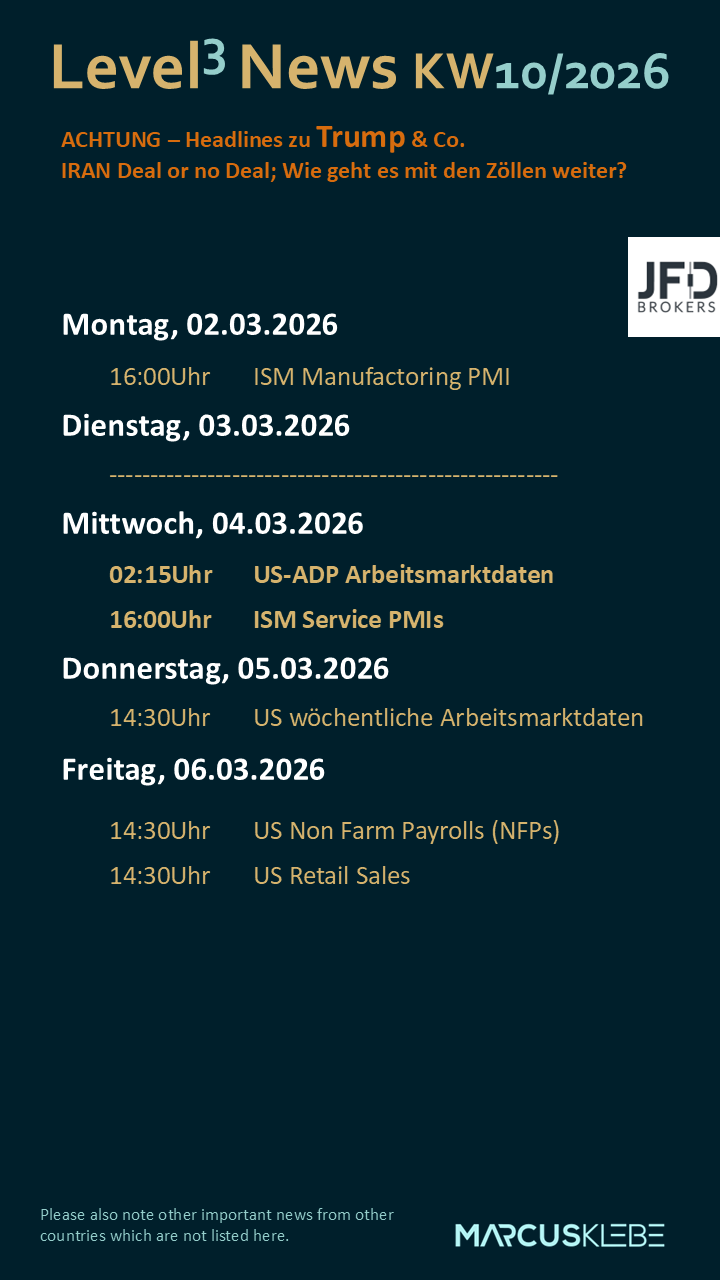

The coming week features several closely monitored US economic indicators, including PMI readings, ADP employment data and Friday’s Nonfarm Payrolls, which may offer additional insight into current economic conditions. At the same time, geopolitical tensions between the United States and Iran remain elevated. Ongoing negotiations are accompanied by uncertainty regarding regional stability, which may contribute to increased volatility across financial markets.

The coming week brings several closely monitored US economic indicators that may provide additional insight into current economic conditions. Early in the week, attention will turn to the ISM Manufacturing and Services PMIs, which offer a snapshot of activity in the industrial and service sectors. These forward-looking surveys are widely regarded as leading indicators, as they can provide early indications of trends in production, new orders, and employment.

On Wednesday, the ADP employment report will be released, providing an additional data point on private-sector labor market conditions ahead of Friday’s official figures. Although ADP results do not always align with the government report, they can influence market expectations for the upcoming Nonfarm Payrolls release. Retail Sales data, also scheduled during the week, may offer insight into consumer spending, which represents a significant component of overall economic activity.

Friday’s Nonfarm Payrolls report is one of the most closely monitored economic releases each month. The report includes payroll growth, wage data and the unemployment rate, all of which can influence market expectations regarding Federal Reserve policy. Following several months of relatively stable labor market data, market participants will assess whether recent trends persist.

While macroeconomic releases will dominate the economic calendar, geopolitical developments continue to contribute to broader market uncertainty. Tensions between the United States and Iran remain elevated, while diplomatic negotiations over Iran’s nuclear program are ongoing, fundamental disagreements remain unresolved.

Media Reports indicate adjustments to US military deployments in the region, including the repositioning of certain naval and air assets. While some commentators view these developments as a sign of rising geopolitical risk, no official confirmation of potential military action has been provided. Discussions regarding possible outcomes remain speculative, contributing to heightened uncertainty in global markets.

Public statements from US officials have reflected differing perspectives regarding potential policy responses. While some representatives have sought to downplay the prospect of an extended military engagement, broader strategic options have not been formally ruled out. Financial markets may respond to geopolitical developments of this nature, particularly in energy markets, given Iran’s role in global oil supply.

For financial markets, the combination of key economic releases and geopolitical risk creates a complex environment. Strong PMI and employment data could reinforce expectations that the Federal Reserve maintains a relatively restrictive stance, which may influence valuations across risk sensitive assets. Conversely, weaker data may prompt renewed discussion regarding potential policy easing and could be viewed more positively by equity markets.

Energy markets can be particularly sensitive to geopolitical events. The prospect of heightened tensions may influence oil price movements, reflecting Iran’s position as an exporter and its proximity to the Strait of Hormuz, a key transit route for a substantial portion of global oil shipments.

Recent market reactions reflect this crosscurrent. Higher US crude inventories have conceded with softer price dynamics, while geopolitical uncertainty may contribute to a risk premium in oil markets. This interaction highlights the extent to which energy prices can respond to both macroeconomic fundamentals and political developments.

In summary, the upcoming week presents a complex combination of macroeconomic released and geopolitical developments. PMI releases, ADP figures, Retail Sales, and Friday’s Nonfarm Payrolls are likely to be likely to market expectations regarding the US economy and Federal Reserve policy. At the same time, ongoing tensions between the United States and Iran may contribute to elevated uncertainty, which in turn could lead to increased volatility across various asset classes.

Investors and traders will therefore need to monitor not only the economic data but also the evolving political landscape. The interaction between macroeconomic fundamentals and geopolitical factors may play a significant role in shaping market sentiment in the days ahead.

Risk warning:

This is a marketing communication. The content is provided for informational purposes only and does not constitute investment advice, investment research, or a personal recommendation, nor should it be construed as an offer or solicitation to buy, sell, or hold any financial instrument. This communication has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

The information presented does not take into account your individual investment objectives, financial situation, or needs. You should assess whether any investment is appropriate for you.

Investors are solely responsible for any investment decisions and should consider obtaining independent professional advice tailored on to their personal financial situation, investment objectives and risk tolerance before taking any investment decision. Duplication, distribution or publication of this content is prohibited without explicit approval.

59.18% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Trading in cash equities involves risk. The value of investments may go down as well as up. Past performance is not a reliable indicator of future results. Please read the full Risk Disclosure available on our website.