There are no major economic indicators on today’s agenda, but we do have several central bank policymakers to hear from. Today, the ECB’s forum on central banking begins, while in the US, Fed Chief Jerome Powell is scheduled to testify before the Senate Banking Committee on the Fed’s policy response to the coronavirus pandemic. Other policymakers are also scheduled to speak throughout the week.

ECB Forum on Central Banking Begins, Fed Chair Powell Testifies

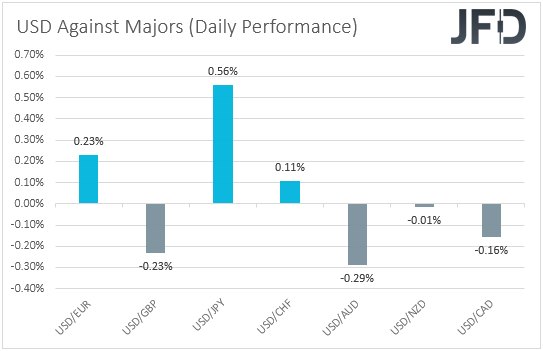

The US dollar traded mixed against the other major currencies on Monday and during the Asian session Tuesday. It gained versus JPY, EUR, and CHF in that order, while it underperformed against AUD, GBP, CAD. The greenback was found virtually unchanged versus NZD.

The weakening of the yen and franc, combined with the strengthening of the risk-linked Aussie and Loonie, suggests that financial markets may have traded in a risk-on manner yesterday and today in Asia. Indeed, major EU indices finished their session in positive territory yesterday, perhaps due to the absence of new negative headlines surrounding China’s Evergrande. However, the picture was different during the US session. The Dow Jones gained somewhat, but the S&P 500 and the Nasdaq traded lower, dragged by tech stocks, which slid due to rising Treasury yields. Remember that high-growth stocks are valued based on discounted estimated future cash flows, and thus, rising interest rates result in a lower present value. Today, in Asia, sentiment was more mixed. Japan’s Nikkei225 and South Korea’s KOSPI slid, but China’s Shanghai Composite and Hong Kong’s Hang Seng edged north.

Today, although we don’t have any major indicators on the schedule, we do have several central bank policymakers to hear from, remarks of whom may reshape market expectations around monetary policy. In the Eurozone, ECB’s forum on Central Banking will start today, and the speakers’ agenda includes Fed Chief Jerome Powell, BoE Governor Andrew Bailey, and BoJ Governor Haruhiko Kuroda. They probably speak tomorrow, but we will stay alert on any early comments today. Other policymakers are also scheduled to speak throughout the week. On top of that, Fed Chair Powell will testify before the US Congress on the Fed’s policy response to the pandemic. He will speak before the Senate Banking Committee today, while tomorrow, he will present the same testimony before the House Financial Services Committee.

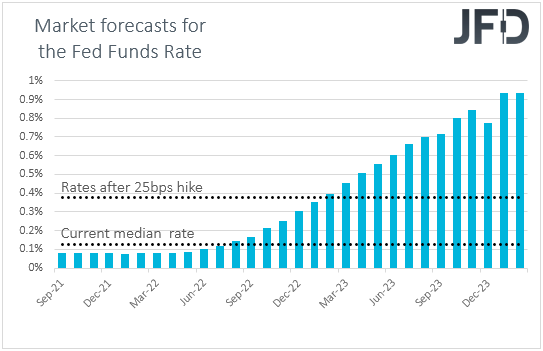

Last week, the Fed confirmed that QE tapering is likely to start this year, with investors hoping that this will happen as early as in November. Thus, remarks adding credence to that view may result in further dollar buying. Having said that though, yesterday, Fed members Brainard and Evans highlighted the importance of the labor market in taking a tapering decision. Therefore, whether (or not) the Fed will taper in November may also depend by the September employment report, scheduled to be released next Friday.

