The US dollar and the Japanese yen continued to slide yesterday, while the Canadian dollar was the main gainer among the G10s as market participants remained confident that the US, Mexico and Canada could strike a trilateral deal by the end of the week. The British currency came under selling interest following PM May’s comments on Brexit.

USD and JPY Down, CAD Up as NAFTA Stays in the Spotlight

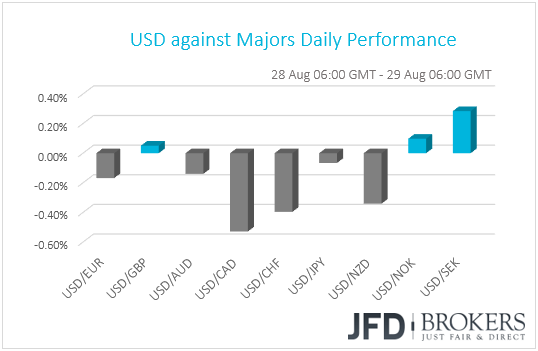

The dollar continued sliding against most of the other G10 currencies on Tuesday. It gained only against SEK, while it traded virtually unchanged versus NOK, GBP and JPY. The main gainer against the US currency was CAD.

The weakening of the dollar and the yen, combined with a strong Loonie, suggest that market participants continued to cheer the US-Mexico trade deal as well as the prospect of Canada joining in. That said, European and US indices ended their sessions flat, with market chatter suggesting that investors have started to worry ahead of the deadline for public comment over tariffs on USD 200bn of Chinese imports, which is set for the 5th of September. However, given that the news is once again old news, our own view is that investors may have decided to take a breather following the surge on Monday. End-of-month rebalancing of portfolios could also be the case.

Now back to NAFTA talks, Canada’s Foreign Minister Chrystia Freeland, who yesterday traveled to the US for the negotiations, said it is good that Mexico has made significant concessions and that those concessions would set the stage for productive talks this week as all three nations try to find a common ground by Friday. What’s more, a report overnight noted that Canada is ready to make concessions on its protected dairy market in order to secure a deal, adding more fuel to expectations that we may get a trilateral accord by the end of the week.

With the economic agenda looking relatively light today as well, we expect market focus to remain on developments around NAFTA talks. Further encouraging headlines suggesting that we may indeed have a trilateral deal by Friday could revive risk appetite, with risk assets coming under additional buying interest and safe havens, like the yen, falling further. The Loonie could keep gaining.

Now, in case Canada refuses to join, US President Trump plans to notify Congress that he will proceed only with Mexico. However, a bilateral deal with Mexico may find it hard passing through Congress, as it may not be eligible for fast-track Senate ratification and thus, it could need 60 votes (instead of 51), which means that some support from Democrats will be needed. So, having all these in mind, the scenario where Canada eventually does not agree could be a “risk off” trigger. Investors are likely to abandon riskier assets and seek shelter in safe havens, while the Canadian dollar could come under selling interest.

