The pound tumbled at the opening on Monday as latest Brexit developments poured cold water on expectations that a Brexit breakthrough was imminent. The common currency suffered as well, with EUR/USD breaking below 1.1300 ahead of today’s deadline for Italy to submit its revised budget to the EU Commission. In the energy market, oil slid after Trump tweeted that Saudi Arabia and OPEC should not cut oil production.

Pound Stays Driven by Brexit, Euro Slides Ahead of Italy’s Revised Budget

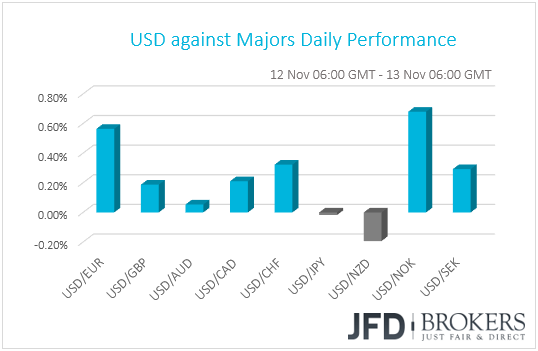

The dollar traded higher against most of the other G10 currencies on Monday. It gained the most against NOK, EUR and CHF in that order, while it underperformed against NZD. The greenback traded virtually unchanged against JPY and AUD.

Monday was marked by a risk-off investor mood, with major EU and US indices closing in negative territory. Sentiment in Europe remained fragile perhaps due to worries surrounding Brexit and Italy (see below), while US markets took a hit after the Wall Street Journal reported that the US is thinking to broaden its trade battle with China beyond tariffs. The report said that the Trump administration is planning to use export controls, indictments and other tools to counter the theft of intellectual property.

That said, market sentiment took a 180-degree turn overnight on headlines that China’s top trade negotiator is expected to visit the US as part of the preparations of the talks between the US President and his Chinese counterpart Xi Jinping at the G20 summit later this month. The safe haven yen, which has been under buying pressure throughout the day, slid overnight following the news, giving back all its daily gains. The commodity-linked currencies AUD and NZD rebounded, recovering earlier losses.

Moving to the pound, the British currency tumbled at Monday’s open following reports that PM Theresa may was forced to cancel a meeting scheduled for yesterday, due to fresh opposition both domestically and in Europe. The news came on top of Jo Johnson’s resignation as transport minister on Friday, which was followed by headlines that four more ministers are on the verge of quitting. Sterling gained later in the day after the Financial Times noted that EU’s chief Brexit negotiator Michel Barnier said that the main elements of an exit treaty are ready to present to the UK cabinet on Tuesday, but the remarks were denied by May’s spokesman and the pound returned towards its lows. The currency rebounded again somewhat overnight.

As for our view, we believe that the risks surrounding the pound’s forthcoming direction may be tilted to the downside. Even if May finds common ground with her Cabinet today, and even if what is agreed is accepted by the EU as well, any deal would still have to get approval by Parliament. In our opinion, the conditional probability for something like that is very low at the moment.

Another victim of the aforementioned Brexit-related headlines may have been the euro, the traders of which, apart from worrying about a disorderly EU-UK divorce, have to deal with another source of political uncertainty: The Italian budget. Yesterday, the common currency tumbled below the 1.1300 key hurdle against its US counterpart, hitting levels last seen on the 27th of June last year. Today is the deadline for Italy to submit its revised budget to the EU Commission. Revealing its own forecasts based on the policies the Italian government wants to put forward, the EU Commission suggested that Italy’s growth projections were overly optimistic and that its deficit could be in fact 2.9%, instead of 2.4% as the Italian government is insisting.

On Friday, Italy’s finance minister Giovanni Tria said that he has no intention of altering Italy’s 2019 spending plans, but on Sunday, sources said that the Treasury could reduce its GDP projection for next year in order to convince the Commission that the budget deficit will not exceed 2.4% of GDP. Thus, it would be interesting how Rome’s revised plan will look like and whether the EU will reject it again.

GBP/USD – Technical Outlook

GBP/USD tumbled yesterday at the opening to find support during the early European morning slightly below 1.2840. The rate rebounded later in the day but hit resistance between the 1.2920 and 1.2950 barriers and returned back near 1.2840, before recovering somewhat again overnight. The pair has been in a sliding mode since the 7th of November, and with no reversal signs on the horizon, we will stay cautiously negative with regards to the short-term outlook.

If the bears manage to take charge again soon and push the rate below the 1.2840 support zone, then we may experience extensions towards 1.2775. Another dip below that area could carry more bearish implications, perhaps targeting the 1.2700 territory, marked by the lows of the 30th and 31st of October.

That said, our short-term oscillators suggest that some further recovery may be in the works before the next negative leg, perhaps for another test near the 1.2920 line. The RSI has bottomed within its below-30 zone and just moved above 30, while the MACD, although below both its zero and trigger lines, has started to bottom.