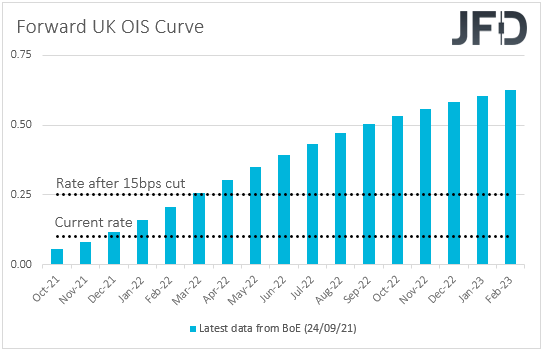

In the UK, the BoE appeared more hawkish than expected, encouraging participants to bring forth their rate-hike expectations. Therefore, it would be interesting to see whether we will get any hints on when the first hike may take place. According to the latest data on the forward curve of the UK OIS (Overnight Index Swaps), the market is pricing in a 15bp hike to be delivered in March 2022. So, anything suggesting that this may happen earlier could support the British pound, especially against currencies the central banks of which are forecast to stay accommodative for longer, the likes of the euro, the Aussie and the yen. That said, the Aussie and the yen are more sensitive to developments surrounding the broader market sentiment. Thus, we would prefer to study them against each other, as when market sentiment improves, AUD/JPY marches higher, while the opposite is usually true when risk appetite deteriorates. Indeed, yesterday, when appetite improved, AUD/JPY was the best performing cross, consisting of major currencies.

With regards to the ECB, officials of this Bank announced a “moderately lower pace” in their Pandemic Emergency Purchase Program (PEPP) purchases but made it clear that this is not a tapering move, and that when PEPP is over they have all the other tools available. With that in mind, we look for any comments as to whether the Bank intends to compensate by buying more through other schemes, like the Asset Purchase Program (APP). This will keep the ECB near the dovish end of the central bank spectrum and may result in some more euro-selling, at least against the US dollar, if indeed Fed policymakers are willing to start tapering in November, and sound more hawkish on interest rates.

As far as the BoJ is concerned, there is not much to anticipate, as Japanese policymakers have been stuck with extra loose monetary policy, showing no intention to proceed with any changes any time soon.

EUR/USD – Technical Outlook

EUR/USD traded lower yesterday, to hit support once again near the 1.1683 barrier today in Asia. Although it has yet to confirm a forthcoming lower low since Thursday, it continues to trade below all three of our moving averages on the 4-hour chart, but more importantly, below the downside resistance line taken from the high of September 3rd. Therefore, we stick to our guns that the short-term picture is negative.

A clear dip below 1.1683 will confirm a forthcoming lower low and may initially target the 1.1665 zone, defined as a support by the lows of August 19th and 20th, the break of which could carry larger bearish implications. It could allow the bears to shoot for the 1.1620 area, marked by the low of November 2nd, 2020.

On the upside, in order to start examining a reversal, we would like to see a break above 1.1749. This will not only confirm a forthcoming higher high on the 4-hour chart, but it may also confirm the break above the aforementioned downside line. The bulls may then get encouraged to climb towards the 1.1790 or 1.1797 areas, marked by the high of September 17th and the inside swing low of September 14th respectively. Now, if neither barrier is able to stop the advance, we may experience extensions towards the 1.1832 level, defined as a resistance by the high of September 15th.

