Yesterday, the big winner among the G10 currencies was JPY, which came under buying interest during the Asian session Wednesday following the release of the Summary of Opinions for last week’s BoJ gathering. The main loser was the Kiwi. It came under selling interest after the RBNZ pushed further back the timing of when its expects interest rates to start rising.

Yen Gains After BoJ Summary of Opinions

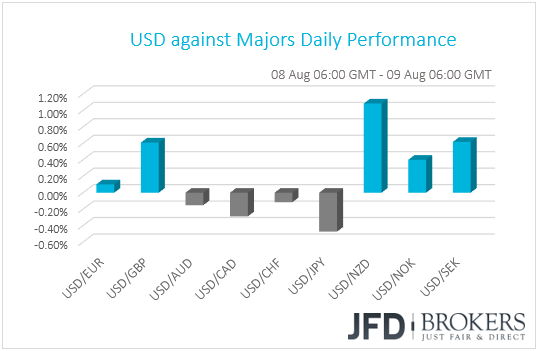

The dollar traded mixed against the other G10 currencies on Wednesday. It gained against NZD, SEK, GBP and NOK in that order, while it lost ground versus JPY, CAD and AUD. The greenback ended the day virtually unchanged against EUR and CHF.

The winner of the day was the Japanese yen, which came under buying interest during the Asian session Wednesday following the release of the Summary of Opinions for last week’s BoJ gathering. The Summary revealed that a couple of members wanted to allow long-term yields to fluctuate within double the ±0.1% range, while one member suggested that the Bank should allow yields to move up or down by around 0.25%. Although at the press conference following decision, Governor Kuroda announced that the Bank will allow yields to fluctuate within a ±0.2% range, the fact that one member advocated for a wider range may have prompted some market participants to increase bets that the BoJ is turning more hawkish. This could be the case, especially following Tuesday’s report citing sources saying the reflationists within the Bank have become a minority and that there were even plans to raise rates twice this year.

That said, even if this is the case, even if the Bank is turning more hawkish, we stick to our guns that with all metrics of Japanese inflation well below the Bank’s 2% objective, it could be very hard for policymakers to proceed with a meaningful step towards normalization any time soon. Seen in isolation, the fact that the BoJ kept its policy program ultra-loose, albeit more flexible, should work against of the yen, especially versus currencies like USD and CAD, the central banks of which are expected to continue raising rates. That said, with market attention firmly focused on the US-China trade conflict, it’s difficult for someone to play the theme of monetary policy divergence between the BoJ and other, more hawkish, central banks. During periods of escalating tensions, investors abandon riskier assets and seek shelter in safe haven assets, one of which is the yen.

CAD/JPY – Technical Outlook

CAD/JPY had been trading within a rising wedge formation for quite a while, but on the 7th of August it broke through its lower bound. Now we can see that the bulls are trying to fight back and take the pair back up again, but this move higher could be short-lived, as the pair could meet its strong resistance either at 85.35, or at the lower side of the aforementioned wedge. This is where we expect the bears to jump in again and try to drive CAD/JPY lower.

If CAD/JPY gets rejected at the abovementioned levels and then moves lower to test the 85.00 hurdle again, a break of that hurdle could lead to a drop to the 84.70 zone, marked near yesterday’s low. If that zone is not able to withhold, then a further decline could open the way to the 84.45 or the 84.25 levels, with the last being the low of the 24th of July.

Alternatively, if CAD/JPY moves back into the wedge formation, this is where we could start examining higher levels. The next good area of resistance to monitor could be the 85.85 barrier, marked by the high of the 7th of August. Above that lies the other good area of resistance at 86.25, which was near the high of the 1st of August. If that area doesn’t stop the rate from accelerating further, then the pair could test the upper bound of the aforementioned wedge formation, where we could see the rate stalling for a while, until the bulls and the bears decide on who will take control from there onwards.

![]()

RBNZ Keeps Rates Unchanged, Pushes Hike-timing Further Back

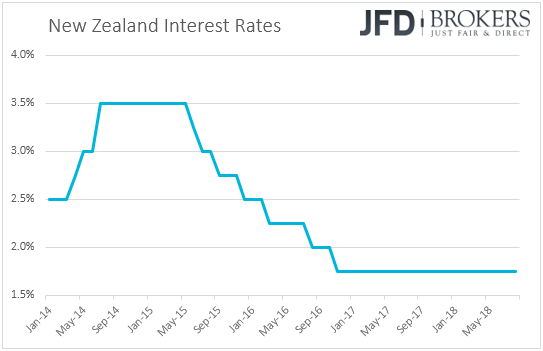

The Kiwi was the G10 currency that got hit the most, coming under massive selling pressure following the RBNZ monetary policy decision. The Bank decided to keep interest rates unchanged at +1.75% as was widely anticipated, reiterating that the direction of the next move could be up or down. That said, in the accompanying statement, Governor Orr noted that policymakers expect to keep rates at this level through 2019 and into 2020, longer that it was projected in the May quarterly Monetary Policy Statement. According to the Bank’s new projections, interest rates are now expected to start rising in September 2020. The previous path was for rates to begin rising in September 2019.

As for the rest of the forecasts, officials downgraded somewhat their growth projections for this year, but upgraded them for the next one, while they now expect inflation to hit the midpoint of their 1-3% target range in March 2021, compared to December 2020 in the May Statement.

At the press conference following the decision, Governor Orr said that if growth slows further below its potential rate, then officials would have to cut rates, while in a Reuters interview thereafter he noted that the Bank needs to make sure it is “blowing winds into sails” of the economy for some time yet. If there is a deterioration in growth we might have to “blow more wind”, he added.

As for our view, with a Bank giving so much emphasis on the possibility of a cut and pushing one year back the timing for when it expects interest rates to start rising, we expect the New Zealand dollar to stay under selling interest. What’s more, given that the New Zealand economy is heavily reliant on exports to China, the US-China trade conflict is likely to keep pressure on the Kiwi as well.

EUR/NZD – Technical Outlook

Following the RBNZ, the New Zealand currency tumbled against most of its majors, including the Euro. We can see that EUR/NZD had a strong spur to the upside, breaking some key resistance levels on its way. Before yesterday, the pair was trading below its short-term downside resistance line, taken from the peak of the 3rd of July. But once the RBNZ statement came out, the pair blew up higher.

For now, we will stick to the upside and aim for the next potential area of resistance at the 1.7480 zone, which was the highest point of December last year. But before EUR/NZD could get there, it could retrace back down a bit, so that the bulls could take advantage of the lower levels and use those as entry points. For us, a good confirmation of a possible retracement could be a rejection near the 1.7375 barrier, which was the high of the 3rd of July. In this case, we could then target the 1.7335 level, or even the 1.7300 hurdle, marked by the highs of the 8th of August and the 20th of July, respectively. The last area that may act as a good bouncing ground could be the aforementioned broken downside resistance line.

For us to join the bears and start examining lower levels, we would need to see a break and a close below that abovementioned downside line. The move could lead EUR/NZD back down towards the 1.7185 level, from which yesterday the pair rocketed to the upside. If that level does not hold, then a further decline could test the important zone between the 1.7130 and 1.7115 marks that acted as strong support since mid-July.

![]()

As for Today’s Events

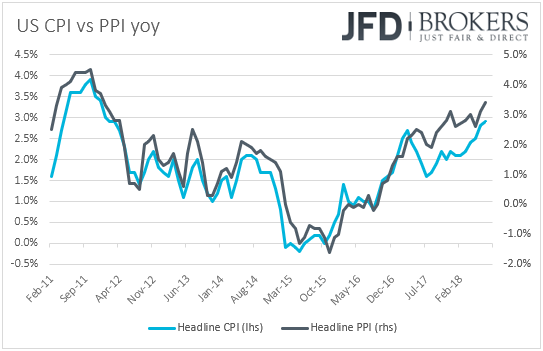

The US PPIs are coming out. Expectations are for both the headline and core PPI rates to have declined to +3.2% yoy and +2.6% yoy, from +3.4% and 2.8% respectively. Slowing producer prices could result slowing consumer prices and thus, these prints could raise some speculation that the CPIs, due out on Friday, may follow suit. Initial jobless claims for the week ended on the 3rd of August are due to be released as well. Expectations are for a minor increase to 220k from 218k the previous week, something that would drive the 4-week moving average up to 219.7k from 214.5k.

Tonight, during the Asian morning Friday, we get Japan’s preliminary GDP for Q2. Expectations are for a rebound to +0.3% qoq after a 0.2% slide in Q1. This is likely to drive the yoy rate up to +1.4% from -0.6%.

We also have one speaker on the schedule: Chicago Fed President Charles Evans.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.