This week, market participants are likely to be sitting on the edge of their seats in anticipation of the G20 summit, where US President Trump and his Chinese counterpart Xi Jinping are likely to meet and discuss trade. With regards to the other events of the week, we have an RBNZ gathering. Following the Bank’s decision to cut rates in May, we will dig into the statement for clues as to whether another cut in the months to come is looming. Eurozone’s preliminary CPIs for June, as well as the US core PCE index for May, are also due to be released.

Monday appears to be a relatively light day in terms of economic events and indicators, with the only release worth mentioning being the German Ifo survey for June. Expectations are for the current assessment index to have slid slightly, to 100.3 from 100.6, while the business expectations one is forecast to have declined to 94.6 from 95.3. The business climate index is forecast to have slid to 97.4 from 97.9. The case for lower Ifo indices is supported by declines in both the current conditions and economic sentiment ZEW indices for the month.

On Tuesday, during the Asian morning, New Zealand’s trade data for May are scheduled to be released, and expectations are for the nation’s trade surplus to have narrowed somewhat. Later in the day, the US Conference Board consumer confidence index for June and new home sales for May are coming out. The CB index is expected to have declined to 132.0 from 134.1, while new home sales are forecast to have rebounded 2.2% mom after falling 6.9% in April.

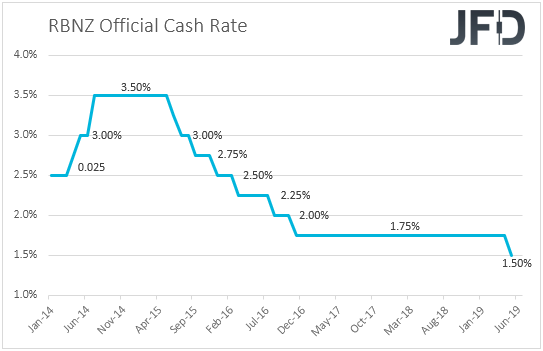

On Wednesday, during the Asian morning, the main event is likely to be the RBNZ rate decision. This would be one of the “smaller” meetings that are not accompanied by updated economic projections, neither a press conference by Governor Adrian Orr. Thus, if the Bank keeps interest rates unchanged as it is expected, attention is likely to fall on the meeting statement. When they last met, RBNZ officials decided to cut rates by 25bps, to +1.50% from +1.75%, and lowered their rate-path projections, signaling that another rate cut may be possible during the forecast horizon. Specifically, the projections showed the OCR hitting 1.4% in March 2020, staying there until June 2021, and then rebounding slowly towards 1.9% by June 2022.

Last week, data showed that the economy grew 0.6% qoq in Q1, more than the RBNZ’s +0.4% qoq projection for the quarter, which added credence to early June remarks by RBNZ Assistant Governor Christian Hawkesby that interest rates will “remain broadly around current levels for the foreseeable future”. Having said that though, the data were referring to a period before the latest escalation in tensions between the US and China. Thus, we will dig into the statement to see whether Hawkesby’s view is shared among other policymakers as well, or whether another rate decrease at one of the upcoming meetings is looming.

In the US, durable goods orders for May are due to be released. Headline orders are expected to have stagnated after falling 2.1% mom in April, while the core rate is expected to have ticked up to +0.1% mom from 0.0%.

On Thursday, Asian time, we have Japan’s retail sales for May and the forecast is for an acceleration to +1.2% yoy from +0.5% in April. New Zealand’s ANZ Business Confidence index for June is also coming out, but no forecast is currently available.

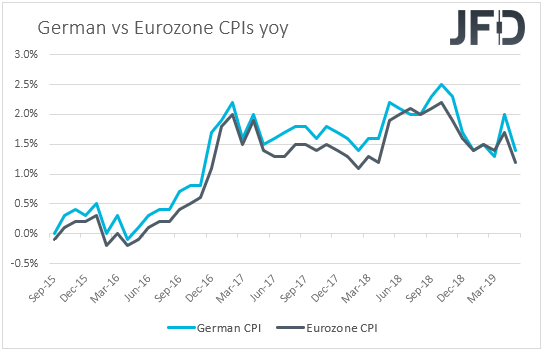

During the European morning, we get Germany’s preliminary inflation data for June. Both the CPI and HICP rates are expected to have ticked up to +1.5% yoy and +1.4% yoy, from +1.4% and 1.3% respectively. This would raise speculation that Eurozone’s headline CPI rate, due out on Friday, may rise somewhat as well.

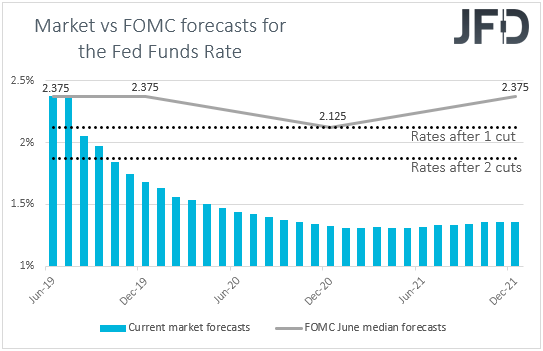

In the US, the final GDP for Q1 is due to be released. The qoq SAAR rate is forecast to have been revised up to +3.2% from +3.1%, but we expect this to pass unnoticed as it will be referring to a period ahead of the latest escalation in trade tensions between the US and China. The Atlanta Fed GDPNow model suggests that the economy slowed to +2.0% qoq SAAR in the second quarter, while the New York Nowcast points to an even more severe slowdown, to +1.4%. At last week’s meeting, the FOMC dropped its “patient” stance, and instead noted that it will “act as appropriate” to sustain the economic expansion. With 7 of its 17 members also favoring two quarter-point rate cuts by year end, market participants have ramped up their expectations with regards to lower US rates, with a 25bps cut fully priced in for the next gathering. US pending home sales for May are also due to be released and the forecast is for a 0.9% mom rebound after a 1.5% slide.

