Yesterday, the main event was the BoE’s decision not to proceed with hitting the hike button as market pricing suggested, disappointing those who add bets on such an action following hawkish hints at the last gathering, as well as hawkish remarks by several officials, including Governor Bailey himself. Today, the highlight may be the US employment report for October, where decent numbers could add to the case of a hike next year, despite Chair Powell signaling patience on Wednesday.

BoE Officials Refrain from Pushing the Hike Button Despite Market Pricing

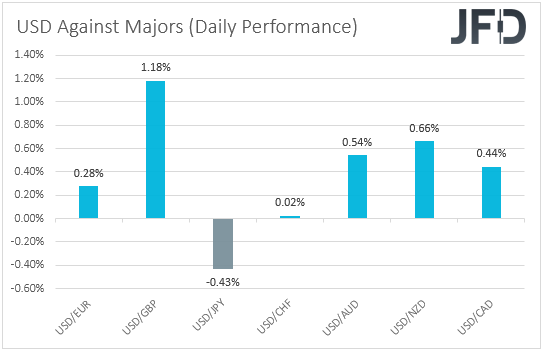

The US dollar traded higher against most of the other major currencies on Thursday and during the Asian session Friday. It gained the most versus GBP, NZD, and AUD, while it underperformed only against JPY. The greenback was found virtually unchanged against CHF.

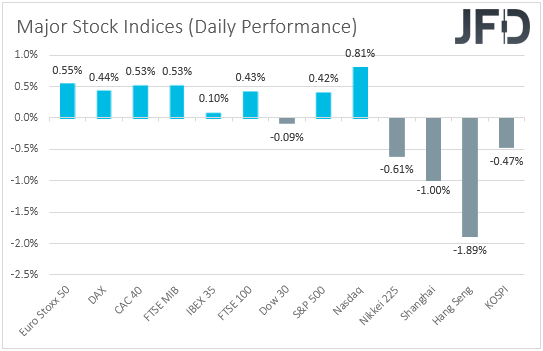

The strengthening of the US dollar and the other safe havens, yen and franc, combined with the weakening of the risk-linked Aussie and Kiwi, suggests that markets turned to risk-off trading at some point yesterday or today in Asia. The pound has also been acting as a risk-correlated currency lately, but yesterday’s weakness was the result of the BoE outcome, rather than the overall market sentiment. (See below). Turning our gaze to the equity world, we see that all-but-one of the major EU and US indices traded in the green, with the only exception being Wall Street’s Dow Jones. The S&P 500 and the Nasdaq hit fresh record highs for another day. That said, sentiment softened during the Asian trading once again, and with no apparent trigger, we stick to our guns that this is due to the uncertainty surrounding the Chinese economy and its property sector.

Now, the reason why equities may have continued drifting north this week may be the less-hawkish-than-anticipated central banks. Remember that, on Tuesday, the RBA signaled that it could start raising interest rates in 2023, sooner than its previous estimate of 2024, but the market was already more aggressive, betting that Australia’s rates will hit or surpass 1% by the end of 2022. On Wednesday, the Fed began its tapering process as expected, but maintained the “transitory” wording in the accompanying statement, while Fed Chair Powell said that they will stay patient on interest rates. Last but not least, yesterday, we had the BoE, which refrained from pushing the hike button, even as prior remarks by its officials let market participants to assign an 80% chance to such an action, at least according to the UK OIS forward yield curve. What’s more, British policymakers now noted that it will be necessary over coming months to increase the bank rate in order to return inflation sustainably to the 2% target. This means that they may not hike in December either. February is still in the “coming months” spectrum.

That’s why we saw the pound falling around 180 pips against its US counterpart. It was not only the decision to keep interest rates unchanged, but it was also the 7-2 vote in favor of doing so, and the “coming months” narrative, which suggest that policymakers may delay a potential rate lift-off beyond the end of this year. We would expect the pound to stay under selling interest for a while more, especially against the Kiwi, due to the RBNZ being the most hawkish among the major central banks, but also against the US dollar, despite Fed Chair Powell signaling patience on interest rate increases. Remember, yesterday, we said that, in our view, the Committee appeared more concerned on inflation, and also kept the door for rate hikes starting next year wide open, which could allow the US dollar to strengthen again. Clearer remarks or hints that interest rates could indeed start rising after the tapering is over may allow traders to buy more dollars.

