This week, market participants will be sitting on the edge of their seats in anticipation of Friday’s G20 summit, where US President Trump is scheduled to meet his Chinese counterpart Xi Jinping in order to discuss trade. The Fed is expected to be in the limelight as well. Following recent dovish remarks by several Fed members, Powell’s speech on Wednesday and the Fed minutes on Thursday may shed some light with regards to the Committee’s future plans.

Monday appears to be a relatively light day in terms of economic releases. The only one worth mentioning is the German Ifo survey for November. Both the current assessment and expectations indices are forecast to have declined somewhat, to 105.3 and 99.2 from 105.9 and 99.8 respectively, something that is likely to bring the business climate index down to 102.3 from 102.8. The case for sliding Ifo indices is supported by the ZEW survey for the month, where both the current conditions and economic sentiment indices declined as well.

That said, investors may prefer to focus on Draghi’s testimony before the European Parliament’s Economic and Monetary Affairs Committee. In recent remarks, the ECB chief acknowledged the loss in Eurozone’s growth momentum, but he repeated once again that the overall risks to the growth outlook remain broadly balanced. He also said that he anticipates QE will end in December. Therefore, it would be interesting to see whether he continues to hold that view, even after another disappointment in the bloc’s PMIs on Friday, where the composite index slid for the fourth consecutive month.

Tuesday is also a light day. During the Asian morning, we get New Zealand’s trade balance and BoJ’s core CPI, both for October. However, neither release is accompanied with a forecast.

Later in the day, we have the US Conference Board consumer confidence index for November, which is expected to have declined to 135.5 from 137.9 the month before.

On Wednesday, the 2nd estimate of the US GDP for Q3 is due to be released. The forecast suggests that the 2nd estimate is likely to confirm the 1st one and reveal that the US economy grew 3.5% qoq SAAR in the three months to September. New home sales for October are also coming out and are expected to have rebounded 4.5% mom after sliding 5.5% the previous month.

Besides the US economic data, we also have a speech by Fed Chairman Jerome Powell, just a day ahead of the minutes from the latest FOMC gathering. Recent comments by several FOMC policymakers leaned to the dovish side. The Fed’s new Vice Chairman Richard Clarida said that interest rates are very close to neutral, adding that there is some evidence of slowing global economic growth and that the Committee is at a point where it needs to be data dependent. His remarks over global economic growth were echoed by Dallas Fed President Robert Kaplan as well as Philadelphia Fed President Patrick Harker, who even appeared concerned on whether a December hike would be appropriate. Thus, following these remarks, investors would be eager to find out what’s the Fed Chief’s view on monetary policy.

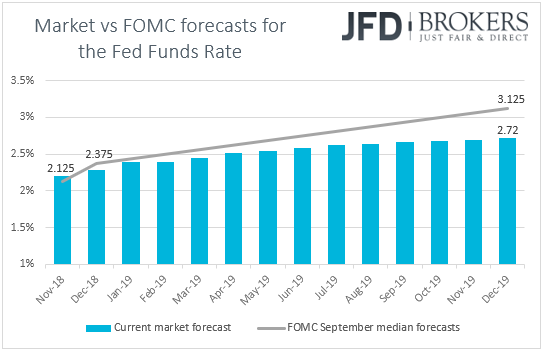

On Thursday, the spotlight is likely to fall on the Fed minutes. At that gathering, Fed officials decided to keep interest rates unchanged as was broadly expected, and made almost no changes in the accompanying statement, something that was interpreted as keeping the door wide open for a December hike and more to come in 2019.

However, following the aforementioned dovish remarks, it would be interesting to see whether the massage taken by the market was the correct one. We will scan the minutes to see if any members were skeptical with regards to a December hike, and whether officials are considering a pause as soon as interest rates reach their neutral level. According to the Fed Funds futures, the market remains optimistic over a December rate increase, assigning a 76% chance for such a move, but with regards to regards to 2019, it now prices in only 1.4 hikes compared to 2 prior the dovish speeches.

As for Thursday’s economic indicators, during the European morning, Germany’s preliminary CPI for November is due to be released. Expectations are for the German inflation rate to have declined to +2.3% yoy from 2.5% in October, which could raise speculation that Eurozone’s headline inflation, due out on Friday, may slow as well. The nation’s unemployment rate for November is coming out as well and is forecast to have held steady at 5.1%. Switzerland’s and Sweden’s GDP prints for Q3 are also scheduled to be released and expectations are for slowing growth in both nations.

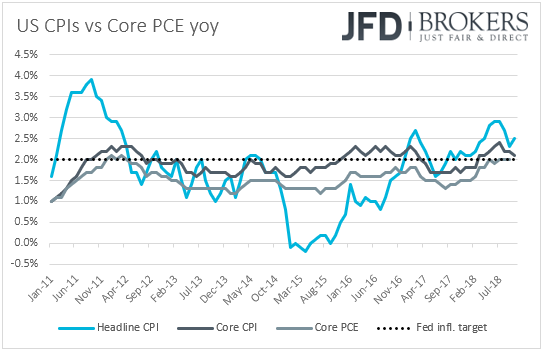

In the US, apart from the FOMC minutes, we get personal income and spending data for October, as well as the yearly core PCE rate for the month. Income is expected to have accelerated to +0.4% mom from +0.2%, and spending is expected to have risen at the same pace as in September, which is also +0.4% mom. That said, bearing in mind that the monthly earnings rate for October ticked down to +0.2% from +0.3%, we view the risks surrounding the income forecast as tilted to the downside. As for the spending forecast, given the strong rebound in retail sales for the month, we view the risks as skewed to the upside.

