Most major EU and US indices ended higher yesterday, perhaps due to the European Commission’s plans to loosen Covid-related restrictions on tourism, as well as largely upbeat earnings season. Today, Asian trading, the RBA decided to keep its policy settings untouched, but said that at the July meeting they will consider future bond purchases following the completion of the second AUD 100bln purchases in September.

Stocks Gain as Covid Restrictions are Lifted, RBA to Consider More QE

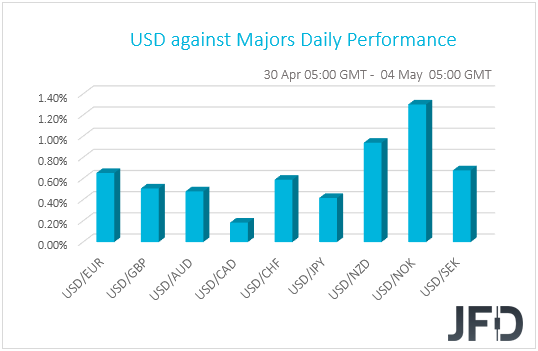

The US dollar traded higher on Friday, and although it pulled back somewhat on Monday, it remained elevated against all the other G10 currencies. It advanced the most against NOK, NZD, EUR, and CHF in that order, while it eked out the least gains versus CAD.

The greenback rally on Friday may have been the result of end-of-month portfolio rebalancing, with international investors perhaps loading up on US treasuries. Remarks by Dallas Fed President Robert Kaplan that he and his colleagues should start discussing QE tapering may have also encouraged some USD buying. However, Fed Chair Powell maintained a cautious stance, noting that the economy is doing better but is “not out of the woods yet”. Indeed, latest data support the notion. Yesterday, the ISM manufacturing PMI for April slid to 60.7 from 64.7, at a time when the forecast was for a rise to 65.0, warning participants not to be overly excited.

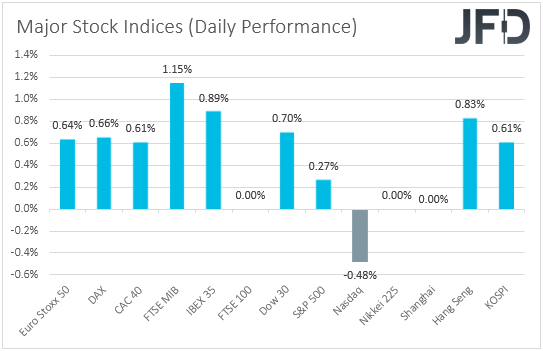

Leaving the FX sphere and traveling to the equity world, we see that yesterday, most major EU and US indices ended higher. perhaps due to the European Commission’s plans to loosen Covid-related restrictions on tourism, as well as a largely upbeat earnings season. The exceptions were UK’s FTSE 100, which stayed closed due to a bank holiday, and Wall Street’s Nasdaq, which slid 0.48% as investors have been rotating into cyclical and “reopening” stocks. Megacap tech stocks, the likes of Amazon, Alphabet, Facebook, and Microsoft, traded south, despite reporting upbeat results last week. As for today in Asia, Japanese and Chinese markets were closed due to holidays. Otherwise, sentiment appeared to have remained supported. Both Hong Kong’s Hang Seng and South Korea’s KOSPI are up 0.83% and 0.61% respectively.

Overall, we stick to our guns that with most economies around the globe now reopening due to the improving pace in the vaccination rollouts, the Fed’s willingness to stay accommodative for longer, and US President Biden’s pledge to pass more supportive bills, the broader market sentiment is very likely to stay supported. We believe that equity markets may continue trending north, while the US dollar and other safe havens, like the yen, may come under renewed selling interest. This could happen as early as this Friday, when the US employment report is due to be released, with the forecast pointing to another round of stellar job gains.

Now, flying to Australia, today, during the Asian trading, the RBA decided on monetary policy. As it was widely anticipated, the Bank kept all its policy settings unchanged, repeating that “the economic recovery in Australia has been stronger than expected and is forecast to continue”. That said, officials added that despite the strong recovery, inflation pressures remain subdued in most parts of the economy, and thus, at the July meeting they will consider future bond purchases following the completion of the second AUD 100bln purchases in September. This means that, similarly to the Fed, the RBA is committed to stay extra-loose for long, at least until actual inflation is sustainably within its 2-3% target, something they don’t see happening until 2024 the earliest.

In our view, the RBA’s pledge to keep its policy loose in the years to come may be a relatively negative factor for the Aussie. However, the Bank noted that the currency remains near the upper end of the range of recent years, which means that they are not too concerned about its value. With that in mind, we would consider the path of list resistance for this currency as actually being to the upside. The extra-loose monetary policy stances outside Australia as well, like in the US and the Eurozone, are likely to keep the broader market sentiment supported, and thus, as a risk-linked currency, the Aussie may benefit as well.

