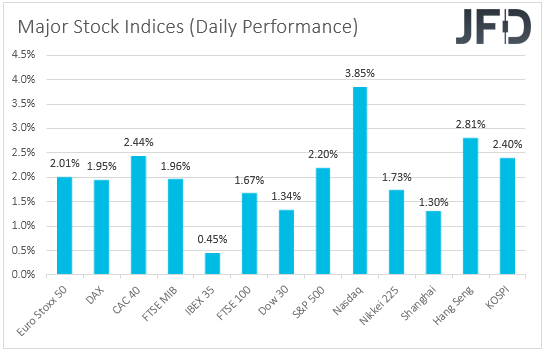

Global equities were a sea of green yesterday and during the Asian session today as Joe Biden widened his lead against Donald Trump in winning the US elections. Although we saw a Biden victory as somewhat negative for Wall Street, US equities gained as well due to the fact that Republicans appear likely to retain majority in the Senate. During the early EU trading hours, the BoE decided to expand its QE by more than expected, while later in the day, the central bank torch will be passed to the Fed.

Equities Gain as Biden is Seen More Likely to Win

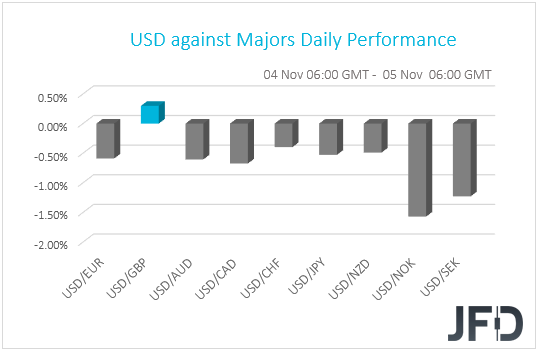

The US dollar traded lower against all but one of the other G10 currencies on Wednesday and during the Asian morning Thursday. It lost the most ground versus NOK, SEK, and CAD in that order, while it eked out some gains only versus GBP.

The weakening of the dollar suggests that markets continued trading in a risk-on fashion. Indeed, turning our gaze to the equity world, we see that major EU and US indices were a sea of green with the positive investor appetite rolling into the Asian session today.

The reason behind the advance in equities outside the US may have been the fact that Biden widened his lead against incumbent President Trump. At the time of writing, Biden has 264 electoral votes and Trump 214 in a race to 270. Although Trump is leading in Georgia, North Carolina and Pennsylvania, Biden is ahead in Nevada, which could give him the 6 votes needed to win the race.

We’ve been repeatedly noting that a Biden victory could be positive for equities outside the US, but we also said that it could prove negative for Wall Street due to his pledge for higher corporate taxes and tighter financial regulation. So, why did US stocks gain yesterday? This may have been due to the fact that Republicans appear likely to retain majority in the Senate, something that will make it hard for Biden to proceed with the tax increases and stricter regulations he promised. Thus, even if Biden wins, US indices may continue marching higher. The reason why a Biden victory is positive for equities around the rest of the world is because the Democrat is likely to adopt a softer stance on international trade relationships than Trump.

In the FX world, Biden is seen as negative for the US dollar due to his fiscal agenda being looser than Trump’s, but with Republicans staying in control of Senate, he may not be able to push through with his plans. Thus, we don’t expect a major slide. For the same reasons we believe that global equities will gain, we see the risk-linked currencies Aussie and Kiwi strengthening as well, as investors abandon safe havens, like the Japanese yen.

BoE Expands QE More than Initially Anticipated

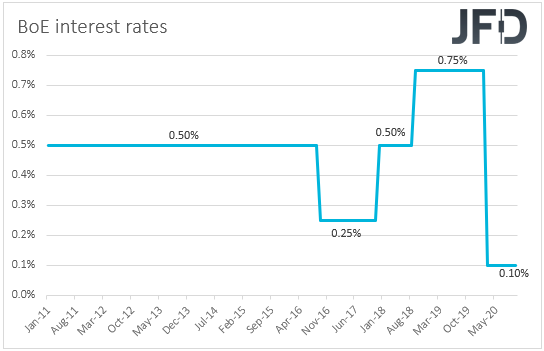

Apart from headlines surrounding the US election, during the early European morning, we also had a BoE monetary policy decision. The Bank decided to keep interest rates unchanged at 0.10%, but expanded its asset purchase program by more than initially expected. According to economic calendars, expectations were for a GBP 100bn increase, but instead, the Bank decided to go for a GBP 130bn expansion. In the statement accompanying the decision officials noted that the outlook for the economy remains unusually uncertain and that they stand ready to increase QE again if market functioning worsens.