Moving to the yoy core PCE rate, the Fed’s favorite inflation metric, it is expected to have stayed at +2.0%, but bearing in mind the tick down in October’s core CPI rate, we believe that the risks are tilted somewhat to the downside. Although a small slowdown could raise some more concerns over the Fed’s future plans, we expect market participants to have most of their attention locked to the FOMC minutes later in the day. The US pending home sales for October are also due out and expectations are for a 0.5% mom rise, the same pace as in September.

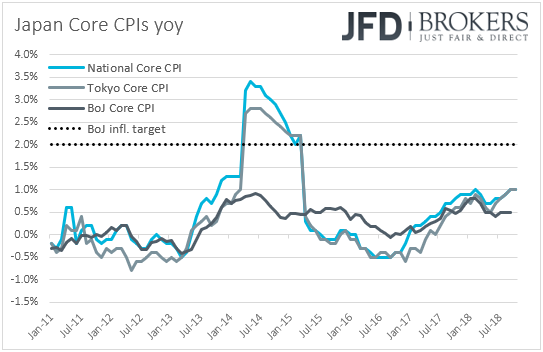

Finally, on Friday, during the Asian morning, we get the usual end of month data dump from Japan. Getting the ball rolling with the Tokyo CPIs for November, expectations are for the headline rate to have declined to +1.1% yoy from +1.5% in October, while the core rate is forecast to have remained unchanged at +1.0% yoy. This could raise bets that the National CPIs for the month may move in a similar fashion, something that would confirm our longstanding view that BoJ policymakers have a long way to go before they consider a meaningful step towards normalizing monetary policy. Moving to the nation’s preliminary industrial production data, the forecast suggests that industrial production rebounded 1.3% mom in October after sliding 0.4% in September. Japan’s unemployment rate for October is also due to be released with expectations suggesting that it held steady at 2.3%.

From China, we have the official manufacturing and non-manufacturing PMIs for November. Both indices are expected to have ticked down to 50.1 and 53.8 from 50.2 and 53.9 respectively.

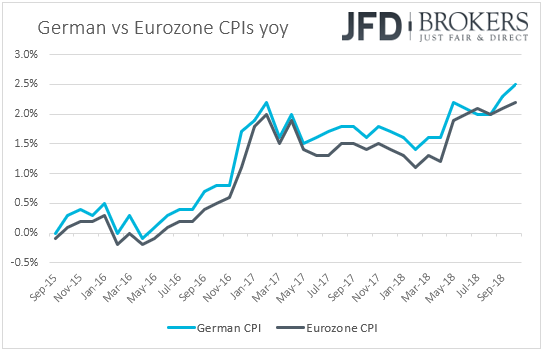

During the European morning, Eurozone’s preliminary CPIs for November are coming out. The headline rate is expected to have ticked down to +2.1% yoy from 2.2% yoy in October, something also supported by Germany’s forecast, while the core rate is anticipated to have remained unchanged at +1.1% yoy. Although a tick down would leave the headline rate above the ECB’s objective of “below, but close to 2%”, coming on top of the softness in recent economic data, like GDP and PMIs, an underlying inflation rate of +1.1% yoy could slightly increase concerns over the bloc’s economic and inflation outlooks. Eurozone’s unemployment rate and Germany’s retail sales, both for October, are due out as well.

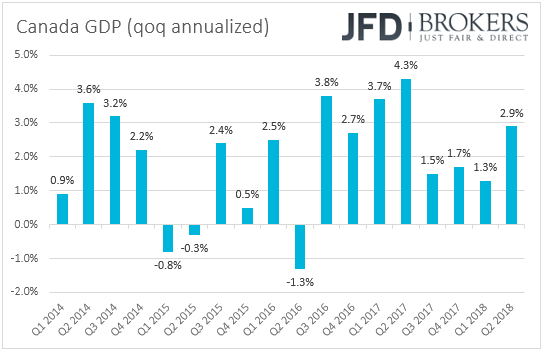

Later in the day, we get Canada’s GDP data for both September and Q3. With regards to the monthly rate for September, expectations are for the economy to have grown +0.1% mom, the same pace as in August, but the qoq annualized rate is expected to have declined to +1.9% from 2.9% inQ2. At its latest gathering, the BoC raised interest rates by 25bps and removed the part saying that officials will “take a gradual approach” with regards to future rate increases, which, in our view, means that interest rates can rise faster than previously anticipated if data suggest so.

Canada’s latest economic data have been mainly on the positive side, with both the headline and core inflation metrics accelerating in October, and the unemployment rate for the same month declining to 5.8% from 5.9%. Therefore, we doubt that a decline in the qoq annualized growth rate would be enough to alter expectations with regards to more BoC rate increases in 2019.

Apart from the data, investors are also likely to have their gaze fixed on the G20 summit in Buenos Aires, Argentina. The spotlight is likely to fall at the meeting between US President Donald Trump and his Chinese counterpart Xi Jinping. Market participants will be eager to see whether the two leaders are willing to work in finding common ground over trade, or the dispute between the two nations will escalate further.

The US President has repeatedly expressed his willingness to work towards securing a deal with China, but recent developments suggest that it would be very hard for an accord to be agreed as early as at this meeting. Last week, the Asia-Pacific Economic Cooperation (APEC) group failed to strike a communique for the first time in its history, due to differences between US and China over trade, while last Tuesday, the Trump administration said that China took “further unreasonable actions in recent months” with regards to intellectual property. In our view, the two leaders could just agree to keep the door open for further talks and perhaps signal a pause with regards to future tariffs, something that could be a somewhat positive outcome for the markets.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.