Major global equity indices traded north on Thursday and during the Asian session Friday, with all three of Wall Street’s main indices hitting new all-time highs. It seems that investors continued cheering the Democrats’ victories in the runoff elections in the US state of Georgia. As for today, the main event on the agenda is the US employment report for December. We also get jobs data for the month from Canada as well.

Equities Gain Ahead of the US Jobs Data

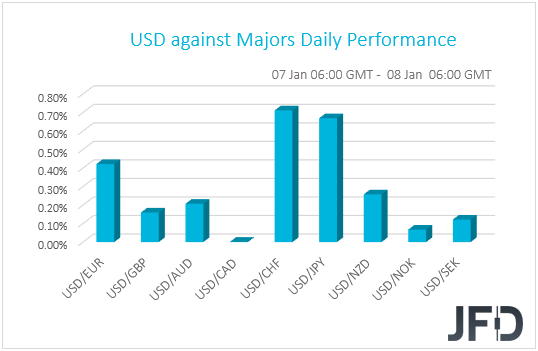

The US dollar traded higher against all but one of the other G10 currencies on Thursday and during the Asian session Friday. It gained the most versus CHF, JPY, and EUR in that order, while it eked out the least gains against NOK and SEK. The greenback was found virtually unchanged against CAD.

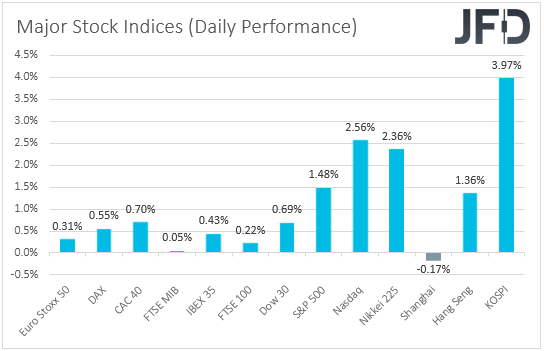

The strengthening of the US dollar and the weakening of the risk-linked Aussie and Kiwi suggest that markets traded in a risk-off fashion yesterday and today in Asia. Nonetheless, the weakening of the safe-havens yen and franc points otherwise. Thus, in order to get a clearer picture with regards to the broader market sentiment, we prefer to turn our gaze to the equity world. There major EU and US indices were a sea of green, with all three of Wall Street’s main indices hitting new all-time highs. The upbeat morale rolled over into the Asian session as well, with the only exception being China’s Shanghai Composite, which slid 0.17%.

It seems that investors continued cheering the Democrats’ victories in the runoff elections in the US state of Georgia. Now, with a Democrat-controlled Congress, President-elect Biden’s fiscal agenda may pass much more easily, which means more stimulus and infrastructure spending. It also means higher taxes and more regulation, which is negative for stocks, but we still believe that due to the coronavirus vaccinations, the fiscal support in the US, the monetary policy easing around the globe, and the Brexit trade accord, the path of least resistance for equities and other risk-linked assets may be to the upside.

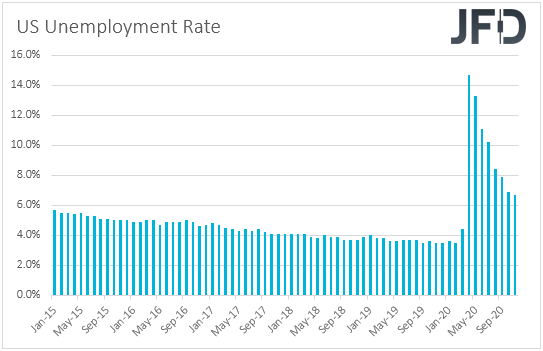

As for today, the main event on the agenda is the US employment report for December. Non-farm payrolls are expected to have slowed to 71k from 245k in November, but bearing in mind that, on Wednesday, the ADP reported that the private sector has lost 123k jobs, we would consider the risks as tilted to the downside. Although the ADP is far from a reliable predictor of the NFPs, it is the only major gauge we have. The unemployment rate is forecast to have ticked up to 6.8% from 6.7%, while average hourly earnings are forecast to have slowed to +0.2% mom from +0.3% mom. Barring any revisions to the prior monthly prints, this is likely to leave the yoy rate unchanged at +4.4%.

