The pound edged south on Monday, following weekend remarks that revived concerns over a disorderly Brexit, and remained pressured after the disappointing manufacturing PMI for August. Overnight, the RBA was not as dovish as some may have expected and thus, the Aussie rebounded.

Pound Tumbles on Brexit Remarks and Disappointing Data

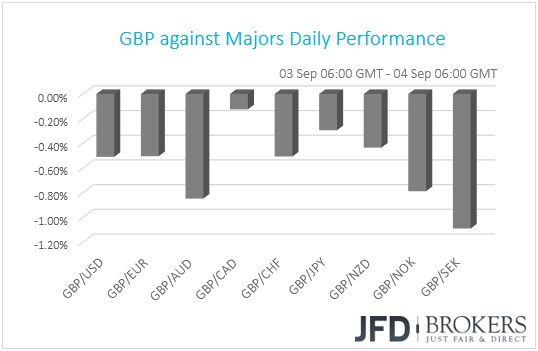

The pound traded lower against all the other G10 currencies on Monday. It lost the most against SEK, AUD and NOK, in that order, while it depreciated the least against CAD.

The British currency opened Monday with a negative gap following remarks by EU chief negotiator Michel Barnier and by UK PM Theresa May. Over the weekend, Barnier noted that he is “strongly opposed” to Theresa May’s latest proposal on the future trade relationship between the UK and the EU, while the UK Prime Minister, writing in the Telegraph, noted that she will not accept compromises to her plan that are against the national interest.

Remember that last week, the pound surged after Barnier said, “We are prepared to offer Britain a partnership such as there never has been with any other third country.” At the time, we noted that although the comments were a major relief for investors, they were far from suggesting that a deal is imminent. The weekend developments confirmed that, and they may have revived fears that the UK could end up leaving the EU without any deal.

Apart from the political landscape, the pound was also hit by disappointing economic data. Yesterday, the UK manufacturing PMI for August slid to 52.8 from a downwardly revised 53.8 in July, missing expectations of 53.9. This was the lowest point since July 2016 and may have raised questions whether the economy can maintain its recovery seen in Q2, following the slowdown in the first three months of the year. Today, we get the construction PMI, where another disappointment, combined with fears of a no-deal Brexit, could bring the pound under renewed selling interest. That said, we believe that investors may choose to place more emphasis on the services PMI due out tomorrow, as the service sector accounts for almost 80% of the UK GDP.

As for our view, we expect the pound to remain extremely sensitive to developments surrounding the UK’s departure from the EU. With the clock ticking towards the 29th of March 2019, the official date of the EU-UK divorce, and with no signs that two sides can find common ground, investors’ anxiety could increase and thereby, the pound could stay under selling interest. Even if we get remarks similar to those Barnier made last week, we would expect any pound-rallies to stay short lived. We would like to see clear evidence that the two sides have made notable progress towards securing a deal before we start examining whether the pound could hold onto any gains.

