We don’t have any central bank decisions on this week’s agenda, but we do get the minutes from the latest RBA and FOMC gatherings, with investors eager to get more clues with regards to each bank’s future plans. As for the data, the most important ones may be the UK and Canadian CPIs for January, as well as Australia’s employment report for the same month.

On Monday, the calendar appears very light in terms of data, as there are not top-tier releases scheduled. However, we will get to hear once again from ECB President Christine Lagarde, remarks of whom could well affect expectations around ECB monetary policy. Remember that at the press conference following the latest ECB decision, Lagarde said that inflation remained elevated for longer than previously thought, and that the economy was hurt less than anticipated by the pandemic. She also added that the March and June meetings would be essential for evaluating their guidance, which means that they could, after all, decide to lift rates this year.

Last week though, she pushed against expectations over a summer rate increase, by saying that there were no signs that measurable monetary policy tightening would be required, while ECB member Klaas Knot said that a hike could be delivered during the fourth quarter. Therefore, clearer hints that they are unlikely to touch the hike button during the summer months could result in further pullback in the euro.

Although we don’t have any other major events on the agenda, we will stay extra careful as tensions in Ukraine have intensified, with the White House warning on Friday that a Russian attack could begin any day. A Russian invasion could result in further risk aversion, which means further retreat in equities and stronger safe havens.

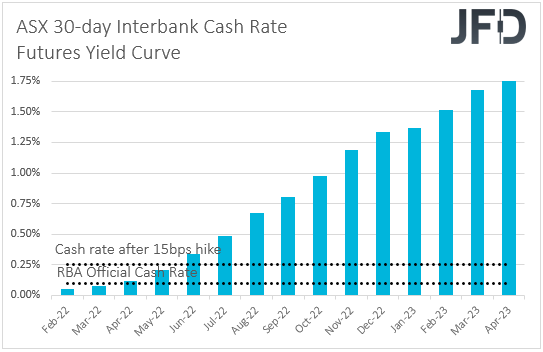

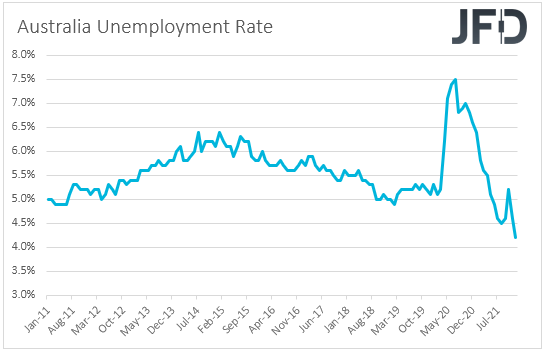

On Tuesday, Asian time, we get the minutes from the latest RBA gathering. At that meeting, officials decided to keep interest rates untouched at 0.10% and announced the end of their QE purchases, as was broadly expected. However, in the statement accompanying the decision, it was noted that, while inflation has picked up, it is too early to conclude that it is sustainably within that target band, and that they will not increase the cash rate until that happens. However, market participants remained convinced that the Bank will hike to 0.25% around May or June, while they see the OCR surpassing 1.25% by the end of the year. Thus, in order to scale back those bets, they may need clearer hints that the RBA is unlikely to touch the hike button soon. If they find such clues in the minutes, the Aussie could slide, but everything could change again on Thursday, when we get Australia’s employment report.

From Japan, we get the preliminary GDP for Q4, with the forecast pointing to a +1.4% qoq rebound after a 0.9% contraction in Q3. This will be pleasant news for BoJ policymakers, but with inflation expected to stay well below 2%, we don’t expect them to be tempted to alter their ultra-loose monetary policy. Japan’s National CPIs are due to be released on Friday.

During the early European session, the UK releases its jobs data for December. The unemployment rate is expected to have held steady at 4.1%, while there is no forecast for the employment change. Average weekly earnings, both including and excluding bonuses, are forecast to have slowed somewhat, which could be a sign that inflation may slowing soon, but we prefer to focus more on the actual inflation data for the month of January, which are released on Wednesday.

From Germany, we have the ZEW survey for February. The current conditions index is expected to have risen to -7.0 from -10.2, while the economic sentiment one is forecast to have inched up to 53.5 from 51.7. As for the Eurozone as a whole, we get the second estimate of GDP and the employment change for Q4. The second GDP estimate is expected to confirm its preliminary print, while no forecast is available for the employment change.

On Wednesday, during the Asian session, China releases its CPI and PPI rates for January, with the former expected to have declined to +1.0% yoy form +1.5%, and the latter to have slid to +9.4% yoy from 10.3%.