The minutes from the latest FOMC meeting revealed that some participants noted that they could consider further adjustments to their QE purchases, such as increasing the pace of purchases, or weighting them towards longer maturities. That said, other members said that once progress towards their goals had been attained, a gradual tapering could begin. In our view, a soft employment report could increase the chances for more monetary-policy support, which could prove negative for the US dollar. The big question is how equities will react. On the one hand, they could slide on signs of a weaker labor market, while on the other, they could gain on expectations of more support by the Fed. That said, whatever the reaction is, we stick to our guns that the overall path remains positive and we would expect equities to continue marching north in the near-term, even if they correct lower on a soft employment report.

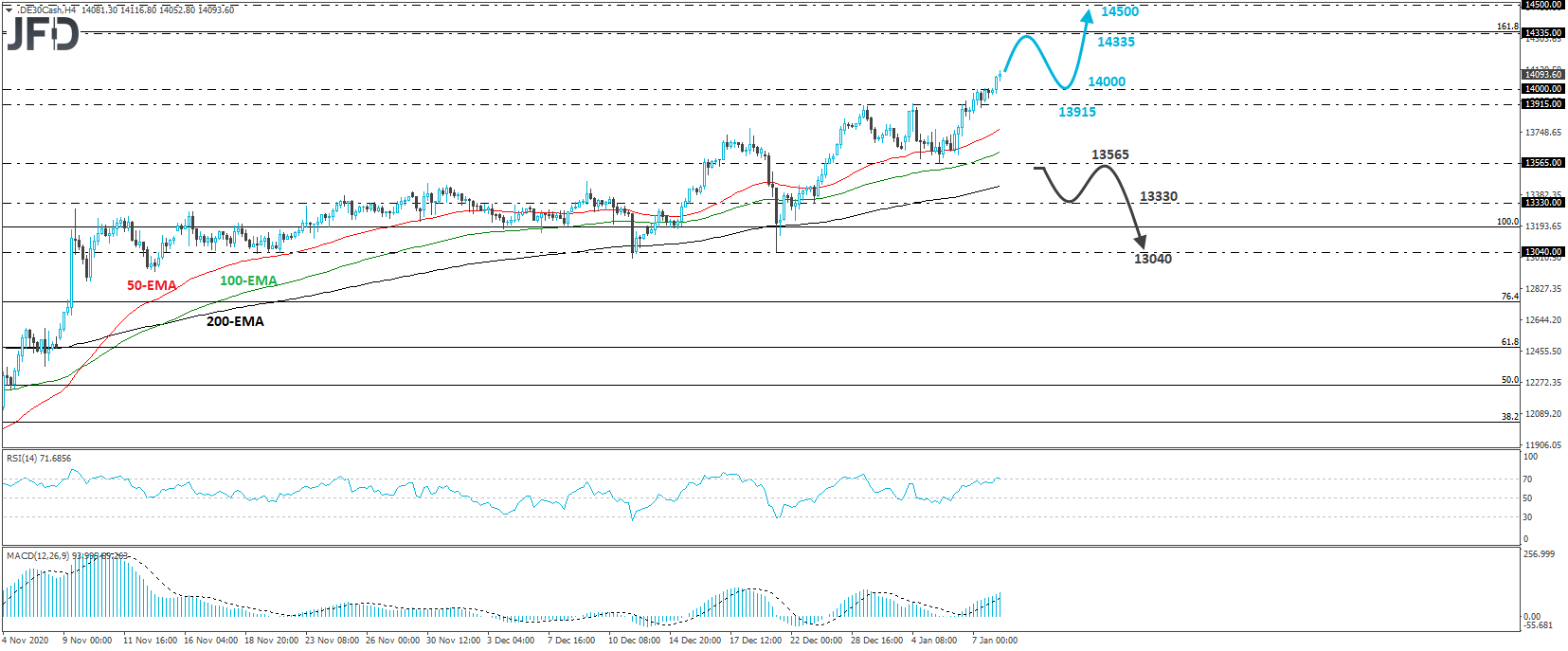

DAX – Technical Outlook

The German DAX cash index traded higher today, entering uncharted territory and breaking above the psychological round number of 14000. Overall, the price structure of this index remains of higher peaks and higher troughs and thus, we would consider the near-term outlook to be positive.

We believe that the break above 14000 may have opened the path towards the 14335 zone, which is the 161.8% extension level of the October 12th – October 30th slide. If that barrier is not able to stop the advance, then the next territory to pay attention to may be the next psychological barrier, at 14500.

In order to abandon the bullish case, we would like to see a retreat back below 13565, a support marked by the low of January 5th. Such a move would confirm a forthcoming lower low and may initially pave the way towards the low of December 23rd, at around 13330, the break of which may extend the decline towards the low of December 21st, at 13040.