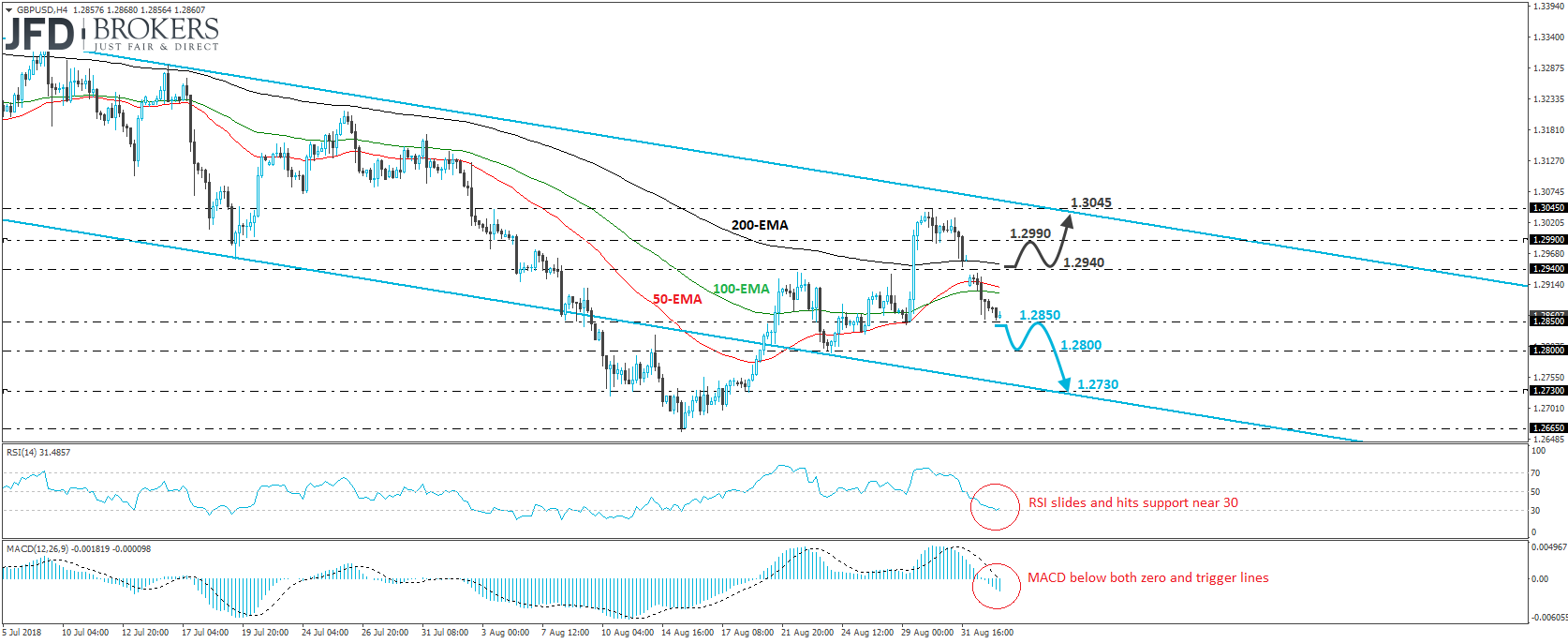

GBP/USD – Technical Outlook

GBP/USD opened with a negative gap on Monday, breaking below back below the 1.2940 hurdle. The slide continued throughout the whole day and today, during the Asian morning, the declined was paused slightly above the 1.2850 level. Bearing in mind that the latest leg down began after the rate hit resistance slightly below the upper end of the downside channel that contained most of the price action since the end of May, we would consider the near-term outlook to be negative for now.

If the bears are strong enough to regain momentum soon, then we would expect them to push the rate below the 1.2850 level and perhaps aim for our next support, at around 1.2800, defined by the low of the 24th of August. Another dip below 1.2800 could carry more bearish implications and is possible to pave the way for the crossroads of the 1.2730 level and the lower end of the aforementioned channel.

Taking a look at our short-term oscillators, we see that the RSI slid and hit support near its 30 line, while the MACD remains below both its zero and trigger lines. Both these indicators detect downside momentum and support the case for further declines, but the fact that the RSI rebounded somewhat from near 30 make us cautious that a minor bounce may be on the cards before the next negative leg.

On the upside, a clear move above 1.2940 may signal that the bears decided to take a break for a while and could initially target the 1.2990 zone. A break above that zone could open the path for another test near the 1.3045 barrier, or the channel’s upper bound.

Aussie Rebounds After the RBA

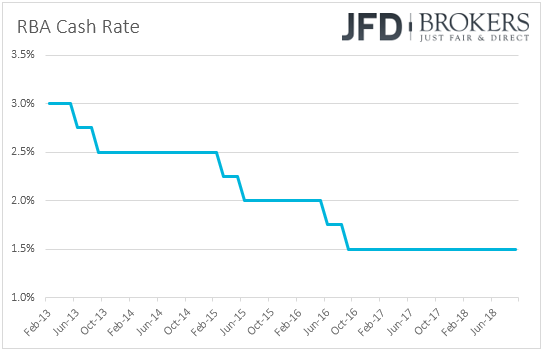

The Aussie managed to gain some ground overnight against its US counterpart, following the RBA policy meeting. Once again, officials kept interest rates unchanged +1.50% and made little changes in the accompanying statement.

