Eurozone’s economy expanded at its slowest pace in 4 years according to yesterday’s preliminary data for Q3, raising even more concerns over the bloc’s performance. Another interesting point was the stagnation in Italy’s growth, which comes in the midst of the ongoing row between the nation and the EU over its budget. Overnight, the BoJ stood pat, but lowered its inflation projections.

Eurozone’s Growth Rate Hits a 4-year Low

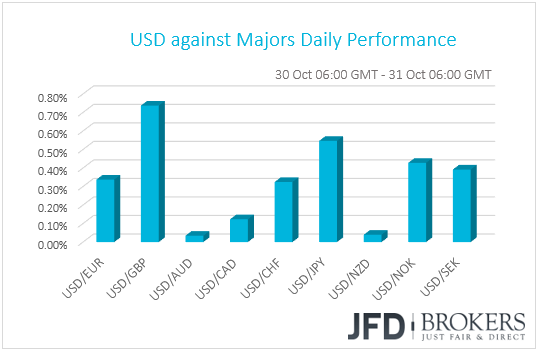

The dollar continued trading higher against most of the other G10 currencies on Tuesday. The main losers were GBP, JPY and NOK, while the currencies that managed to resist the greenback’s strength, ending the day virtually unchanged against it, were AUD and NZD.

The pound slid the most against the dollar after the S&P ratings agency said that a no-deal Brexit would result a moderate recession in the UK. With uncertainty surrounding the UK’s departure from the EU still elevated, we maintain our bearish view on the pound. Theresa May appears to be stuck between a rock and a hard place. It seems that the closer it gets in in finding common ground with the EU, the harder it becomes for any accord to be approved by the UK Parliament.

The resistance of the commodity-linked currencies and the weakening of the safe haven yen suggest that the relatively supported sentiment we saw on Monday rolled over into Tuesday. Although European bourses were mixed, US and major Asian indices were in positive territory.

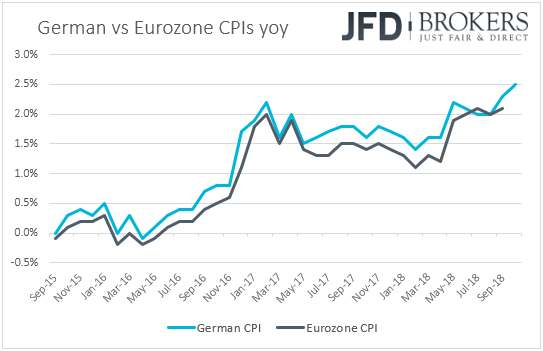

The mixed performance of the European markets may be owed to Eurozone’s disappointing growth data. The Euro Stoxx 50, the French CAC 40, the German DAX, and Italy’s FTSE MIB, all ended their trading in the red. Yesterday, the data showed that the bloc’s economy slowed to +0.2% qoq in Q3 from +0.4% in Q2, marking the slowest rate of expansion since Q3 2014. This has also dragged the yoy rate down to +1.7% from +2.2%, well below the ECB’s forecast for 2018, which is +2.0%.

At the latest ECB policy meeting, President Draghi maintained his fairly optimistic stance with regards to Euro area’s economic and inflation outlooks, but the data keep amplifying concerns over the bloc’s economic performance. Thus, market participants may have priced further out the possibility for an ECB hike by the end of 2019. The next ECB meeting is scheduled of the 13th of December, an if data continue coming on the soft side, it would be interesting to see whether Draghi would still consider the risks surrounding the Euro area growth outlook as broadly balanced.

Another interesting point in yesterday’s data was the stagnation in Italy’s growth for the quarter. This comes in the midst of the ongoing row between the Italian government and the EU Commission over the nation’s budget. Last week, the Commission rejected Italy’s plans and yesterday’s data make it even harder for EU officials to accept a budget deficit target of 2.4%, as the projections of the Italian government now look even more overly optimistic.

Despite recent reports suggesting that Italy could trim its budget target, Italy’s PM Giuseppe Conte said yesterday that his government will not change its 2019 target and that zero growth justifies the expansionary budget plans. His deputy, Matteo Salvini, echoed his remarks, saying “The slowing GDP is another reason to go full steam ahead with the budget”. This confirms our view to wait for handshakes before we start considering that this risk is out of the way.

In our view, the combination of the Italian budget deadlock and the increasing concerns over Eurozone’s economic performance are likely to keep the common currency under pressure, especially against the US dollar. The US economy is on a strong footing, while the Fed remains on track to keep raising rates, with the next hike perhaps coming in December. Bearing the latest boost in risk appetite, the euro could underperform the Aussie and the Kiwi as well. These commodity-linked currencies tend to get benefited when market sentiment improves.

EUR/AUD – Technical Outlook

EUR/AUD has been on a move lower since the beginning of October and it looks like that this could continue for the near term. The pair is still trading below its short-term downside resistance line taken from the high of the 23rd of October. Until that line is broken, we will aim for lower levels.

For now, we will keep monitoring the recent newly-found support area at 1.5955, a break of which could invite more bears to step in and drive EUR/AUD lower towards the 1.5910 obstacle, which acted as good support on the 29th of August. If the bears-pressure remains strong, we could see the pair making its way lower to test the 1.5830 barrier, marked by the low of the 24th of August. That said, let’s not forget a possible scenario where the pair could retrace a bit more to the upside and test the aforementioned downside line. If EUR/AUD is still not able to move above it, the sellers could see this as a good opportunity to step in and take advantage of the higher rate.