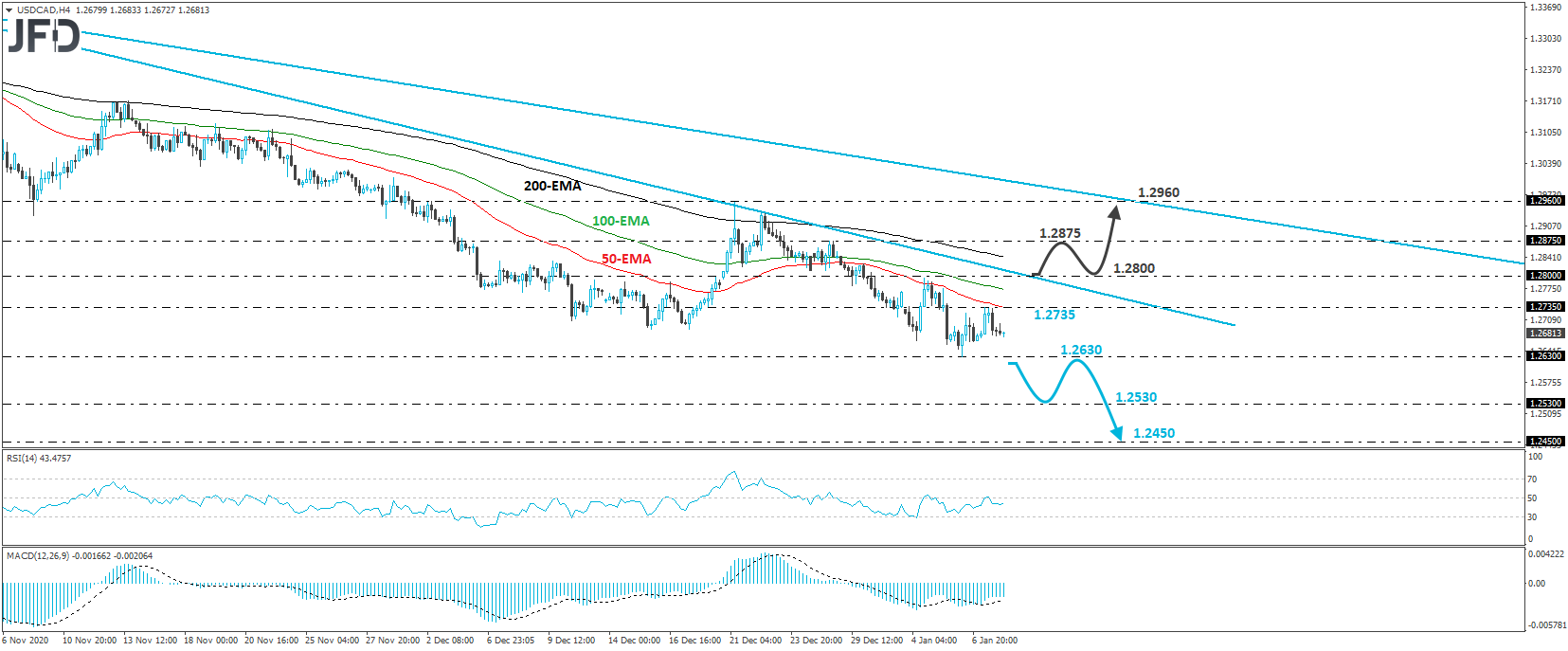

USD/CAD – Technical Outlook

USD/CAD traded higher yesterday, but hit resistance at 1.2735 and then, it pulled back. Overall, the pair is trading below a short-term downside resistance line drawn from the high of October 29th, as well as below a medium-term one taken from the high of March 19th. In our view, these technical signs paint a negative picture.

A clear and decisive dip below 1.2630 would confirm a forthcoming lower low and perhaps signal the continuation of the prevailing downtrend. The bears may then get encouraged to push the battle towards the 1.2530 barrier, which is marked as a support by the low of April 16th, 2018, the break of which may allow extensions towards the low of February 16th, 2018, at 1.2450.

On the upside, a break above 1.2800, marked by the high of January 4th, may signal the start of a decent corrective phase, as it would take the rate above the aforementioned short-term downside line. The bulls may initially target for the 1.2875 zone, marked by the high of December 28th, where another break may see scope for extensions towards the crossroads of the 1.2960 resistance and the downside line taken from the high of March 19th.

As for the Rest of Today’s Events

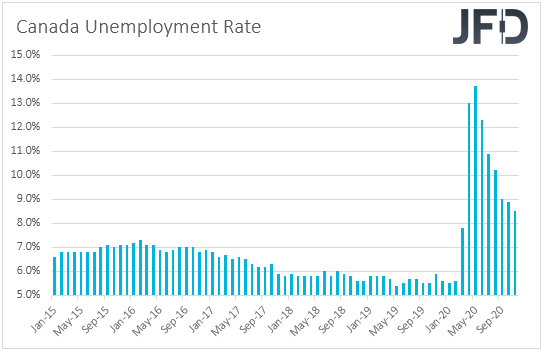

At the same time with the US employment report, we get jobs data from Canada as well. The unemployment rate is expected to have inched up to 8.6% from 8.5%, while the net change in employment is forecast to show that the Canadian economy has lost 27.5k jobs after gaining 62.1k in November.

After scaling back its QE purchases in October, the BoC decided to keep its policy unchanged in December, noting that the rebound in the global and Canadian economies has unfolded largely as the Bank anticipated in its October Monetary Policy Report. Officials acknowledged that the positive vaccine news is providing some reassurance but added that the pace and breadth of the global rollout of vaccinations remain uncertain. Overall, the language was on the neutral side, and a weak employment report is unlikely to spark speculation for more reductions in QE purchases. On the contrary, it may add to chances of a QE re-increase, which could hurt the Canadian dollar. That said, we believe that the overall path of this commodity currency will depend on developments surrounding the broader sentiment. As we already noted, we see risk appetite improving in 2021, at least in the first months, something that could prove supportive for oil prices and thereby for the Canadian dollar.

Elsewhere, we get Germany’s trade balance for November, and Eurozone’s unemployment rate for the same month. Germany’s surplus is expected to have slightly declined, while Eurozone’s unemployment rate is expected to have ticked up to 8.5% from 8.4%.

We also have one speaker on today’s agenda and this is Fed Vice Chairman Richard Clarida.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.57% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.