The euro tumbled yesterday after the ECB decided to push back its interest-rate guidance, officially announced a new round of TLTROs, and slashed its economic projections, keeping its growth risk assessment to the downside. As for today, investors may lock their gaze on the US employment data for February. Expectations are for a strong report, which could encourage market participants to place some bets with regards to a Fed hike this year.

ECB Pushes Guidance Back, Announces New TLTROs

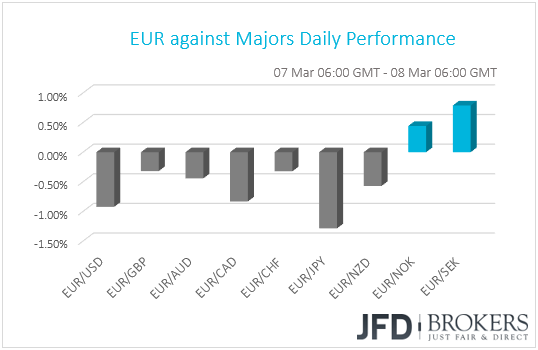

The euro traded lower against all but two of the other G10 currencies on Thursday. It underperformed the most against JPY, USD and CAD in that order, while it managed to eke out some gains only against SEK and NOK.

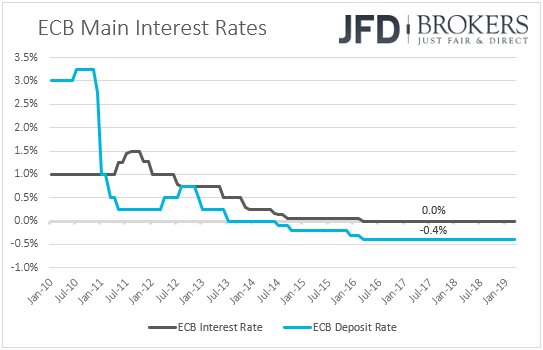

Yesterday, it was all about the ECB. The European Central Bank decided to keep all three of its interest rates unchanged as was broadly expected but proceeded with some bold changes within the accompanying statement. Policymakers pushed back their interest-rate forward guidance, noting that rates are likely to remain at current levels “at least through the end of 2019”, instead of “at least through the summer of 2019”, which was the case before. What’s more, they officially announced that they will launch a new series of TLTROs starting in September and ending in March 2021.

At the press conference following the decision, ECB President Mario Draghi reiterated that the risk surrounding the bloc’s growth outlook are “still tilted to the downside”, even after the aforementioned policy moves and even after the Bank slashed both its GDP and inflation projections. In the Q&A session, Draghi noted that this is because the new measures can’t actually address external factors weighing on Eurozone’s economy, such as the threat of protectionism, Brexit and emerging market vulnerabilities.

Yesterday, we noted that we will look for hints on whether the Bank could introduce a new round of TLROs at one of the upcoming meetings, but we also said that we didn’t expect a change in the forward guidance at this meeting. The outcome was more dovish than we have anticipated and apparently, it came as a surprise to many others as well. The euro tumbled across the board, with EUR/USD falling below 1.1200 for the first time since June 2017.

With the ECB officially confirming market expectations that a hike is off the table for this year, we see the case for the euro to continue losing ground against the dollar. Yes, the Fed also switched to a more dovish stance in January, but the market has mostly digested the idea, and after all, the Fed has not clearly ruled out a hike by year end. The greenback has been strengthening lately, perhaps as recent data eased concerns with regards to the health of the US economy, and bearing in mind that the market remains unwilling to price in any Fed hikes at the moment, a March “dot plot” pointing to even one 25bps increase this year could prove positive for the dollar.

EUR/USD – Technical Outlook

It was a bad day yesterday for the euro-bulls, as the common currency sold off against most of its major counterparts. Looking at the EUR/USD chart, we can see that the pair broke below its November low at 1.1215 and headed further south. It only managed to find good support near the 1.1175 hurdle, marked by the low of June 29th, 2017. For now, we believe the pair may continue sliding lower, but before that, it might retrace slightly back up, a move we will only see as a temporary correction.