The Bank reiterated that its central forecast is for growth to average a bit above 3% in 2018 and 2019 and added that in the first half of 2018, the economy is expected to have grown at an above-trend rate. Officials made no changes to their inflation outlook, while they maintained their positive view on the labor market. With regards to wage growth, they repeated that it remains low, but they removed the part saying that this is likely to continue for a while yet, and instead added that wage growth has picked up a little recently.

Although this statement is far from suggesting a change in the RBA’s future plans, the Aussie may have gained on the somewhat upbeat additions , or the lack of more concerns over the global trade and the increase in mortgage rates by some lenders. Remember that last week, Westpac decided to increase its variable mortgage rates by 14bps, which combined with the increased uncertainty over global trade, may have prompted market participants to position themselves for a somewhat more dovish outcome. Instead policymakers repeated that one ongoing uncertainty regarding the global outlook stems from the direction of trade policy in the US and that although some lenders have increased mortgage rates by small amounts, the average rate is lower than a year ago.

As for our view, we still believe that AUD/USD may be poised to drift lower, and we would treat the latest recovery as a corrective bounce. On the one hand, the RBA has a long way to go before considering pushing the hiking button, while on the other, the Fed is expected to hike two more times this year. What’s more, as we noted in the past, escalating trade tensions between China and the US are likely to keep extra pressure on the Australian currency, given that the Australian economy is heavily dependent on exports to China, while the greenback may continue attracting safe-haven flows.

AUD/USD – Technical Outlook

AUD/USD edged north following the RBA decision after it hit support slightly above the 0.7185 barrier. However, the recovery remained limited slightly below 0.7240, a resistance marked by the inside swing lows of the 23rd and 24th of August. The pair is still trading below the downtrend line taken from the peak of the 16th of February, which keeps the medium-term outlook negative.

We would expect the bears to take charge again soon and aim for another test near 0.7185. If they prove strong enough to overcome that level, then we may see them driving the battle towards 0.7160, a support defined by the lows of the 23rd and 28th of December 2016, which is fractionally below yesterday’s low.

Shifting attention to our momentum indicators, we see that the RSI rebounded from near its 30 line, while the MACD, although negative, has bottomed and crossed above its trigger line. These indicators suggest that the pair may continue to recover a bit more before the bears decide to shoot again, perhaps towards the 0.7240 level, or slightly above it.

Nevertheless, in order to assume the bears have quit the game, at least for the short run, and that a notable recovery may be looming, we would like to see a clear move above 0.7275. This could open the way for the 0.7315 level, the break of which could trigger extensions towards our next resistance of 0.7360.

As for the Rest of Today’s Events

During the European morning, we get Switzerland’s CPI for August. Expectations are for the Swiss inflation rate to have remained unchanged at +1.2%. Although this is above the SNB’s inflation projections for Q3, it is still distant of the Bank’s 2% objective. According to their latest projections, SNB policymakers, expect inflation to exceed their target in Q1 2021, conditional upon interest rates staying at current levels over the entire forecast horizon. Thus, even if inflation accelerates somewhat, we don’t expect this to alter expectations around the SNB’s thinking, especially if we take into account the latest strength of the Swiss franc.

In the US, the final Markit manufacturing PMI for August, as well as the ISM manufacturing index for the month are coming out. The final markit print is forecast to confirm its preliminary estimate, while the ISM index is anticipated to have declined to 57.6 from 58.1.

Tonight, during the Asian morning, Australia’s GDP for Q2 is due to be released. Expectations are for the quarterly rate to have declined to +0.8% from +1.0%, something that could bring the yoy rate down as well, to +2.8% from +3.1%. China’s Caixin services PMI for August is also coming out.

As for the speakers, BoE Governor Mark Carney and several other MPC members will testify on the August Inflation Report before the UK Parliament’s Treasury Committee. RBA Governor Lowe and Chicago Fed President Charles Evens are speaking as well.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.