Following the ECB’s decision to cut its deposit rate and to restart its QE program, we have five more central banks on this week’s agenda: The Fed, the BoJ, the SNB, the Norges Bank and the BoE. The Fed is anticipated to cut rates by 25bps, and thus, if this is the case, all the attention may be on how officials intend to move forward. Following recent reports that the BoJ is more open to discuss further stimulus, it would be interesting to see whether it will decide to act as early as this week. We are also eager to find out whether the SNB will follow the footsteps of the ECB. The Norges Bank is the only Bank expected to hike, while the BoE is anticipated to stand pat.

Monday is the only light day this week, with the only indicator worth mentioning being the New York Empire State manufacturing index for September, which is expected to have declined to 4.00 from 4.80.

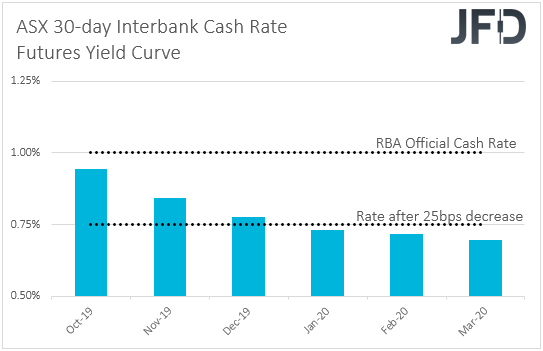

On Tuesday, during the Asian morning, we get the minutes from the latest RBA policy decision. At that meeting, the Bank decided to keep interest rates unchanged at the record low of +1.00%, and reiterated that they will continue to monitor developments, including in the labour market, and ease monetary policy further “if needed”.

In our view, keeping the “if needed” part within the statement lessened the chance for an October move, and made November and December more likely candidates. It seems that the market holds the same view as well. According to the ASX 30-day interbank cash rate futures implied yield curve, the probability for an October cut lies at 22%, while the chance for something like that to happen in November stands at 64%. A 25bps cut is almost fully priced in for December. Thus, we will scan the minutes for clues as to whether policymakers are indeed planning to hold off from acting when they meet next, or whether they are in a rush to push the cut button again.

As for Tuesday’s data, Germany’s ZEW survey for September is coming out, as well as the US industrial and manufacturing production rates for August. With regards to the German data, the current conditions index is expected to have declined to -16.0 from -13.5, while the economic sentiment index is forecast to have risen to -38.0 from -44.1. In the US, both IP and MP are forecast to have rebounded 0.2% mom, after sliding 0.2% and 0.4% respectively.

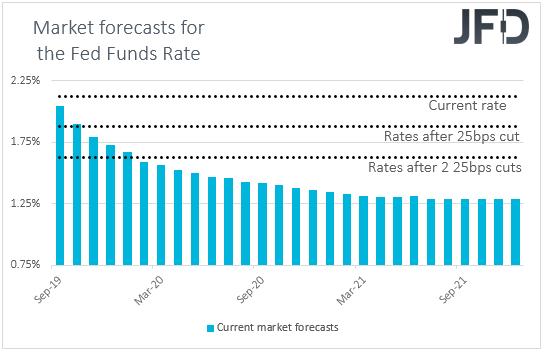

On Wednesday, all lights are likely to fall on the FOMC decision. This would be one of the “bigger meetings”, where apart from the decision, the statement and Chair Powell’s press conference, we will also get updated economic projections, including a new “dot plot”.

On September 6th, Fed Chair Powell repeated what he said at Jackson Hole, namely that the Committee will “act as appropriate” to keep economic expansion on track, comments that allowed market participants to keep elevated their bets with regards to this meeting. According to the Fed funds futures, the probability for such an action currently lies at 85%. Thus, if this is the case, all lights will turn to signals on how officials intend to move forward. In June, the 2019 median dot of their interest-rate projections pointed to no hikes this year. That said, 8 out of the 17 members were in favor of lower rates. One member voted for one cut, while the other seven supported the case of two. Since then, the Committee cut rates in July, and as we already noted, it is expected to deliver another one at this meeting. With investors almost factoring in another one to come by year end, it would be interesting to see whether the new dots will confirm that view or not.

As for Wednesday’s economic indicators, we get inflation data for August from the UK and Canada. In the UK, both the headline and core rates are expected to have declined to +1.9% yoy and +1.7% yoy, from +2.1% and +1.9% respectively. That said, barring any major deviations from the forecasts, GBP-traders are likely to pay more attention on the Supreme Court’s hearings on whether Parliament’s suspension was lawful or not. In Canada, the headline CPI rate is forecast to have remained unchanged at +2.0% yoy, while no forecast is available for the core one. Eurozone’s final CPIs, as well as the US building permits and housing starts, all for August, are also coming out.