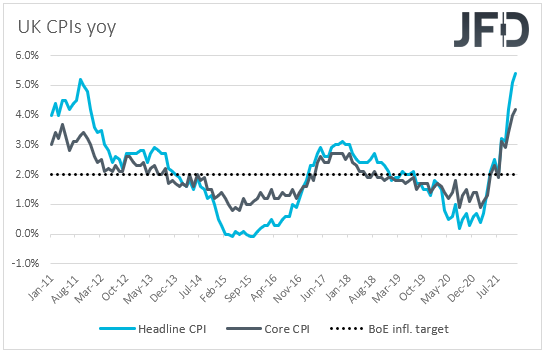

We get more CPIs for January later, during the early European session, this time from the UK. The headline rate is forecast to have held steady at +5.4%, while the core one is anticipated to have inched up to +4.3% from +4.2%. At the prior meeting, the BoE decided to lift interest rates by 25bps, to 0.50%, via a 5-4 vote, with the 4 dissenters calling for a 50bps hike. Given that only one member needs to be convinced that a double hike may be appropriate at the next gathering, these CPI numbers may attract special attention. If indeed inflation stays elevated, or even accelerates further, market participants could add to bets over a double hike at the Bank’s upcoming gathering, something that could support the British pound.

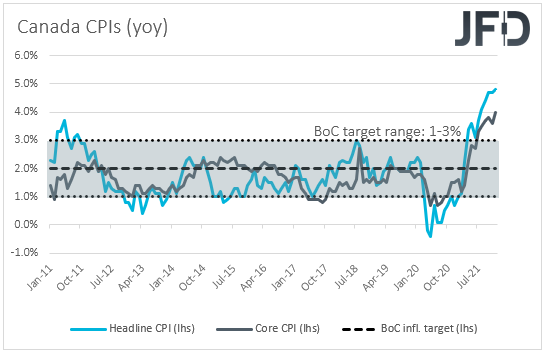

Canada’s CPIs for January are also on Wednesday’s agenda. The headline CPI is expected to stay at +4.8% yoy, while the core one to have slid to +3.5% yoy from 4.0%. At its latest gathering, the BoC decided to keep interest rates untouched at 0.25%, at a time when the financial community was expecting a hike. In the statement accompanying the decision, it was noted that the Council expects rates to increase, and that the overall economic slack is now absorbed, which means that they are more likely to hit the hike button in March. However, they once again noted that the Omicron coronavirus variant is weighing on activity, with Governor Macklem adding that hikes will not be automatic. They will take decisions at each meeting, he added. With all that in mind, we don’t expect slowing core inflation to stop officials form pushing the hike button in March, but it could prompt market participants to scale back their bets with regards to upcoming liftoffs. Something like that could weigh on the Canadian dollar.

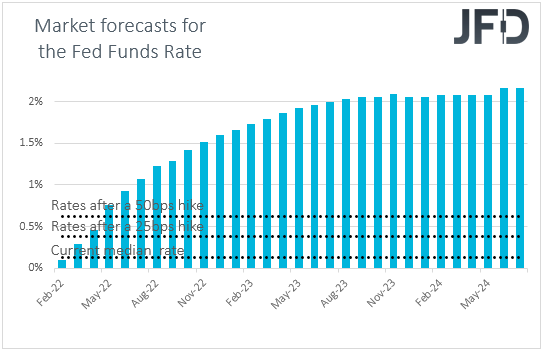

From the US, we have the US retail sales for January and minutes from the latest FOMC gathering. Both headline and core retail sales are forecast to have rebounded in January, which could add credence to market expectations with regards to the Fed’s future course of action, but we don’t believe that we will get a major market reaction as participants may stay cautious in anticipation of the Fed minutes. The message we got from the latest meeting was that a hike is coming in March, and that there is a decent likelihood for more liftoffs this year than the December “dot plot” suggested. Now, following a strong employment report and accelerating inflation in the aftermath of the gathering, market participants are fully pricing in around six quarter-point hikes by the end of the year. Thus, we will scan the minutes for clues as to whether this number is logical or not. Anything confirming that the Fed is willing to proceed as aggressing as the current market pricing suggests could support the US dollar, and perhaps result in further retreat in equities. The opposite could be possible if the minutes reveal a more cautious picture than Fed Chair Powell presented at the press conference following the decision.

On Thursday, the only release worth mentioning may be Australia’s employment report for January. The unemployment rate is expected to have held steady at 4.2%, while the net change in employment is forecast to show that the economy has lost 15k jobs after adding 64.8k in December. Conditional upon the RBA minutes revealing a cautious picture on Tuesday, a soft employment report could eventually convince investors to scale back their hike bets, something that could result in a slide in the Australian dollar.

Finally, on Friday, during the Asian session, as we already noted, we get Japan’s CPIs for January. No forecast is available for the headline rate, while the core one is anticipated to have slid to +0.3% yoy from +0.5%.

Later in the day, we have retail sales data from the UK and Canada, for the months of January and December respectively. In the UK, headline sales are forecast to have rebounded 0.6% mom after sliding 3.7%, while core sales are forecast to have slid 0.5% mom, after falling 3.6%. In Canada, both the headline and core rates are forecast to have declined to -2.1% mom and -2.3% mom, from +0.7% and +1.1% respectively.

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.82% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2022 JFD Group Ltd.