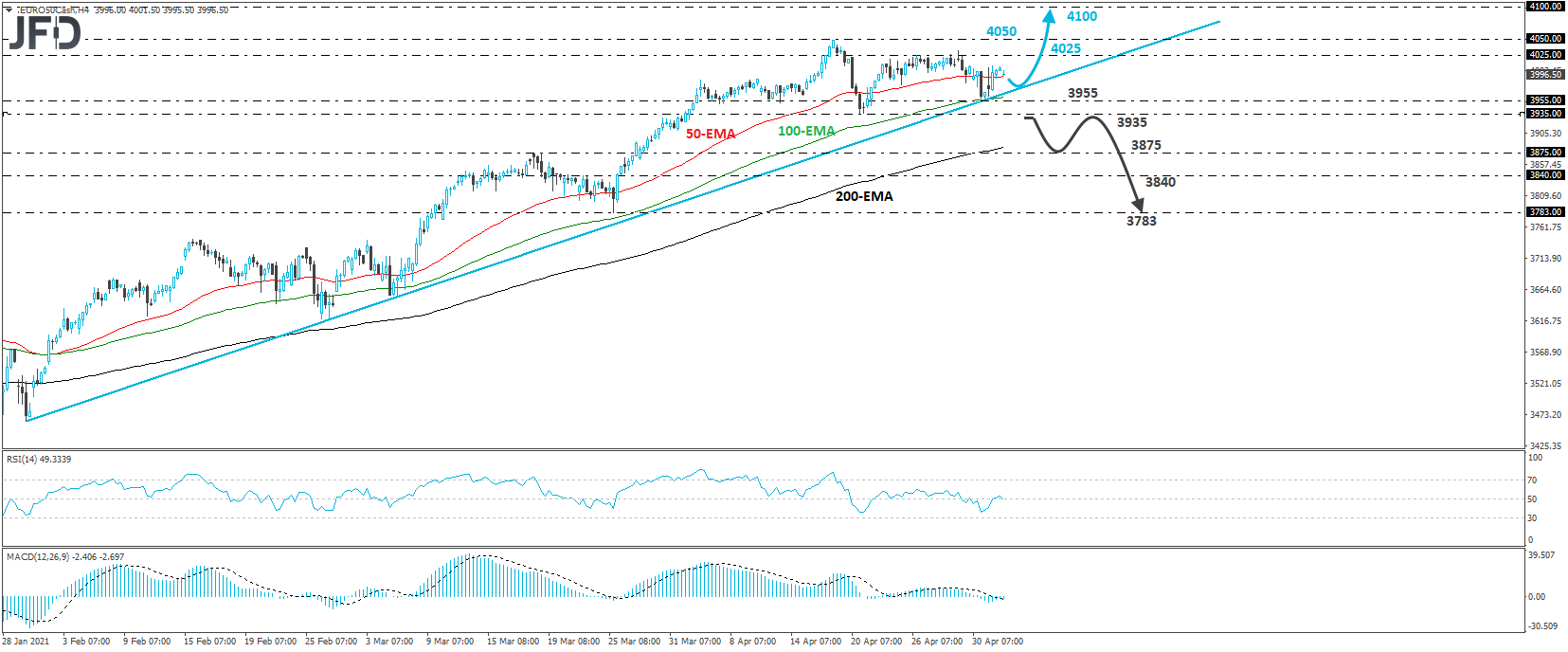

Euro Stoxx 50 – Technical Outlook

The Euro Stoxx cash index traded higher yesterday, after hitting support slightly above Friday’s low of 3955. Although investors have failed to form a forthcoming higher high since hitting 4050 on April 16th, the index continues to trade above the upside support line drawn from the low of January 29th, and thus, we would consider the near-term outlook to still be positive.

The index may pull back again and perhaps test that upside line, but if market participants take control from near that support zone, we would expect them to aim for another test near 4050. If they manage to overcome that obstacle this time around, we may see them sailing towards the 4100 territory, marked as a resistance by the low of the last week of March 2007.

On the downside, we would like to see a decisive dip below 3935 before we start examining the case over a potential short-term reversal. This will not only take the price below the aforementioned upside line, but it will also confirm a forthcoming lower low on the 4-hour and daily charts. The stock may then slide to the 3875 zone, marked by the inside swing high of March 18th, the break of which could trigger extensions towards the inside swing highs of March 22nd and 23rd, at around 3840. Another break, below 3840, could pave the way toward the low of March 25th, near 3783.

AUD/JPY – Technical Outlook

AUD/JPY has been trading in a consolidative manner recently, staying between the 84.42 and 84.75 barriers. Zooming out though, we can see that the rate continues to balance above the upside support line drawn from the low of March 24th, while since April 22nd, it has been supported by a steeper shorter upside line. In our view, all this paints a relatively positive picture.

A break above 84.75 may encourage the bulls to target the peak of April 29th, at 85.00, the break of which would confirm a forthcoming higher high and may see scope for extensions towards the high of March 18th, at around 85.45.

Now, in case the rate drops below 84.42, it will also be placed below the upside line taken from the low of April 22nd. This may signal the beginning of a corrective phase to the downside, and may initially prompt the bears to target Friday’s low of around 84.13. A break lower may extend the fall towards the 83.92 barrier, marked by the inside swing high of April 21st, or towards the 83.74 area, defined as a support by the inside swing high of April 23rd.

As for the Rest of Today’s Events

We have the final UK manufacturing PMI for April, which is expected to confirm its initial estimate, as well as the US and Canadian trade balances for March. The US deficit is forecast to have widened somewhat, while Canada’s surplus is anticipated to have decreased. With regards to the energy market, we get the API (American Petroleum Institute) report on crude oil inventories for last week, but as it is always the case, no forecast is available.

Tonight, during the Asian session Wednesday, New Zealand’s employment report for Q1 is due to be released. The unemployment rate is forecast to have held steady at 4.9%, while the net change in employment is expected to have slowed to +0.2% qoq from +0.6%. The labor costs index is anticipated to have stayed unchanged at +1.5% yoy.

At its prior gathering, the RBNZ kept its policy untouched, staying prepared to lower the OCR further if required, and adding that a prolonged period of time is most likely to pass before their objectives are met. Although the CPIs for Q1 surprised to the upside, the yoy rate remained below the midpoint of the Bank’s target range of 1-3%, and thus, in our view, a slowdown in jobs growth will allow officials to remain ready to cut interest rates if deemed necessary.

We also have a speaker on today’s agenda, and this is San Francisco Fed President Mary Daly.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 79.07% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.