The RSI is currently below 50 and still has some room to move lower into the oversold territory, near the 20 area. The MACD is still in the negative zone and remains below the trigger line, which is not a positive indication for the pair in the short run.

On the other hand, a break above the aforementioned short-term downside resistance line could make the bears worry about the possibility for the pair to travel lower in the short-run. If EUR/AUD also gets a push above the 1.6150 hurdle, this is what could spook the bears, and the bulls could try and take charge of the next potential area of resistance at 1.6190, marked by the high of the 26th of October. A further acceleration of the rate could take the pair towards a test of the 1.6250 barrier, which held the rate down on the 23rd of October.

![]()

BoJ keeps Policy Untouched, Lowers Inflation Forecasts

Overnight, the Bank of Japan kept its ultra-loose policy unchanged via a 7-2 vote, maintaining short-term interest rates at -0.1% and the target of 10-year JGB yields around 0%. What’s more, officials reiterated that they intend to maintain the current extremely low levels in interest rates for an extended period of time.

In their quarterly report, officials trimmed their inflation forecasts for the current fiscal year to +0.9% yoy from 1.1%, and also lowered their projections for the next two years. Now, the Bank expects its core CPI to hit +1.5% in 2021, down from +1.6% previously, and well below its inflation aim of +2%. This enhances our longstanding view that BoJ policymakers have a long way to go before start considering a meaningful step towards normalizing policy.

The yen remained unfazed at the time of the release, confirming our view that the currency remains more sensitive to changes in the broader market sentiment rather than monetary policy. The same applies for the Swiss franc but given that this currency tends to be affected more by problems in Europe, the uncertainty surrounding the Italian budget is likely to keep an extra risk premium for this currency. Therefore, even if both currencies continue to weaken against the dollar, due to the recent switch to “risk on”, we expect the yen to weaken more, something that shifts the risks for CHF/JPY to the upside.

CHF/JPY – Technical Outlook

In this battle of the safe-haven’s, CHF is finally finding some stable grounds, from which it can push itself back to the upside. CHF/JPY had been declining from the second half of September, but it looks like that on the 26th of October a turning point has occurred, and the pair reversed back to the upside. Since then, CHF/JPY keeps forming higher lows and higher highs, and also is trading above its short-term upside support line drawn from the low of that day. As long as the upside line remains intact, we will target slightly higher levels.

A good push above the 112.760 level could open the door for CHF/JPY to make its way a bit higher towards the 113.20 area, marked by the high of the 24th of October. If that area is not able to withhold the bull-pressure, a break of it could set the stage for a further move higher, where the pair could meet the 113.70 resistance zone. In the recent past, the zone acted as good resistance on the 16th of October and support on the 9th of October. This is where the rate could stall, as CHF/JPY would be testing the 200 EMA.

The RSI is currently above 50 and points to upside. The MACD, after bottoming on the 26th of October, continues to travel higher. It still remains above its trigger line and has now entered the positive zone. Both indicators are in support of the above-mentioned idea.

Alternatively, a break below the aforementioned short-term upside support line, could be the first warning signal for the bulls. If after that CHF/JPY keeps falling further and clears the 112.10 obstacle, this could be a sign that the bulls are now abandoning the field and we could see a further slide towards the 111.55 area, marked by the low of the 26th of October. If the pair falls below that area, this is where more sellers could start joining in and driving CHF/JPY to the next possible resistance at 110.80, a break of which could open the way to the 110.30, which acted as strong support throughout the whole month of August.

![]()

As for Today’s Events

During the European day, we get Eurozone’s preliminary CPI data for October. Expectations are for the headline rate to have remained unchanged at +2.1% yoy, while the core rate is anticipated to have ticked back up to +1.0% yoy from +0.9%. That said, yesterday, data showed that Germany’s inflation for the month accelerated, something that tilts the risks surrounding the bloc’s headline print to the upside. An acceleration in Eurozone’s inflation could be a sign of relief after the slowdown in growth, but with the Italian budget matter still unresolved, we doubt that this data set could prove the catalyst for a change in euro’s downtrend.

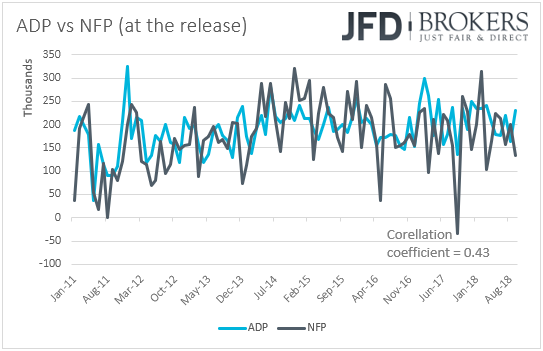

In the US, we have the ADP employment report for October. Expectations are for the private sector to have gained 190k jobs, less than the 230k in September, which could raise speculation that the NFP number, due out on Friday, could come near its forecast, which is 191k. That said, we repeat to the umpteenth time that, even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are taken into account) has been very low in recent years. Even last month, the ADP print rose to 230k, but the NFP number dropped to 134k.

From Canada, we have the monthly GDP for August, but no forecast is currently available.

As for the speakers, we have two on the agenda: BoC Governor Poloz spoke yesterday and is scheduled to speak again today. SNB Chairman Thomas Jordan steps up to the rostrum as well.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.