European equities were a sea of green yesterday, supported by S&P’s decision on Friday not to downgrade Italy’s credit rating. Although the US markets closed negative, mainly due to reports that the US is preparing more tariffs on Chinese goods, Asian stocks bounced after US President Trump predicted a “great deal” with China. Tonight, the BoJ concludes its two-day gathering, but no change in policy is expected.

Sentiment Gets Boosted by Italy’s Rating Relief and Trump’s Remarks on Trade

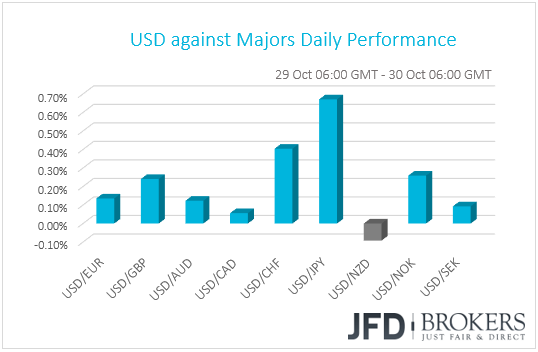

The dollar traded higher against most of the other G10 currencies yesterday. It gained the most against the safe havens JPY and CHF, while it lost ground only against NZD. The greenback traded virtually unchanged against CAD, while AUD was among the currencies that managed to resist, ending only slightly down.

In our view, the FX-performance pattern suggests a “risk on” day overall. Indeed, most EU indices were a sea of green, perhaps boosted by S&P’s decision on Friday to maintain Italy’s credit rating at BBB, although lowering the outlook to negative, as well as by reports citing sources saying that Italy could reduce the budget deficit below 2.4% if a couple of the budget pillars prove less costly than initially anticipated.

However, the US indices closed their session negative, after a Bloomberg report noted that the US is preparing to announce tariffs on all the remaining imported goods from China, which according to last year’s import data, may worth USD 257bn. According to the report, the announcement is conditioned upon a scenario where talks between US President Trump and his Chinese counterpart Xi Jinping, scheduled for next month, do not yield any material progress over trade. That said, the sentiment was switched back to ‘risk on’ after the US President noted that he predicts a “great deal” with China on trade. During the Asian morning Tuesday, most Asian markets rose, with Japan’s Nikkei 225 and China’s Shanghai Composite closing 1.44% and 1.02% up respectively.

Back to the currencies, the euro was also supported by the news over the Italian budget, but its gains remained limited, and reversed against some of its counterparts, after German Chancellor Angela Merkel decided to not seek re-election as the head of her party, and that this would be her fourth and last term as the nation’s Chancellor. Her decision came a day after her CDU party, as well as her coalition partner SPD, suffered heavy losses in Hesse’s regional elections.

With the SPD threatening to end the alliance with the CDU if there are no tangible policy results by next year’s mid-term review, uncertainty emerging from the German political scene is an extra headache for EUR-traders in our view, who are likely to stay cautious over Italy’s budget. Despite signs of a softer stance by the Italian government, the matter is far from resolved. As we noted last week, we need to see handshakes between EU and Italian officials before we consider that risk to be out of the way.

FTSE 100 – Technical Outlook

On Friday last week, we saw the FTSE 100 cash index bouncing off from the lows near the 6850 level and pushing itself higher. Yesterday, the UK index had a bit of a choppy session, but nevertheless didn’t roll over below the recent lows and held strong. Even though, on a bigger picture, FTSE 100 still forms lower lows and lower highs, and continues to trade below the medium-term downside resistance line drawn from the high of the 8th of August, from the short-term perspective, the index is now trading within a range between the 6920 and 7090 levels. For now, we remain flat and wait for a break through one of the sides of that range.

On the upside, a break above the 7090 resistance level could open the door towards the next potential area at 7180, marked by the low of the 9th of October. If the bulls remain in control of the enclave there, this could give them a possibility to charge the next possible resistance zone near the 7245 hurdle, which held the price from moving higher on the 10th of October.

The RSI is currently above 50 and points higher. The MACD has now entered the positive zone and also points to the upside, at the same time being above its trigger line. Both indicators are in support of the idea discussed above.

On the other hand, if the FTSE 100 decides to move back down sharply and breaks below the 6920 level, marked by yesterday’s and the 11th of October’s lows, this could lead the index towards a test of the lowest point of last week, near 6850. A break of that obstacle could open the door to much lower levels. If the bears remain strong, they could easily pull the FTSE 100 to the 6800 hurdle, which was the inside swing high of the 5th of December 2016.

![]()

Bank of Japan Decides on Monetary Policy

Tonight, during the Asian morning Wednesday, the BoJ concludes its two-day monetary policy gathering. The latest meeting passed unnoticed with the Bank keeping is policy framework unchanged via a 7-2 vote and maintaining the view that Japan’s economy is expanding moderately. What’s more, officials reiterated that they intend to maintain the current extremely low levels in interest rates for an extended period of time.

