The Kiwi and the Aussie were the main losers among the G10s, perhaps due to the weaker-than-expected Chinese data overnight, which weighed on Asian equity markets as well. Yesterday, the ECB kept interest rates unchanged and formally ended its QE program. The euro slid after President Draghi, although he repeated that the risks surrounding the Euro area outlook remain broadly balanced, said that the balance of risks is moving to the downside.

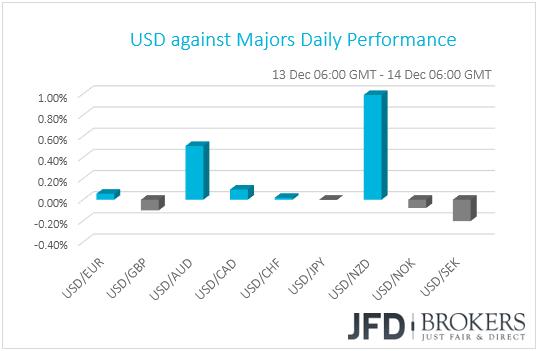

NZD and AUD the Big Losers as Chinese Data Disappoint

The dollar traded mixed against the other G10 currencies. It gained nearly 1.0% against NZD, which was the main loser, and around 0.5% against AUD. It slightly outperformed CAD as well. The greenback was somewhat lower versus SEK and GBP, while it was found virtually unchanged against EUR, CHF, JPY and NOK.

The Kiwi and the Aussie were the main losers, perhaps feeling the heat of the weaker-than-expected Chinese data overnight. Although fixed asset investment accelerated as expected, retail sales slowed to their weakest yoy rate since 2003, while industrial production grew by the slowest in nearly three years. The data add to evidence that the US-China trade conflict continued to take a toll on Chinese growth, despite policy efforts to boost the economy. The Kiwi may have been also weighed by the RBNZ’s release that it is considering to increase the capital banks need to hold, in order to strengthen the financial system’s resilience to financial shocks.

The Chinese data weighed on Asian equity markets as well and prompted some participants to seek shelter to safe havens, like yen. Japan’s Nikkei 225 and China’s Shanghai Composite Index closed 2.09% and 1.53% lower. That said, it’s hard to say that this suggests a broader reversal in investors’ morale. Bearing the positive developments surrounding the US-China trade sequel, any further declines may stay limited and short-lived. Barring any headlines suggesting that tensions between the world’s two largest economies are flaring up again, investors’ risk appetite may improve again soon, and equities could rebound.

Back to the currencies, the Swiss franc barely moved after the SNB decision, with the Bank keeping interest rates unchanged. Officials repeated that they will remain active in the foreign exchange market as necessary, and that the franc remains highly valued. They also downgraded their inflation projections. Swiss policymakers do not see inflation hitting their 2% target, even in Q3 2021. In September, they anticipated that this could happen in Q2 2021.

The Norwegian Krone strengthened after the Norges Bank maintained the guidance that interest rates are likely to be raised in Q1 2019, noting that this will most likely happen in March. What’s more, the statement accompanying the decision had a hawkish flavor, with officials saying that the upturn in the economy appears to be continuing, without mentioning anywhere the slowdown in mainland GDP for Q3. In any case, the currency pared gains, and traded virtually unchanged against its US counterpart.

AUD/JPY – Technical Outlook

In the early hours of the Asian morning today, AUD/JPY sold off and broke the short-term tentative upside line, drawn from the low of this week, which kept holding the rate from falling. Now, it looks like the pair could be heading back down to the levels, where it started off the week. For now, we will aim for slightly lower levels, but given that further declines could be limited near the tentative upside line taken from the lowest point of October, we would be more careful as we approach that line.

As we can see, AUD/JPY is already trading below one of its key support hurdles at 81.64, marked by Wednesday’s low, which leads us to an idea that there could be a bit more selling on the way. If so, then the next potential support zone we could look at would be the 81.30 obstacle, a break of which may push the pair further down for a re-test of the 81.05 level, marked by the low of the 10th of December. This is where AUD/JPY could meet the short-term tentative upside line taken from the lowest point of October, which might hold the rate from moving further down.

On the upside, in order to consider AUD/JPY traveling higher again, we would need to see a push back above the 81.95 obstacle, marked by yesterday’s intraday swing low. But for a better confirmation of seeing a higher high, the pair would have to rise above this week’s high, near the 82.20 level. If the bulls start believing in themselves again, a further acceleration of the rate could lead towards the 82.55 resistance zone, which was the intraday high of the 5th of December.

![]()

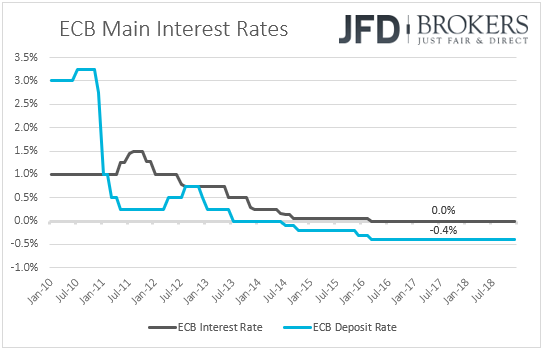

ECB Ends QE, Draghi Continues to See Balanced Risks

The euro was also among the currencies that traded virtually unchanged against the US dollar, but its day was not so quiet either. Once again, for around an hour, it was at the mercy of Draghi’s words at the press conference following the ECB policy meeting. Ahead of the conference, the Bank kept all three interest rates unchanged as was widely anticipated and formally ended its asset purchasing program. The statement was more or less the same as the previous one, with officials reiterating that rates are likely to stay untouched “at least through the summer of 2019”. The only change was that they gave more emphasis to reinvestments of the purchased securities, noting that they intend to continue reinvesting, in full, the principal payments for an extended period of time past the date when interest rates will start rising.

