This week, we have two central banks deciding on monetary policy and those are the ECB and the BoC. Following the latest rally in bond yields, ECB officials sounded concerned and thus, it would be interesting to see whether they will signal more action soon. With regards to the BoC, latest data have been on the weak side and thus, we expect a more dovish language than previously. In the US, rising inflation may add more fuel to the latest rise in yields.

On Monday, there are no major events or economic releases on the schedule.

On Tuesday, the calendar appears relatively light as well. During the Asian session, we have Japan’s final GDP for Q4, which is expected to confirm its preliminary estimate of +3.0% qoq. China’s trade balance for February is also due to be released and the forecast suggests that the nation’s surplus has narrowed.

Later in the day, we get final GDP data for Q4 from the Eurozone as well, and expectations are for a confirmation of the second estimate of -0.6% qoq.

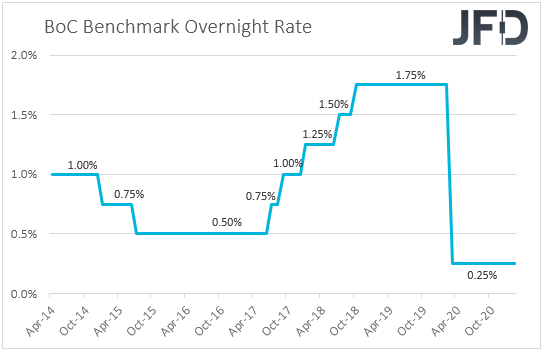

On Wednesday, we have a central bank deciding on monetary policy, and this is the BoC. At its prior meeting, the BoC decided to keep interest rates and the pace of its QE purchases unchanged, disappointing those expecting a small cut or even a re-increase in QE. Officials also noted that “As the Governing Council gains confidence in the strength of the recovery, the pace of net purchases of Government of Canada bonds will be adjusted as required", which suggests that the next policy step for BoC may be tapering QE.

However, the employment report for January disappointed, with the unemployment rate rising to 9.4% from 8.9%, and the net change in employment showing that the economy has lost 212.8k jobs. What’s more, although the CPIs for January came in better than expected, they still stayed below the BoC’s inflation aim of 2%, while last week, GDP data showed that the Canadian economy has slowed more than anticipated in December. Thus, with that in mind, we don’t believe that tapering may be on the cards for the months to come. We expect BoC officials to sound more dovish this time around, diminishing expectations on that front, something that could hurt the Canadian dollar. That said, we expect any retreat in the Loonie to be temporary. With oil prices surging after the decision from OPEC and its allies to not increase output, the Loonie is likely to stay supported as well, especially against the yen, given that the BoJ is pledged to keep its long-term government bond yields near zero.

As for Wednesday’s data, during the Asian morning, we have China’s CPI and PPI for February. The CPI rate is forecast to have slid to -0.4% yoy from -0.3%, while the PPI one is anticipated to have rallied to +1.5% yoy from +0.3%.

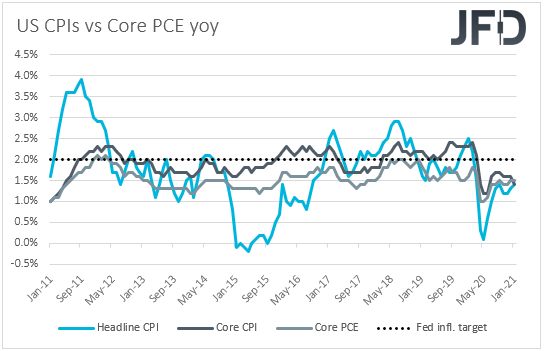

Later in the day, we get inflation data for February from the US as well. Given the latest surge in bond yields, which has been attributed to fears over high inflation in the not-too-distant future, this data set may attract special attention this time around. The headline rate is forecast to have risen to +1.7% yoy from +1.4%, while the core one is anticipated to have held steady at 1.4% yoy. In our view, rising headline inflation may add to concerns over high inflation and thereby push yields higher. As a result, the US dollar could strengthen and equities could slide more.

Having said all that though, we stick to our guns that the decline in equities may be a corrective phase. The reason is that the Fed has noted that they will not tighten policy even if inflation overshoots 2% in the months to come. They clearly said that they expect such a spike to be temporary and that inflation will rise and stay above 2% for some time – the goal for the beginning of normalization – in the years after 2023. As a result, we expect fears over high inflation to ease in the foreseeable future, which may allow equities and other risk-linked assets to rebound. As for the dollar, it may come under selling interest on more signs that the Fed is likely to stay accommodative for longer than previously assumed.

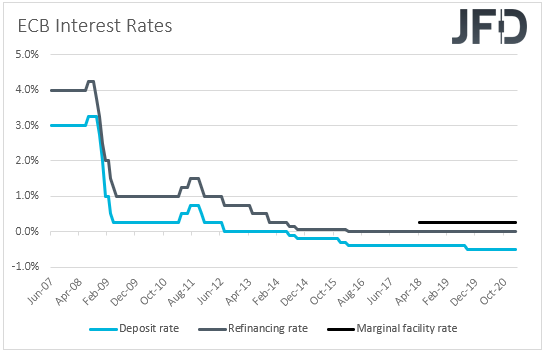

On Thursday, the central bank torch will be passed to the ECB. Despite the lockdown measures around the Eurozone, at the press conference following the latest ECB meeting, President Lagarde said that the downside risks to the economic outlook are now “less pronounced”, making investors skeptical over further easing.

However, following the latest rally in bond yields, ECB officials have been worried, noting that the rise has been “unwarranted” as the Eurozone’s economic recovery is still fragile and the vaccination process has been much slower than in the UK and the US. Rising bond yields in Europe have partly spilled over from US markets reacting to President Biden’s massive fiscal stimulus. Therefore, it would be interesting to see whether the ECB will turn dovish again, perhaps signaling that more easing may be required soon, or whether they will just say that the situation is worth monitoring closely. With the US dollar having the tendency to benefit from rising US yields, we believe that EUR/USD may be poised to slide if indeed the ECB shows intention to react.

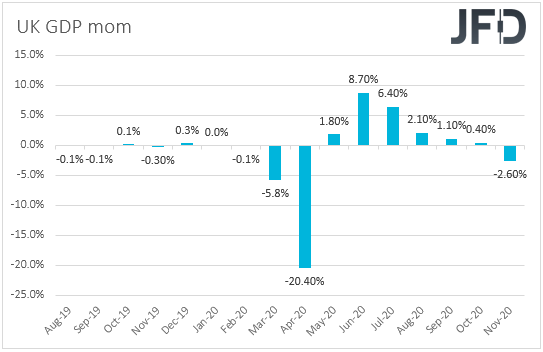

Finally, on Friday, market participants may turn their gaze to UK data. The UK monthly GDP for January is coming out, but no forecast is currently available. We also get the nation’s industrial and manufacturing production, as well as the trade balance for the month. IP and MP are forecast to have slid 0.5% mom and 0.7% mom respectively, after rising 0.2% and 0.3% in December, while the trade balance is forecast to show that the nation’s deficit has narrowed.

In our view, potentially sliding IP and MP increase the chances for a contractionary GDP print, but bearing in mind that the UK has been in full lockdown during the month of January, this may not come as a surprise. Thus, we will stick to our guns that with the vaccinations proceeding very well in the UK, and with BoE officials being aligned with the relaxed views of the Fed over the rally in bond yields around the globe, the pound may continue performing well, especially against the yen. That’s because, as we already noted, the BoJ’s policy is to keep its government bond yields close to zero.

As for the rest of Friday’s releases, Germany’s final CPIs for February are forecast to confirm their preliminary estimates, while Eurozone’s industrial production is anticipated to have rebounded 0.3% mom in January, after contracting 1.6% in December. From Canada, we get the employment report for February. The unemployment rate is forecast to have ticked down to 9.3% from 9.4%, while the employment change is expected to show that the economy has gained 52.5k jobs after losing 212.8k in January. In the US, the preliminary UoM consumer sentiment index for March is coming out and the forecast points to an increase to 78.0 from 76.8.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 79.07% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.