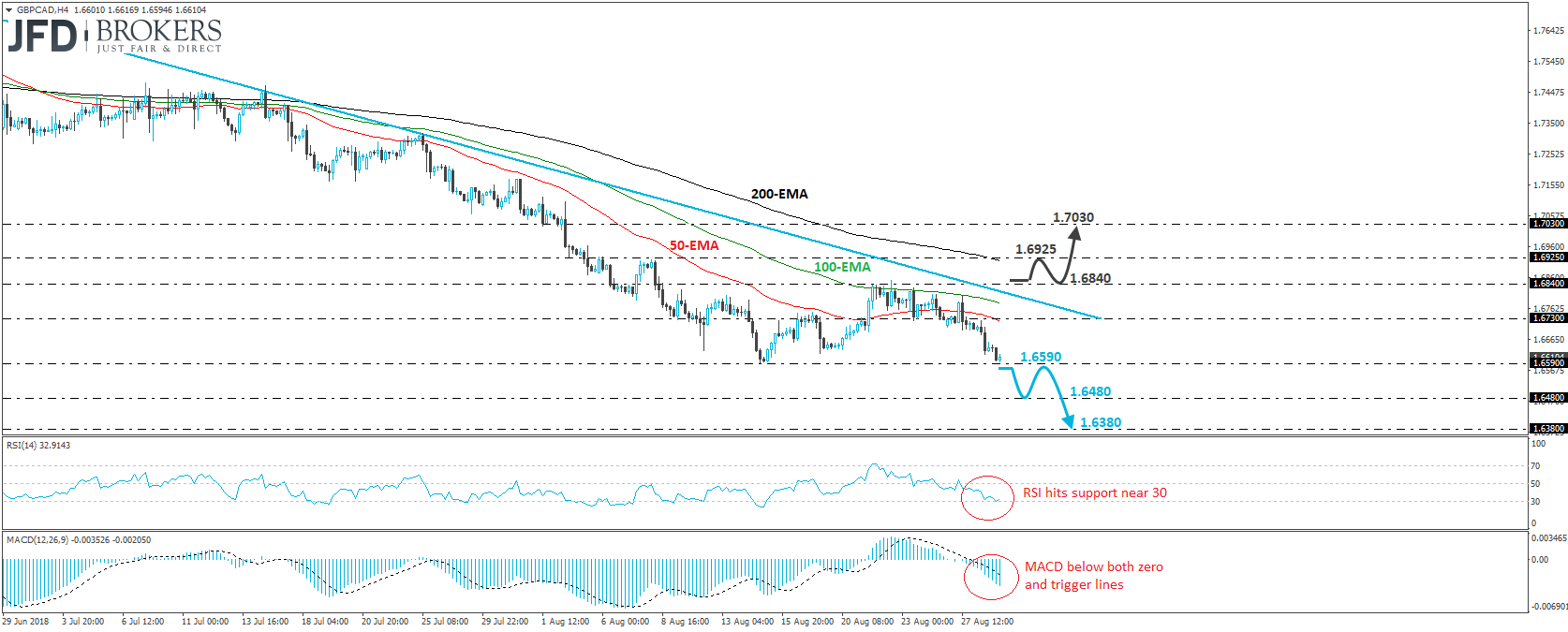

GBP/CAD – Technical Outlook

GBP/CAD traded south yesterday and during the Asian morning Wednesday, it hit support near the 1.6590 barrier, marked by the lows of the 14th and 15th of August. The rate continues to trade below the downtrend line taken from the peak of the 22nd of June and therefore, we would consider the short-term picture to still be negative.

A clear and decisive dip below 1.6590 is likely to set the stage for our next support barrier of 1.6480, defined by the inside swing peak of the 19th of October 2017. If that level is broken as well, then we may experience more downside extensions, perhaps towards the lows of the 19th and 20th of October, at around 1.6380.

Taking a look at our short-term oscillators, we see that the RSI drifted lower and hit support near its 30 line, while the MACD lies below both its zero and trigger lines, pointing down. These indicators support the case for the pair to continue lower in the short run. However, the RSI rebounded somewhat from near its 30 line, which make us cautious that a minor bounce may occur before the bears decide to seize control again.

On the upside, we would like to see a clear break above 1.6840, before we start examining the case of a short-term trend reversal. Such a move would confirm the break above the aforementioned short-term downtrend line and could initially aim for the 1.6925 resistance. Another break above 1.6925 could see scope for more upside extensions, perhaps towards 1.7030.

Sterling Slides on PM May’s Comments

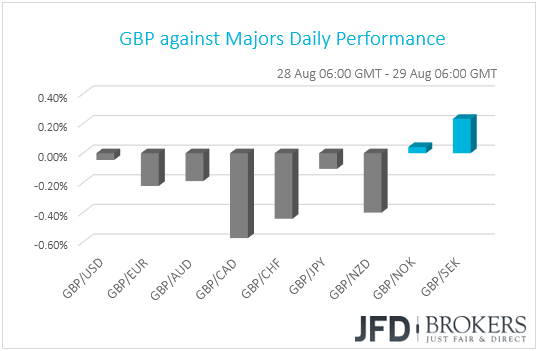

The British currency was also lower against most of its G10 peers yesterday. It gained only against SEK, while it lost the most against CAD, CHF and NZD in that order.

The catalyst behind the pound’s slide was once again developments surrounding the Brexit front. Speaking to reporters on the plane as she was traveling to Africa in an attempt to strengthen trade ties, PM Theresa May said that a no-deal Brexit “wouldn’t be the end of the world”. Although she tried to play down the consequences of the UK leaving the EU without a deal, pound traders may have interpreted her words as keeping the chances of that scenario high. What’s more, an overnight report said that officials on both sides admit that finding common ground by October is unlikely, and they will now aim to finalize the terms of the divorce by November.

As for our view it remains the same. With any BoE rate-hike expectations well-pushed into next year, the main game in town for GBP-traders remains Brexit. With the clock ticking towards the 29th of March, the official date of the UK’s departure from the EU, and no signs that the two sides are close to finding an accord, the pound could still come under additional selling interest. We would expect any rallies to stay short-lived. Even the latest recovery in GBP/USD is mainly due to dollar weakness rather than pound strength.