A potential push back up could lead to a test of the above-mentioned 1.1215 hurdle, this time from underneath. If the rate fails to get above it, then the pair might get hit with another wave of selling, which could drag it back down towards the 1.1175 support area. If this time that support area fails to withhold the bear-pressure, then a break of it could push EUR/USD lower, where the next potential support zone could be at 1.1140, which is the low of June 22nd, 2017.

Alternatively, in order to aim back up again, at least towards this week’s highs, we would like to see a firm push back up above the 1.1233 barrier, which is the low of February 15th. This way, the buying momentum might pick up again and the door to the 1.1260 obstacle could be open again. If at that point the bulls will not be willing to ease off, the rate could break the 1.1260 obstacle and accelerate further, towards the 1.1290 resistance, which marks the low of Wednesday.

![]()

Spotlight Turns to US Jobs Data

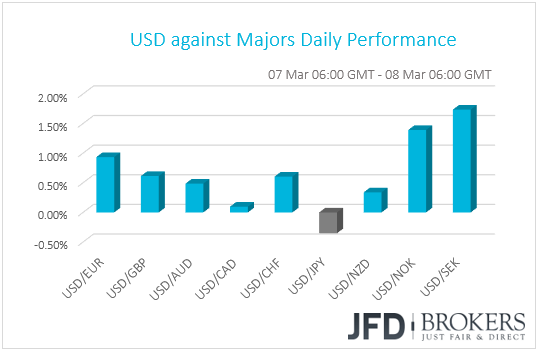

Speaking about the Fed and the dollar, the US currency rebounded against all but two of the other G10 currencies, gaining the most against SEK, NOK and EUR in that order. It lost some ground only versus JPY, while it traded virtually unchanged against CAD.

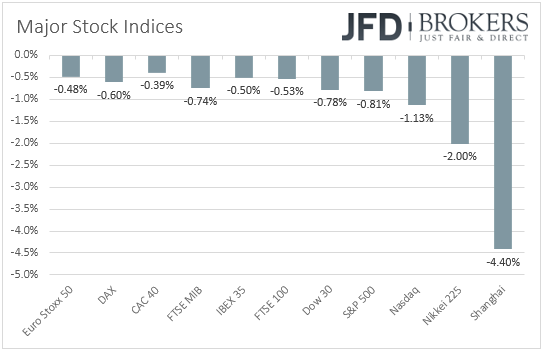

Although not so clear by the overall FX performance, the strengthening of the US dollar and the yen suggests that the broader sentiment was subdued. Indeed, EU and US indices were a sea of red yesterday, with the negative investor morale rolling into the Asian morning Friday. Japan’s Nikkei 225 ended its session 2.00% lower, while China’s Shanghai Composite slid 4.40%.

With no clear catalyst behind investors risk-averse mood, we assume that one possible driver may be the ECB decision. Usually a dovish outcome is positive for equities and risk assets, but the fact that the Bank kept its growth risk assessment to the downside, even after the measures it took, may have sparked fresh fears with regards to global economic growth. China’s disappointing trade data overnight may have added to those fears, evident by the fact that the Shanghai index was the big loser. The nation’s trade surplus shrank to USD 4.1bn in February from nearly USD 39.2bn in January, with both imports and exports tumbling by much more than anticipated.

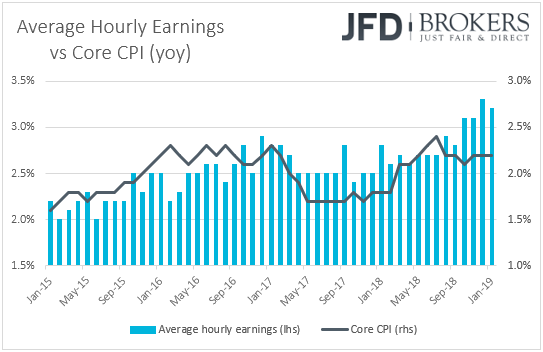

As for today, investors are likely to lock their gaze on the US employment report for February. Expectations are for nonfarm payrolls to have risen 181k, less than January’s 304k, but still a healthy number. The unemployment rate is forecast to have declined to 3.9% from 4.0%, while average hourly earnings are anticipated to have accelerated to +0.3% mom from +0.1%. Barring any revisions to the prior monthly prints, this is likely to drive the yoy rate up to +3.3% yoy from +3.2%, as the monthly print of February 2018 that will drop out of the yearly calculation is +0.1%.