Speaking about the Fed and the US dollar, today, the main event on the financial agenda may be the US employment report for October. Nonfarm payrolls are forecast to have rebounded to 450k after falling to 194k in September, while the unemployment rate is expected to have ticked down to 4.7% from 4.8%. Average hourly earnings are expected to have slowed somewhat on a monthly basis, to +0.4% from +0.6%, but the yoy rate is forecast to have risen to +4.9% from 4.6%.

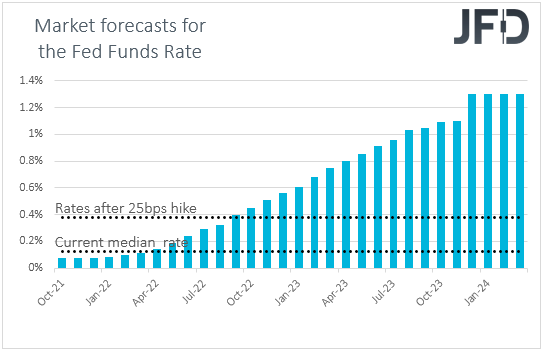

Overall, the numbers point to a decent report, and may encourage market participants to bring forth their Fed hike expectations. According to the Fed funds futures, they anticipated the first 25bps hike to be delivered in September next year. All this could encourage more USD buying, but the tricky question is: How will the stock market respond? Will it slide due to expectations of faster rate hikes, which could hurt profitability of firms, or will it rise on signs that the US economy is performing better than many may have recently feared due to the latest supply shortages. In our view, although the former has been the case in the past, we believe that lately, it’s been the latter. Thus, we expect decent jobs data to help stocks drift further north.

GBP/USD – Technical Outlook

GBP/USD fell sharply yesterday following the BoE’s decision not to hike rates. It broke below the 1.3607 and tumbled all the way to the 1.3470 zone. With the price structure being of lower highs and lower lows since October 26th, yesterday’s tumble added more negativity to this pair’s outlook.

We believe that a break below 1.4470 could extend the fall towards the 1.3412 zone, marked by the low of September 29th, the break of which could carry more bearish implications, perhaps paving the way towards the low of December 22nd, at around 1.3305. However, before we see the next leg south, there is a chance for the pair to correct part of yesterday’s overstretched slide.

Now, in order to abandon the bearish case in the short run, we would like to see a recovery above the 1.3740 zone, which provided support between October 20th and 25th. A higher high will be already confirmed and the bulls may target one of the 1.3815, 1.3835, and 1.3854 zones, defined as resistances by the highs of October 28th, October 19th, and September 15th, respectively. If neither zone is able to stop the advance, we may experience extensions towards the peak of September 14th, at around 1.3913.

EUR/USD – Technical Outlook

EUR/USD traded lower yesterday, to hit once again the key support zone of 1.1524, which has been holding the rate from falling lower since October 6th. Overall though, EUR/USD remains below the downside resistance line taken from the high of May 25th, and thus, we would consider the short-term outlook to be cautiously negative.

In order to get confident on more declines, we would like to see decisive dip below the 1.1524 territory. This would confirm a forthcoming lower low on both the 4-hour and daily charts and may initially target the psychological number of 1.1500, or the 1.1465 zone, marked by the inside swing high of July 20th, 2020. If neither zone is able to halt the slide, then a break lower could set the stage for declines towards the low of July 16th, at 1.1370.

We will start examining a bullish reversal only upon a break above 1.1694, the high of October 28th. This could signal the break above the aforementioned downside line and may pave the way towards the 1.1749 zone, marked by the peak of September 23rd, the break of which could allow extensions towards the high of September 17th, at around 1.1790.

As for the Rest of Today’s Events

At the same time with the US NFPs, we get the employment report for October from Canada as well. Expectations are for the unemployment rate to have slid to 6.8% from 6.9%, but for the net change in employment to show that the economy has added fewer jobs than in September. With the BoC unexpectedly ending its QE program last week, officials may be now scratching their heads on when the appropriate time for a rate increase may be. The financial world anticipates such a move early next year, and in our view, a slowdown in jobs growth for just a month is unlikely to change that, especially if the unemployment rate indeed slides.

We will also get to hear from four central bank officials and those are: ECB Vice President Luis de Guindos, ECB Executive Board member Fabio Panetta, BoE MPC member Dave Ramsden, and BoE MPC member Silvana Tenreyro.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.90% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.