The US dollar pulled back yesterday, but equities traded lower suggesting that market participants remained concerned and in the absence of major developments yesterday, the reasons remain the same as the last few days: persistently high inflation, the deadlock in US Congress over the debt ceiling, and fears of Evergrande defaulting after it missed a second offshore bond payment.

USD Retreats, But Equities Slide as Investors Remain Worried

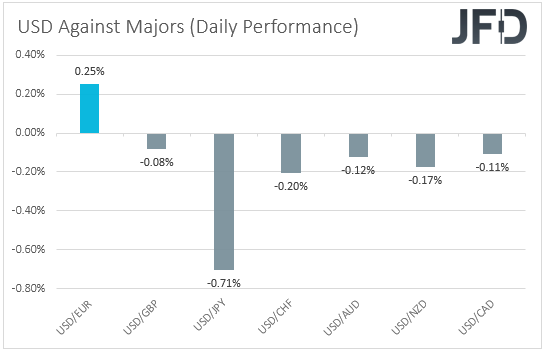

The US dollar pulled back against all but one of the other major currencies on Thursday and during the Asian session Friday. It gained only versus EUR, while it slid the most against JPY.

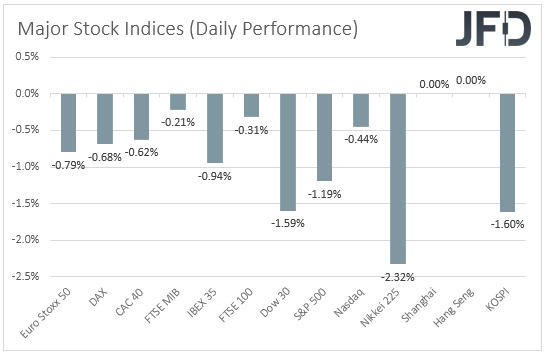

The performance in the FX world does not paint a clear picture with regards to the broader market sentiment this time around. The strengthening of the yen suggests a risk-off environment, but the retreat of the US dollar points otherwise. Thus, in order to clear things up, we prefer to turn our gaze to the equity world. There, we see that major EU and US indices closed in negative territory, with risk aversion rolling into the Asian session today. Both Japan’s Nikkei 225 and South Korea’s KOSPI fell 2.32% and 1.60% respectively. China’s Shanghai Composite and Hong Kong’s Hang Seng remained closed.

In our view, despite the pullback in the US dollar, the performance in the equity world suggests that market participants remain concerned and in the absence of major developments yesterday, the reasons remain the same as the last few days: persistently high inflation, the deadlock in US Congress over the debt ceiling, and fears of Evergrande defaulting after it missed a second offshore bond payment.

So, why did the dollar retreat? Market chatter suggests that this may have been due to initial jobless claims rising by more than anticipated last week. But this would have proved positive for equities, at least the US ones, as it could mean that the labor market is not at the desired state, which may be a reason for delaying the beginning of QE tapering. In our view, the dollar may have pulled back due to some profit taking after its latest steep rally. Perhaps some participants decided to lock some profits in the end of the month, and re-evaluate whether to jump back into the action at a later stage. We believe that, even if the retreat continues for a while more, the fundamental background remains the same and thus, we would expect the greenback to rebound and continue trending north for a while more.

As for today, the most important piece of data on the agenda is Eurozone’s preliminary CPIs for September. The headline CPI rate is expected to have risen to +3.3% yoy from +3.0%, while the HICP excluding energy and food one is anticipated to have inched up to +1.9% yoy from +1.6%. Despite the headline rate moving further above the ECB’s objective of 2%, underlying inflation is expected to stay below that target, something that may allow the ECB to stay accommodative for longer than other central banks. Remember that at their latest meeting, officials of this Bank announced a “moderately lower pace” in its Pandemic Emergency Purchase Program (PEPP) purchases but made it clear that this is not a tapering move, and that when PEPP is over, they have all the other tools available. Thus, we expect the euro to stay under selling interest, especially against the dollar, given that the Fed is anticipated to start scaling back QE in November, and perhaps start raising interest rates next year.

DJIA – Technical Outlook

The Dow Jones Industrial Average cash index tumbled again yesterday, and today, during the Asian session, it hit the 33615 support, marked by the low of September 20th. Even if we see another round of buying, the price structure has been of lower highs and lower lows recently, which paints a negative short-term picture.

A potential recovery may extend towards the 34260 zone, marked by the inside swing low of September 28th, but we see decent chances for the bears to jump back into the action from near that zone. Another slide could result in another test at 33615, the break of which will confirm a forthcoming lower low and perhaps see scope for extensions towards the 33030 territory, defined as a support by the low of June 21st.

On the upside, we will abandon the short-term bearish case, only if we see a break above yesterday’s high of 34680. This will confirm a forthcoming higher high on the 4-hour chart, and could aim for Tuesday’s peak, at 34985, or the high of September 10th, at 35110. Another break higher could extend the advance towards the 35280 zone, which provided strong support between August 31st and September 6th.

EUR/USD – Technical Outlook

EUR/USD fell sharply on Wednesday, breaking below the 1.1665 barrier, which provided support on August 19th and 20th. Yesterday, the pair hit support at around 1.1563, and then, it consolidated somewhat. Overall, the rate continues to trade well below the downside resistance line drawn from the high of September 3rd and thus, we would consider the short-term picture to still be negative.

The current consolidation suggests that we may see a corrective bounce soon, perhaps even above 1.1610, which is yesterday’s high. However, the rate would still be below the aforementioned downside line and the bears may take charge again from below the 1.1665 barrier. This may result in another slide to the 1.1563 level, the break of which could pave the way towards the 1.1505 level, marked by the low of July 22nd, or the psychological figure of 1.1500.

On the upside, we would like to see a recovery all the way above the 1.1725 zone to start examining whether the outlook has turned bullish. This could confirm the break above the pre-mentioned downtrend line and could initially target the 1.1749 zone, marked by the high of September 23rd. A break above that zone could trigger extensions towards the 1.1790/1.1797 zone, the break of which could encourage more advances, perhaps towards the peak of September 15th, at 1.1832.

As for the Rest of Today’s Events

Besides the Eurozone CPIs, later in the day, from the US, we have the personal income and spending numbers for August, as well as the core PCE index for the month. The ISM manufacturing index for September is also on the agenda and the forecast points to a small decline, to 59.5 from 59.9. From Canada, we get the monthly GDP for July.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.90% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.