Overall, the numbers point to a strong report, consistent with further tightening in the labor market. Although Fed Vice Chair Richard Clarida noted last week that wage gains are no putting upward pressure on inflation, further acceleration in earnings may eventually lead to somewhat higher consumer prices. Following the latest upbeat data from the US, especially last week’s GDP data which eased concerns of a severe slowdown, a robust employment report could reduce the likelihood of a Fed cut in 2019, and may encourage market participants to put some hike bets on the table. According to the Fed funds futures, investors are nearly 85% confident that the Committee will refrain from pushing the hiking button this year, while the probability for a rate cut has increased to 15%, perhaps due to the aforementioned fears over the global economic outlook. The chance for a hike has dropped to 0%.

USD/CHF – Technical Outlook

This whole week the bulls have remained behind the steering wheel of USD/CHF, which moved from the a low of around 0.9980 and managed to hit strong resistance at 1.0125, which is near the high of November 13th. The pair is also trading above its short-term upside support line drawn from the low of February 28th. At the time of this analysis, we can see that the rate is declining, but as long as USD/CHF remains above that short-term uptrend line, we will class this move lower just as a correction before another move higher.

If the pair continues to travel lower, but fails to get below the 1.0070 hurdle, or the aforementioned upside line, we could see the bulls re-joining the battlefield again and pushing back up. This is when we will target yesterday’s high, at 1.0125, a break of which could open the door to areas which were last time seen in March 2017. The first potential target could be the 1.0142 barrier, a break of which could allow USD/CHF to travel further north to test the highest point of March 2017, at 1.0170.

On the other hand, a break of the previously-mentioned upside line and also a drop below the 1.0060 hurdle, could spook the buyers from the arena in favour of the sellers. This is when the rate might continue falling, potentially testing a strong support area between the 1.0023 and 1.0029 levels, where the last one acted as a very strong resistance between February 20th and March 4th. If even this support zone will be no match for the bears, then a break below it could lead the pair to the 0.9980 obstacle, which as we have mentioned before, marks the low of this week.

![]()

As for the Rest of Today’s Events

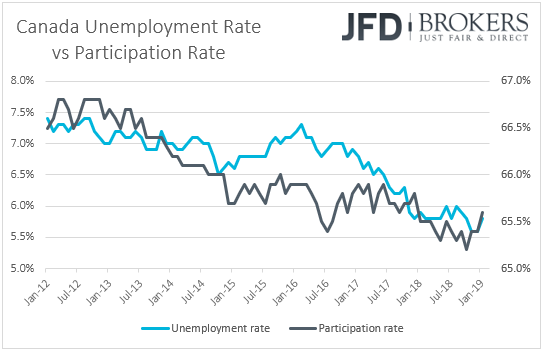

Apart from the US jobs report, we also get employment data from Canada. The unemployment rate is expected to have ticked down to 5.7% from 5.8%, but the net change in employment is expected to show a decline of 5k jobs after a 66.8k gain in January. Given that the participation rate is expected to have declined as well, we believe that the potential slide in the unemployment rate may be owed to unemployed people stop looking actively for a job, instead of more people being employed. Following Wednesday’s dovish shift by the BoC, a weak report may add to speculation that the Bank is unlikely to push the hiking button this year.

US building permits and housing starts for January are also coming out, as well as Canada’s housing starts for February.

As for the speakers, ECB Executive Board member Yves Mersch will step up to the rostrum.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

76% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.