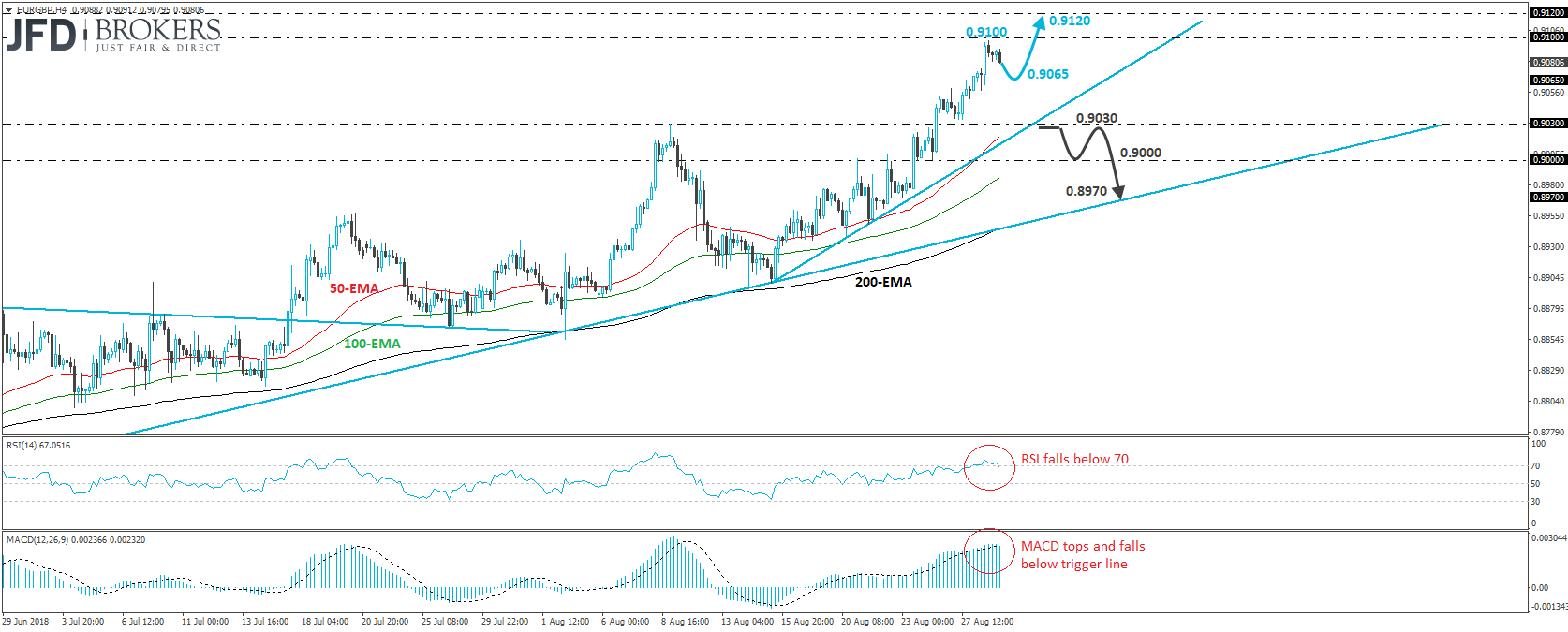

EUR/GBP – Technical Outlook

EUR/GBP continued climbing higher yesterday, breaking above the resistance (now turned into support) barrier of 0.9065. That said, the advance was stopped fractionally below 0.9100, and then the rate retreated somewhat. The price structure continues to be of higher highs and higher lows above the uptrend line taken from the low of the 21st of June, while now the pair looks to be respecting a shorter-term upside line, taken from the low of the 15th of August. So, having all these technical signs in mind, we would maintain the view that the near-term outlook is to the upside.

We would expect a clear move above 0.9100 to aim for our next resistance of 0.9120, defined by the peak of the 11th of September, but before that, we see the case for the current setback to continue for a while more before the bulls decide to jump back into the action, perhaps to test the 0.9065 zone as a support this time.

Our view for some further retreat is derived by our short-term oscillators. The RSI has topped within its above-70 zone and just crossed below 70, while the MACD, although positive, has topped and fallen below its trigger line.

Now in case the 0.9065 level does not act as a support, we would still see a decent chance for a rebound from near the upside line taken from the low of the 15th of August. We would like to see a clear dip below that line and the 0.9030 support before we start examining the case for a deeper correction. Such a break could initially aim for the 0.9000 zone, the break of which could carry more bearish implications, perhaps towards the crossroads of the 0.8970 level and the uptrend line drawn from the low of the 21st of June.

As for Today’s Events

The second estimate of the US GDP for Q2 is due to be released. Expectations are for a downside revision to 4.0% qoq SAAR from 4.1% qoq SAAR, but this would still mark the strongest rate in nearly four years. US pending home sales for July are also coming out and expectations are for a slowdown to +0.4% mom from +0.9% in June.

From Canada, we get current account data for Q2. Expectations are for the nation’s current account deficit to have narrowed to CAD -15.3bn from CAD -19.5bn.

As for the energy market, the Energy Information Administration’s (EIA) weekly crude oil inventories are set to be released. The forecast suggests that inventories fell by around 0.7mn barrels in the week ended on the 24th of August, after a 5.8mn barrels slide the week before.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.