On Thursday, four more central banks decide on interest rates. During the Asian day, we have the BoJ, while later in the day, it’s the turn of the SNB, the Norges Bank and the BoE.

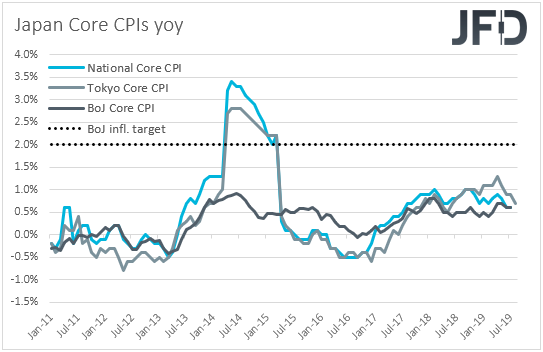

Kicking off with the BoJ, at their latest meeting, Japanese policymakers kept once again their ultra-loose policy unchanged, and maintained the forwards guidance that the current extremely low levels of interest rates are likely to stay unchanged “at least through spring 2020”. The Bank also added that it “will not hesitate to take additional easing measures if there is a greater possibility that the momentum toward achieving the price stability target will be lost”.

Concerns over the state of the global economy have grown since then, while all Japanese inflation metrics remained well below the Bank’s objective of 2%. What’s more, recent reports said that the Bank is now more open to discuss the possibility of further easing this week. Thus, all the focus will be on whether officials will decide to act as early as at this meeting, and if so, what tools they will use. The Bank has the options of cutting short-term rates further into the negative territory, cutting the 10-year yield target, increasing its asset buying pace, or using a combination of those measures.

Now passing the ball to the SNB, the big question here is whether this Bank will follow the footsteps of the ECB and cut interest rates further into the negative territory, or whether they would prefer to wait and see whether tensions between US and China would ease further, and thereby reduce demand for the safe-haven franc.

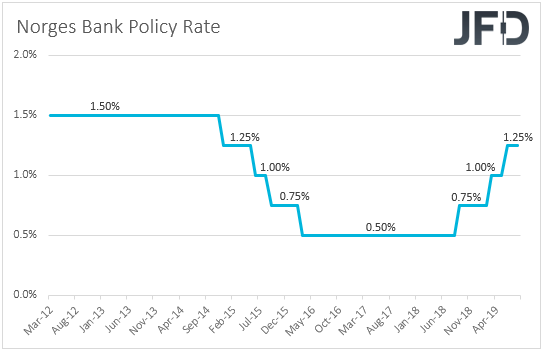

Flying from Switzerland to Norway, the Norges Bank is the only Bank on the agenda which is expected to hike rates. Latest inflation data showed that the headline CPI slowed to +1.6% yoy from +1.9%, while the core rate ticked down to +2.2% from +2.3%. This may have raised some doubts as to whether policymakers would indeed push the hike button at this meeting, but we don’t expect them to hesitate. We still see the case for a hike this week. We base our view on the fact that despite the slowdown, headline inflation is in-line with the Bank’s latest projections. Yes, the core rate is below its respective estimate of +2.3%, but it is still above the Bank’s aim of 2.0%. We will also pay extra attention to the Bank’s rate-path projections.

Finally, we have the BoE, but we don’t expect any changes from this Bank. At its latest meeting, the Bank decided to keep monetary policy unchanged and maintained the view that conditional upon a smooth Brexit, increases in interest rates at a gradual pace and to a limited extent, would be appropriate to return inflation sustainably to the 2% target. Bearing in mind that UK MPs have managed to pass a law that requires the government to ask for a new Brexit delay, as well as the latest GDP which eased fears over a recession in the UK economy, we don’t expect the Bank to abandon its hiking bias at this meeting, despite the potential slowdown in inflation on Wednesday. We expect a reiteration of the forward guidance, and given that there is no press conference to accompany the decision, we don’t expect any major market reaction.

As for Thursday’s data, New Zealand’s GDP for Q2 is forecast to have slowed to +0.4% qoq from +0.6%, something that will drive the yoy rate down to +2.0% from +2.5%, while Australia’s employment report for August is forecast to show that the unemployment rate has ticked up to +5.3% from +5.2%, and that the employment change has slowed to 10.0k from 41.1k in July. Later in the day, both the headline and core UK retail sales for August are expected to have declined 0.2% mom after rising by the same percentage in July.

Finally, on Friday, we get Japan’s National CPIs for August, and later in the day, we have Canada’s retail sales for July. No forecast is available for Japan’s headline CPI rate, but the core one is anticipated to have ticked down to +0.5% yoy from +0.6%. With regards to the Canadian data, headline sales are forecast to have risen 0.6% mom, after stagnating in June, while the core rate is expected to have declined to +0.4% mom from +0.9%.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

75% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.