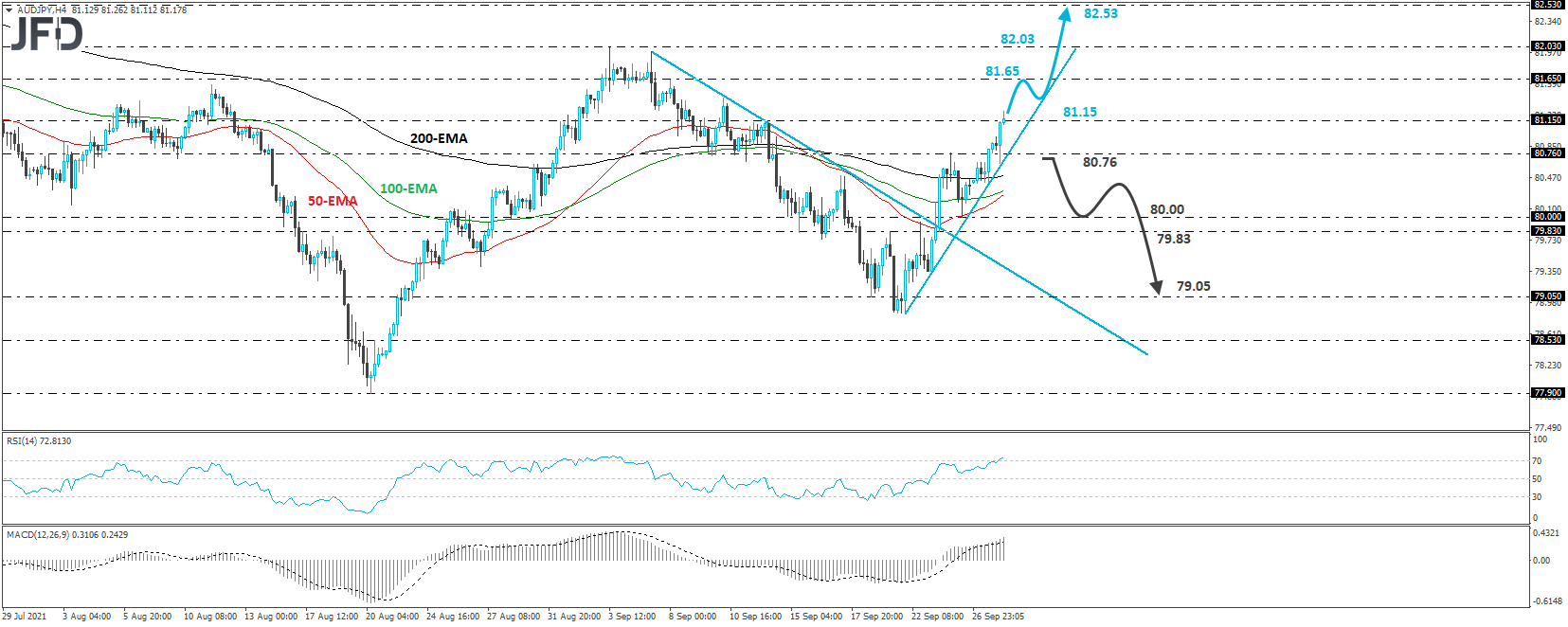

AUD/JPY – Technical Outlook

AUD/JPY traded higher yesterday, and early today, it managed to poke its nose above the 81.15 level, marked by the high of September 14th. Although changes in the broader market sentiment could result in volatile swings in and very short-term trends in this exchange rate, technically speaking, the near-term picture looks relatively positive. The pair has been printing higher highs and higher lows above an upside line since last Wednesday.

The move above 81.15 may have opened the path towards the 81.65 level, marked by the high of September 8th, the break of which could aim for the peak of September 3rd, at 82.03. If that level is not able to hold the advance, then we may see the rate rising towards the 82.53 hurdle, marked by the high of July 14th.

Now, a clear break below 80.76 could signal the end of last week’s uptrend and may invite more bears into the action. This could result in a slide towards the 80.00 mark, which supported the rate on Friday, or the 79.83 zone, marked by the inside swing high of September 21st. Another break, below 79.83, could set the stage for declines towards the 79.05 territory, marked by the low of September 20th.

As for the Rest of Today’s Events

The only data releases worth mentioning are the US Conference Board consumer confidence index for September, which is expected to have risen to 114.5 from 113.8, as well as the API (American Petroleum Institute) report on crude oil inventories for last week, but as it is always the case, no forecast is available.

Tonight, or better say, tomorrow in Asia, we have the leadership elections of Japan’s ruling Liberal Democratic Party (LDP), the winner of which will succeed Yoshihide Suga as a Prime Minister as well. However, he may not hold that position for long as national elections will take place on or before November 28th. Taro Kono appears to be the favorite, a candidate that supports a spending package that focuses on boosting wages and growth. However, we don’t expect Japanese markets to react massively on the outcome. Remember that in the days after Suga’s announcement that he will step down, Japan’s Nikkei 225 surged almost 12%, suggesting that investors have already cheered the prospect of better days with a new PM.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.90% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.