On Friday, during the Asian morning, we get the usual end-of-month data dump from Japan. No forecast is available for the headline Tokyo CPI rate, while the core one is anticipated to have ticked down to +1.0% yoy from +1.1%. The unemployment rate is expected to have held steady at 2.4%, while the preliminary industrial production data for May are forecast to show a slight acceleration to +0.7% mom from +0.6%. The Summary of Opinions from last week’s BoJ gathering is also due to be released. At that meeting, the Bank kept its ultra-loose policy and forward guidance unchanged. That said, following the decision, Governor Kuroda said that extra stimulus would be considered if momentum towards reaching their inflation aim is lost. Thus, we will scan the report for clues on how strong such a case is, and when further easing may be introduced.

During the European day, the preliminary CPIs for June are due to be released. The headline rate is expected to have remained unchanged at +1.2% yoy, while the core one is anticipated to have risen to +1.0% yoy from +0.8%. Bearing in mind that both the German CPI and HICP metrics, due out the day before, are expected to have accelerated somewhat, we see the case for Eurozone’s headline rate to have risen as well. However, even if this is the case and the headline rate moves slightly higher, it would still be well below the ECB’s objective of “below, but close to, 2%”. Thus, we doubt that this could prompt investors to reduce their cut bets. Following ECB President Draghi’s remarks last week over additional stimulus, market participants have brought forth their cut expectations, with a 10bps decrease in the deposit rate almost fully priced in for September.

In the UK, we have the final GDP for Q1, which is expected to confirm its preliminary estimate, namely, that the UK economy accelerated to +0.5% qoq in the three months of 2019, from +0.2% in Q4. However, we already had data pointing to how the economy has performed during Q2, and the picture was not so bright. Latest monthly data showed that GDP shrank 0.4% mom in April, with the NIESR projecting a 0.2% contraction for the whole quarter. Even the BoE revised lower its projection for Q2, to 0.0% from 0.2% previously.

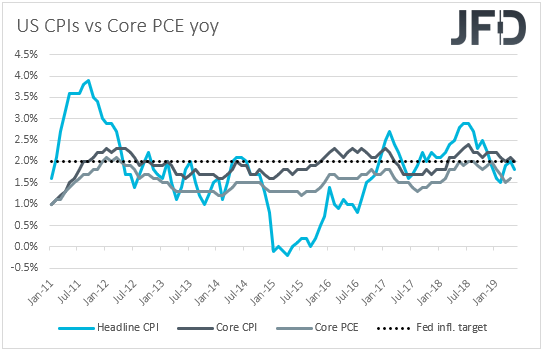

Later in the day, we get the US personal income and spending data for May, as well as the core PCE index for the month. The income rate is expected to have declined to +0.3% mom from +0.5%, but bearing in mind that the average hourly earnings monthly rate for May held steady, we see the risks surrounding the income forecast as tilted somewhat to the upside. Spending is expected to have picked up some steam, accelerating to +0.5% mom from +0.3%, something supported by the retail sales for the month, which also accelerated.

As far as the core PCE index is concerned, which is the Fed’s favorite inflation metric, it is expected to have held steady at +1.6% yoy. However, bearing in mind that the core CPI rate for the month ticked down, we see the risks as tilted slightly to the downside. In any case, even if the PCE rate rises somewhat, we doubt that this could prompt investors to price out a July rate cut by the FOMC. As we already noted, the Fed has opened the door to rate decreases last week, with 7 members supporting 2 quarter-point decreases by December, which is largely in line with market expectations. Apart from July, investors anticipate another cut in September.

From Canada, we get the monthly GDP for April, which is expected to have slowed to +0.2% mom from +0.5% in March. Coming on top of the slowdown in retail sales for the month, this would not be pleasant news for BoC policymakers. However, taking into account the strong acceleration in the CPIs for May and the better-than-expected employment report for the month, we doubt that officials will be tempted to turn their eyes to the cut button when they meet next, on July 10th. They may repeat that the degree of accommodations provided by the current rate remains appropriate and that they will remain data dependent in taking future decision.

Apart from the economic releases, the two-day G20 summit in Japan begins. The spotlight, at least marketwise, will fall on the potential meeting between US President Trump and his Chinese counterpart Xi Jinping, where the two leaders are expected to discuss trade. Up until last week, it was not sure whether such a meeting would take place, with China declining to comment on that front and Trump threatening with more tariffs if the Chinese President did not attend the summit. However, last Tuesday, Trump said he had a very good telephone conversation with Xi, and that they will hold an extended meeting at the summit.

As we noted last week, we don’t expect the two leaders to sign any final accord, but “progress” remarks, pointing towards that direction, may be enough to encourage investors to add to their risk exposure. On the other hand, anything suggesting that there is not much willingness for working towards finding common ground, may result in the opposite market reaction, namely, risk assets could pull back, while safe havens could gain.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

70% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd