For another week, market participants are likely to keep their gaze locked on the crisis in Ukraine, with risk aversion dominating the financial world. However, we do have some other economically important events on this week’s agenda and those are the ECB decision, with investors eager to find out how the Bank’s plans have changed following the geopolitical tensions, the US CPIs, which could revive expectations over aggressive tightening by the Fed, as well as Canada’s jobs data, which could add credence to the case over a BoC hike at the upcoming gathering.

On Monday, the calendar appears very light, with the only releases worth mentioning being Germany’s factory orders and retail sales for January. Factory orders are expected to have slowed to +1.0% mom from +2.8%, while retail sales are anticipated to have rebounded 1.8% mom after falling 5.5% in December.

On Tuesday, during the European session, Germany releases its industrial production data for January, while from the Eurozone as a whole, we get the final estimate of Q4 GDP, as well as the employment change for that quarter. Germany’s IP is expected to have rebounded 0.5% mom after sliding 0.3% in December, while Eurozone’s GDP is expected to confirm its second estimate of +0.3% qoq. No forecast is currently available for the employment change.

Later in the day, we get trade data for January from both the US and Canada. The US trade deficit is expected to have widened to USD 87.10bn from 80.70bn, while Canada’s CAD 0.14bn deficit is anticipated to have turned into a 2.00bn surplus.

On Wednesday, Japan’s final GDP for Q4, as well as China’s CPI an PPI rates for February, are coming out. Japan’s qoq growth rate is expected to be revised up to +1.4% from +1.3%, while both the Chinese rates are expected to have slid somewhat. Specifically, the CPI is anticipated to have ticked down to +0.8% yoy from +0.9%, while the PPI is forecast to have slid to +8.7% form +9.1%.

On Thursday, the economic agenda becomes more interesting, as we have both the ECB decision and the US CPIs for February.

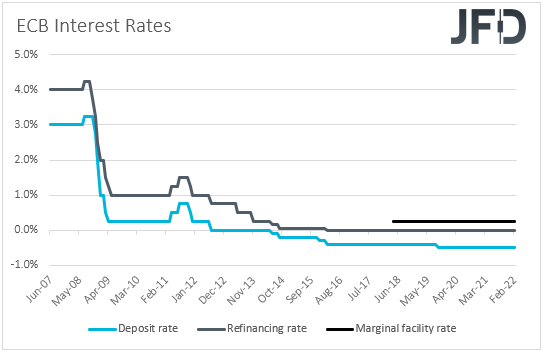

Kicking off with the ECB, at its last gathering, this Bank kept policy untouched, but at the press conference following the decision, President Lagarde said that inflation remained elevated for longer than previously thought and that the economy was hurt less than anticipated by the pandemic. She also added that the March and June meetings would be essential for evaluating their guidance, which means that they could, after all, decide to lift rates this year.

Since then, inflation accelerated further, but we also witnessed the crisis in Ukraine, which may well undermine economic growth in Europe. Also, let’s not forget that Lagarde pushed against expectations over a summer rate increase, even before Russia’s invasion in Ukraine. Thus, we expect the Bank to highlight the risks arising from the war, and signal that it will take a more patient approach on interest rates than previously thought. That said, they will still need to fight inflation pressures, and they may decide to do so by ending their asset purchases earlier.

In any case, a dovish take on interest rates could add extra pressure on the already wounded euro. Even if the outcome is not as dovish as anticipated, and due to that, the euro spikes higher, we expect any recovery to be limited and short-lived. As long as the crisis in Ukraine continues, we will hold a bearish stance against the common currency.

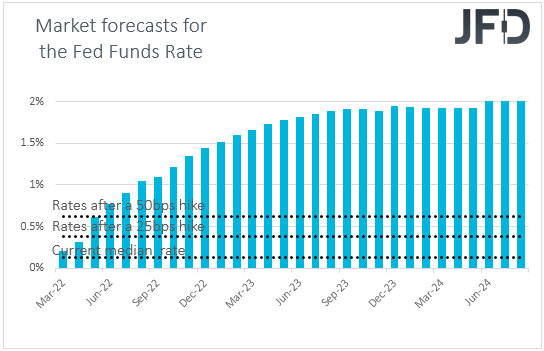

Now, passing the ball to the US CPIs, expectations are for the headline rate to have risen further, to +7.9% yoy from +7.5%, but the core one is anticipated to have ticked down to +5.9% yoy from 6.0%. In our view, this suggests that the main contributor to the spike in headline inflation may be the surging energy prices.

