that doesn’t stop the bulls, then its break could send the pair towards a test of the 1.5115 area, or even the 1.5135 barrier, marked near the peak of the 11th of October.

The alternative scenario here would be if we see a break of the previously mentioned upside support line. But still, we would remain cautious, as we would wait for a possible break of the 1.4930 zone, which held the rate firmly from dropping lower on the 19th of October. Only then we could get comfortable in examining lower possible areas of support, like 1.4860, or even 1.4830. The last one is marked by the low of the 5th of October.

Both the RSI and the MACD are running flat. The RSI is balancing around 50 and the MACD is stuck near its zero line. Hence, we will wait until both indicators start building a clearer picture before we start considering them.

![]()

As for the Rest of Today’s Events

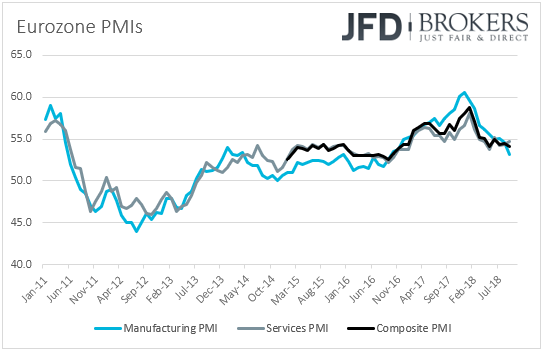

During the European morning, we get the preliminary manufacturing and services PMIs for October from several European nations and the Eurozone as a whole. Both the bloc’s manufacturing and services indices are expected to have declined, to 53.0 and 54.5 from 53.2 from 54.7 respectively, something that could drive the composite PMI down to 53.9 from 54.1. Even though, the services sector appeared to have stabilized somewhat in the second half of the year, manufacturing activity is set to experience its 10th consecutive slowdown.

We have preliminary manufacturing and services PMIs for October from the US as well. The manufacturing index is expected to have ticked down to 55.5 from 55.6, while the services one is forecast to have risen to 54.1 from 53.5. New home sales for September are also to be released and expectations are for a 1.4% slide following a 3.5% increase.

During the Asian morning Thursday, New Zealand’s trade balance for September is coming out and expectations are for the nation’s trade deficit to have narrowed somewhat.

As for the speakers, besides BoC Governor Poloz, we have three more on the agenda: St. Louis Fed President James Bullard, Atlanta Fed President Raphael Bostic, and Cleveland Fed President Loretta Mester.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.