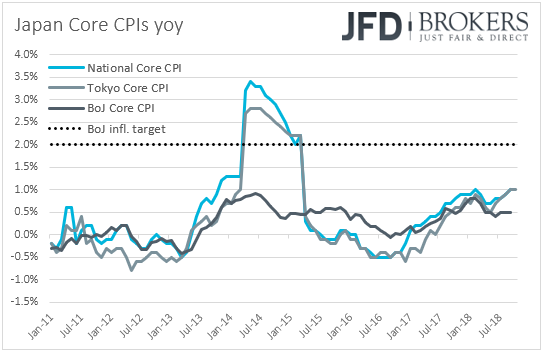

Latest inflation data showed that the nation’s headline CPI rate ticked down to +1.2% yoy from +1.3%, while the core print rose to +1.0% yoy from +0.9%. That said, the BoJ’s own core CPI metric stood unchanged at +0.5% yoy. Therefore, with all inflation metrics well below the Bank’s objective of 2%, we see it hard for policymakers proceeding with further policy changes after the tweaks announced in July.

Yesterday, a report citing people familiar with the matter noted that the Bank is considering some more tweaks to its bond buying operations, such as reducing the frequency of purchases or changing slightly the timing, in order to encourage more trading between financial institutions. That said, the sources noted that the Bank is in no rush to implement the changes, something suggesting that this is unlikely to happen at this meeting. However, even if it happens, we don’t expect any major reaction from the yen. The Bank has been already tweaking the sizes and frequency of its operations lately in order to control the yield curve and thus, we doubt that the market would take this as a material change. As long as the Bank maintains its policy ultra-loose without signaling a strong tapering, we believe that the yen is likely to remain more sensitive to changes in the broader market sentiment, instead of small technical tweaks in monetary policy.

EUR/JPY – Technical Outlook

Last Friday, EUR/JPY showed a good strong reversal back to the upside and since then it continues to drag higher. From the short-term perspective, the pair could continue climbing, but the issue here is the downside resistance line drawn from the 26th of September, which could hold the rate down. Even though we could see EUR/JPY moving a bit more to the upside towards the downside line, as long as that line remains intact, we will aim back down again in the near term.

Today, EUR/JPY got held by the 128.30 resistance level, marked by the low of the 18th of October. If the pair manages to push through that level, it could open the path for itself towards the aforementioned downside resistance line. If that line continues to hold, the bears could see this as a good opportunity to take advantage of the higher rate and push it back down to the same 128.30 zone, or even a bit lower towards the 127.70 hurdle. That hurdle acted as a good bouncing ground for EUR/JPY this morning and was also a good resistance level last Friday.

The RSI and the MACD are somewhat in support of the short-term upside scenario discussed above. The RSI is currently above 50, which is a good sign for the bulls. The MACD, after bottoming last Friday, continues to push higher towards the zero line. The indicator is still negative, but above its trigger line, which gives some hope for the buyers.

The alternative scenario could come into play if EUR/JPY breaks the previously mentioned short-term downside resistance line and closes above the 129.15 resistance area. This way, we could see more buyer coming in and taking a slightly longer-term position. The next potential resistance obstacle to watch could be near 129.70, a break of which could lead to the 130.20 barrier, marked by the high of the 22nd of October.

![]()

As for Today’s Events

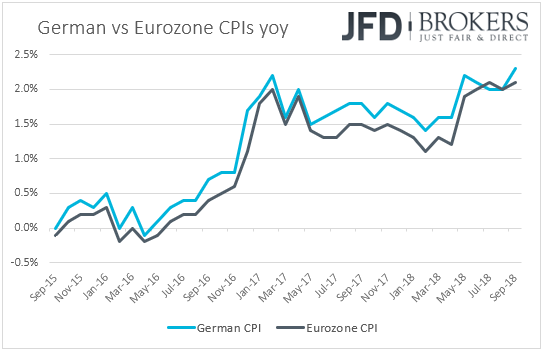

Apart from politics, EUR-traders are likely to keep an eye on Germany’s preliminary CPI data for October, as well as Eurozone’s 1st estimate of Q3 GDP. Getting the ball rolling with Germany’s data, expectations are for both the CPI and HICP rates to have risen to +2.4% yoy, from +2.3% and +2.2% respectively. Something like that could raise speculation that Eurozone’s headline CPI rate, due out tomorrow, may rise as well. With regards to the bloc’s GDP, the forecast suggests that the Euro area economy continued growing at the same pace as in Q1 and Q2, which is +0.4% qoq. Combined, the data may calm somewhat investors’ fears over Eurozone’s economic performance, but we expect participants to stay on guard ahead of the bloc’s inflation numbers, due out tomorrow. Even if the euro recovers somewhat on the data, we expect political uncertainty surrounding Italy and Germany to keep any gains short lived.

From the US, we get the Conference Board consumer confidence index for October, which is expected to have slid to 136.0 from 138.4 in September. That said, the overall trend of the index remains positive and thus, we wouldn’t consider such a setback as a signal of deterioration in consumers’ morale.

With regards to the energy market, we get the American Petroleum Institute (API) weekly crude inventory report, but as usual, no forecast is available.

As for the Asian morning Wednesday, besides the BoJ decision, Australia’s inflation data for Q3 are coming out as well. The headline CPI rate is forecast to have slid to +1.9% yoy from +2.1% in Q2, while the trimmed mean rate is forecast to have remained untouched at +1.9% yoy. Both rates are expected to be above the RBA’s latest forecasts for the second half of the year, but below the lower end of the 2-3% inflation target range. Thus, we see it hard for investors to alter their view around the RBA’s policy plans. According to the Bank’s latest quarterly Statement on Monetary Policy, the cash rate is expected to increase around the end of next year.

We also have one speaker on today’s agenda: BoC Governor Stephen Poloz.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.