Last week, when testifying before Congress, Fed Chair Jerome Powell said that he may support a quarter-point hike at the upcoming gathering, disappointing those expecting a 50bps rise. However, he also added that he is ready to use larger or more frequent rate hikes if inflation doesn’t slow. Thus, despite underlying inflation expected to have slowed somewhat, both rates are still well above the Fed’s objective of 2%, and with energy prices keep surging, the headline rate could continue rising in the months to come as well. Thus, if the forecasts are met, we see decent chances for market participants to bring forward their hike expectations, something which could support further the US dollar, and add more pressure to equities.

Finally, on Friday, during the early European session, we get the monthly UK GDP for January, alongside the industrial and manufacturing production rates for the month. No forecast is available for the GDP, while both the IP and MP rates are expected to have held steady at +0.3% mom and +0.2% mom respectively.

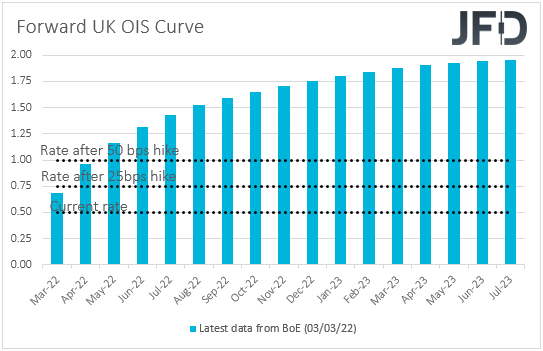

At the latest BoE gathering, officials voted 5-4 for a hike by 25bps, with the 4 dissenters calling for a 50bps increase. Since then, we’ve been highlighting that only one member needed to be convinced for that to happen at the upcoming gathering, and the accelerating CPIs for January, indeed, added to speculation on that front. However, this was the case around a week before Russia invaded Ukraine, with the events unfolding since then, marketwise, raising concerns over the global economic performance, and especially in Europe, something evident by the tumbles in the euro and the pound.

Thus, with all that in mind, we don’t believe that the BoE will now stay willing to hike by 50bps at its upcoming gathering, even if Friday’s data come in better than expected. Actually, we now question officials’ willingness to even hike by 25bps. In any case, according to the UK OIS (Overnight Index Swaps) forward curve, market participants believe that a quarter-point hike could still be delivered. The nation’s trade balance for January, is also coming out, but no forecast is available.

Germany’s final CPIs for February are also coming out at the same time as the UK data, but as it is always the case, they are expected to confirm their preliminary estimates.

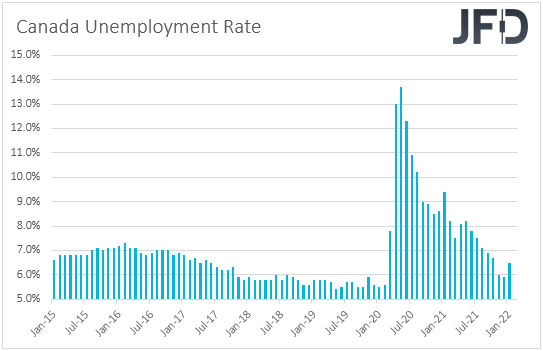

Later in the day, Canada’s employment report for February is scheduled to be released. The unemployment rate is expected to have slid to 6.2% from 6.5%, while the employment change is forecast to show that the economy has added back 160.0k jobs after losing 200.1k in January.

In our view, this will be a decent report, which, following the better-than-expected GDP for Q4 last week, as well as the upside surprise in the Canadian CPIs for January, could increase speculation over a rate hike by the BoC at its upcoming gathering. Let’s not forget that, although officials stood pat last time, they noted that they expect rates to increase and that the overall economic slack is now absorbed.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.82% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2022 JFD Group Ltd.