At the press conference, Draghi noted that while incoming data has been weaker than expected, the underlying strength of domestic demand continues to underpin the euro area expansion and rising inflation pressures. Most importantly, he repeated that “The risks surrounding the euro area growth outlook can still be assessed as broadly balanced.” However, he added that the balance of risks is moving to the downside due to the persistence of uncertainties related to geopolitical factors, the threat of protectionism, vulnerabilities in emerging markets and financial market volatility.

This part may have woken EUR-bears up, with EUR/USD sliding around 50 pips. That said, the pair recovered after the conference was over, perhaps due to the fact that Draghi still assessed the risks as balanced and not as tilted to the downside. When asked whether the Council had a discussion over changing the language around the economic outlook, the ECB Chief said that the decision was unanimous, which probably means that other members share the same view.

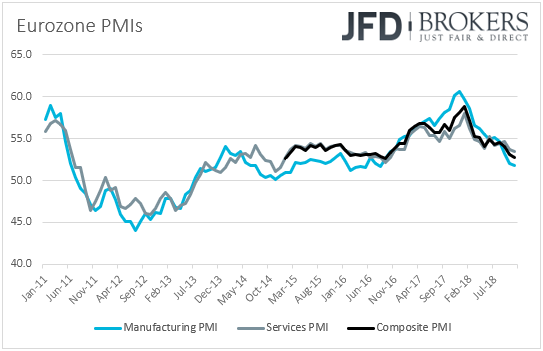

Focus for EUR-traders shifts back to economic data and the preliminary PMIs for December from several European nations and the Eurozone as a whole. Both the bloc’s manufacturing and services indices are expected to tick up to 51.9 and 53.5 from 51.8 and 53.4 respectively, which is likely to drive the composite PMI up to 52.8 from 52.7. Although still a marginal rebound, this could spark some hopes of stability, especially with the composite index hitting its lowest level since September 2016 last month. Now in case of a disappointment, the single currency could come under renewed selling interest as investors will start raising bets that Draghi and co. will change their language around the economic outlook at the turn of the year, noting that the risks have shifted to the downside.

Eurozone’s wages and the Labor Cost Index for Q3 are also coming out but no forecasts are currently available. Yesterday, Draghi noted that even though underlying inflation remains muted, its expected to increase over the medium term, supported by monetary policy measures, the ongoing economic expansion and rising wage growth. Thus, it would be interesting to see whether these indices will point to accelerating (or slowing) wages. The first case would confirm Draghi’s words and could ease concerns around the low level of the underlying inflation rate. On the other hand, declining wage growth may add to investors worries, especially if it is combined with sliding PMIs, fueling further any potential slide in the euro.

EUR/NZD – Technical Outlook

During the Asian morning today, EUR/NZD got a strong boost, which led the pair to break the medium-term downside resistance line, drawn from the high of the 10th of October. It seems that this could be portrayed as a potential change in the near-term direction. But in order to consider this scenario, we have to see EUR/NZD closing this week above that downside line. Because the break has only just happened, and we still have a full trading day ahead of us, we will take a cautiously-bullish approach for now.

Certainly, we could see a bit of retracement to the downside, but if EUR/NZD fails to move back below the aforementioned downside line or the 1.6665 hurdle, marked by Monday’s high, this could mean that the bears are losing the battle. This is when the pair could experience another leg of buying that could lift the rate to the 1.6790 zone, which was the high of the 22nd of November. If there is still interest in EUR/NZD among traders, we could see it moving further up, where the next potential target might be the 1.6875 obstacle, a break of which may lead the pair towards the 1.7060 area. That area was marked by the low of the 2nd of November.

On the hand, a strong push back down below the above-mentioned downside line and a break below the 1.6625 hurdle could make the bulls worry, as this could open the way for EUR/NZD to move lower again. That said, the bears might enjoy their dominance only for a bit, as the pair could get held by the short-term upside support line taken from the low of the 5th of December. The level to watch around there could be the 1.6510, marked by yesterday’s low. If that upside line fails to withhold the rate from dropping lower, this could lead EUR/NZD to re-test the 1.6425 area, which was the Wednesday’s low.

![]()

As for the Rest of Today’s Events

We get preliminary PMIs for December from the US as well. The Markit manufacturing print is expected to have declined to 55.1 from 55.3, while the services index is forecast to have remained unchanged at 54.7. The US retail sales and industrial production, both for November, are also scheduled to be released. Retail sales are anticipated to have slowed in both headline and core terms, while industrial production is expected to have accelerated somewhat.

We also have two ECB speakers on the schedule: ECB Executive Board member Sabine Lautenschläger and ECB Supervisory Board member Ignazio Angeloni.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.