In order to start examining the case of larger bullish extensions though, we would like to see a clear break through the 1.2950 resistance. Such a break could encourage buyers to drive the battle towards the psychological zone of 1.3000, and if they manage to overcome it, then we could see them aiming for the 1.3055 level, marked by Friday’s high.

Oil Tumbles on Trump’s Tweet

Moving to the energy market, oil prices opened with a positive gap on Monday after OPEC and major non-OPEC producers, known as the OPEC+ group, signaled willingness to reduce production in 2019, while Saudi oil Minister Khalid Al-Falih said that his nation will reduce output by 500k bpd, starting in December. On Monday, Khalid Al-Falih said that over the weekend, the group agreed that their analysis suggests the need for a 1mn bpd supply reduction from October levels.

That said, the rebound in oil prices remained short-lived, with the black liquid coming back under new selling interest after US President Trump said via its Twitter account that “Hopefully, Saudi Arabia and OPEC will not be cutting oil production”. “Oil prices should be much lower based on supply!” the US President added.

Oil prices have been in a slide mode since the beginning of October due to a blend of surging US production, a risk-off environment, as well as concerns over global growth. The fact that the US granted waivers to eight countries letting them to continue importing Iranian oil, even after it sanctioned the nation, did not help oil prices either. Now oil traders are likely to turn their attention to the OPEC and IEA monthly reports, due out today and tomorrow respectively, for clues around the supply-demand balance in the market.

As for our view, although OPEC and its allies are more likely (than not) to proceed with cutting production at their upcoming meeting, scheduled for the 6th of December, we expect oil’s direction heading into the event to be dictated by headlines surrounding the amount of the expected cut. Currently, the information investors have in hand is for 1mn bpd. Therefore, anything suggesting a deeper cut could encourage oil-bulls to jump back into the action, while news pointing to a lower number could disappoint investors and the “black gold” may slide further.

WTI – Technical Outlook

WTI opened with a positive gap yesterday, but hit resistance near 61.45 and then, it tumbled again. The price structure remains of lower peaks and lower troughs below the short-term downtrend line taken from the peak of the 10th of October, as well as below the prior long-term uptrend line drawn from the low of the 21st of June last year. Thus, we would consider the near-term outlook to still be negative for now.

The latest slide brought the price below Friday’s low of 59.45, something that may have opened the way for the 58.10 barrier, which proved a strong support zone from the 9th until the 14th of February. If the bears manage to overcome that obstacle this time around, then we may experience extensions towards the low of the 18th of December 2017, at around 56.85.

Looking at our short-term momentum studies, we see that the RSI slid near its 30 line, but now looks flat, while the MACD, although below both its zero and trigger lines, shows signs that it could start bottoming soon. What’s more, there is positive divergence between both these indicators and the price action. So, having these signs in mind, we would stay cautious of a possible corrective bounce before the next negative leg.

That said, even if WTI rebounds back above 59.45, we would still consider the outlook cautiously negative. We believe that the bulls would still have the chance to take charge from near the crossroads of the 61.45 resistance and the aforementioned short-term downtrend line. We would like to see a clear break above 63.35 before we start examining whether the bulls have abandoned the battle, at least in the near term. Something like that could initially pave the way for the 65.45 zone, the break of which could carry extensions towards 67.10, a resistance marked by the high of the 31st of October.

As for the Rest of Today’s Events

Apart from any fresh headlines around Brexit, GBP traders may keep an eye on the UK employment data for September. Expectations are for the unemployment rate to have remained unchanged at its 43-year low of 4.0%, while average weekly earnings including bonuses are forecast to have accelerated to +3.0% yoy from +2.7% in August. The excluding-bonuses wage rate is forecast to have held steady at +3.1% yoy. According to the IHS Markit/REC Report on Jobs for the month, starting salaries for permanent placements rose at the fastest pace since April 2015, while temporary payment accelerated as well. In our view, the strong increases in both permanent and temporary pay suggest that the risks surrounding the ex-bonuses earnings forecast may be tilted to the upside. However, even if accelerating wages prove somewhat positive for the pound, we expect Brexit developments to remain the currency’s main driving force.

Germany’s final CPIs for October are also due to be released, but as usual, the final prints are expected to confirm the preliminary estimates.

As for tonight, during the Asian morning Wednesday, we get preliminary GDP data for Q3 from Japan. Expectations are for the Japanese economy to have shrunk 0.3% qoq, after growing 0.7% in Q2. This, combined with the fact that all the nation’s inflation metrics stand well below the BoJ’s objective of 2%, would support our long-standing view that BoJ policymakers have a long way to go before they start considering a step towards normalization. From Australia, we get the wage price index for Q3, while from China, we have retail sales, industrial production, and fixed asset investment, all for October.

As for the speakers, we have five on the agenda: ECB Chief Economist Peter Praet, ECB Executive Board member Sabine Lautenschläger, Fed Board Governor Lael Brainard, Minneapolis Fed President Neel Kashkari, and Philadelphia Fed President Patrick Harker.

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.