The pound gained on the decision and this is because it had already tumbled yesterday on reports saying that the BoE is considering a move into negative interest rates and that it could expand its QE program by GBP 150bn to GBP 200bn. Moving ahead, we believe that the pound’s faith is likely to stay mostly linked to developments surrounding the Brexit landscape. Negotiations over a post-Brexit trade accord between the UK and the EU continued last week, with EU chief negotiator Michel Barnier saying that the two sides are working hard to reach consensus. With all that in mind, anything suggesting that a deal could be found in the next few weeks may prove supportive for the currency, while signs that the differences-gap is not narrowing may result in weakness.

Fed to Take the Central Bank Torch

Later in the day, it will be the Fed’s turn to decide on policy. At its most recent meeting, the Committee kept its policy unchanged, but changed its inflation language noting that they “will aim to achieve inflation moderately above 2% for some time so that inflation averages 2% over time”. With regards to the new dot plot, it showed that interest rates are likely to stay at present levels at least through 2023. That said, looking at the details, we see that one member was in favor of a hike in 2022, and four saw rates higher in 2023. Combined with the inflation forecast of 2023, which is at 2%, this shows that some members may not be willing to tolerate inflation above target for long as pointed in the decision statement.

With that in mind, and also taking into account that the US economy continues to relatively improve, despite the spike in coronavirus infections, we believe that policymakers can afford staying sidelined at this gathering. Thus, investors may scan the statement for clues and hints as to how officials are likely to proceed in the months to come. If officials hint that there are high chances for further easing at the December gathering, the US dollar is likely to slid, while it could gain somewhat in the absence of such wording. In any case, we believe that its broader path will still be affected by the election outcome, and any post-FOMC reaction could stay limited and short-lived.

DAX – Technical Outlook

From the last trading days of October, the German DAX index has been moving comfortably to the upside. Yesterday, the price jumped above a short-term downside resistance line taken from the high of October 12th. At the same time, the index continues to balance above a short-term tentative upside support line drawn from the low of October 30th. As long as DAX stays above both of those lines, we will remain positive, at least with the near-term outlook.

A further push north could bring the price closer to the 12456 and 12505 levels, marked by an intraday swing low of October 22nd and the low of October 23rd. In between those two hurdles is the 200 EMA on our 4-hour chart. In a way, that whole area might provide a bit of a hold-up for DAX. The index could even retrace back down a bit, but as we mentioned above, if it stays above both of the aforementioned trendlines, we will remain positive. If another uprise is able to overcome the 12505 obstacle, the next possible target might be at 12723, which is marked by the high of October 23rd.

Alternatively, if the index suddenly falls sharply, breaks the previously-discussed upside line and slides somewhere below the 11960 hurdle, marked by the high of October 28th, that could attract more sellers into the game, as such a move might increase DAX’s chances of moving back down again. If so, we will then target the next possible support area between the 11785 and 11709 levels, which mark the low of November 4th and the high of October 29th. If that area is just seen as a temporary pit-stop for the sellers, a further push south might bring the price to the 11460 zone, marked by the low of October 29th and an intraday swing low of October 30th.

![]()

GBP/USD – Technical Outlook

GBP/USD moved higher this morning, after the BoE announcement. Despite still trading below a short-term tentative downside resistance line taken from the high of October 21st, the pair still has a good chance of drifting higher, if the price momentum stays in the positive territory on the RSI and the MACD. In order to get a bit more excited with slightly higher areas, we would prefer to wait for a push above the 1.3050 barrier first.

A strong move above the 1.3050 zone, which is an intraday swing high of yesterday, that may help push GBP/USD to its next possible resistance area, at 1.3079, which marks the high of October 27th and an intraday swing high of November 3rd. The rate may stall there for a bit, but if the buyers are still active, the next potential target might be the aforementioned downside line, which could provide additional resistance.

On the other hand, a strong drop below the 1.2938 hurdle, marked by the current low of today, may open the door fur further declines. We will then aim for the 1.2914 obstacle, a break of which might set the stage for a move to the 1.2855 level, marked by the current lowest point of November.

![]()

As for the Rest of Today’s Events

Besides the BoE and Fed meetings, we also get Eurozone’s retail sales for September and the US initial jobless claims for last week. The Euro-area retail sales are forecast to have slid 1.0% mom after rising 4.4% in August, while initial jobless claims are expected to have declined somewhat, to 732k from 751k.

We also have 5 speakers on the agenda: BoE Governor Andrew Bailey and Fed Chair Jerome Powell will hold press conferences related to their Bank’s decisions. We will also get to hear from ECB Vice President Luis de Guindos, ECB Governing Council member Jens Weidmann, and ECB Executive Board member Isabel Schnabel.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.57% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2020 JFD Group Ltd.