There are no major central banks deciding on monetary policy this week, but that is far from suggesting a quiet trading activity. We have several companies reporting their earnings results, while in terms of economic data, we get Canada’s and New Zealand’s CPIs for March and Q1 respectively, as well as the preliminary PMIs for April from the Eurozone, the UK and the US, releases which could well reshape expectations around monetary policy. On Thursday, we will get to hear from Fed Chair Jerome Powell, while on Sunday, it is the second round of the French election, with incumbent President Macron racing against Marine Le Pen.

On Monday, during the Asian session, we already got China’s GDP for Q1, as well as the nation’s fixed asset investment, industrial production, and retail sales, all for the month of March. Economic activity slowed somewhat in the first quarter, but not as much as the forecast suggested, something that took the yoy GDP rate up to +4.8% from 4.0%. Industrial production and fixed asset investment also slowed by less than anticipated. Only retail sales came in worse than expected, with the yoy rate diving further into the negative territory.

As for the rest of the day, we don’t have any major economic release on the agenda, as it is Easter Monday for most nations under our radar. However, we do get some earnings results, with both the Bank of America and Bank of New York Mellon reporting today ahead of the US open. The season kicks into higher gear during the rest of the week, with reports including Netflix on Tuesday and Tesla on Wednesday.

On Tuesday, the only items on the economic agenda worth mentioning are the US building permits and housing starts for March, with both expected to have declined somewhat.

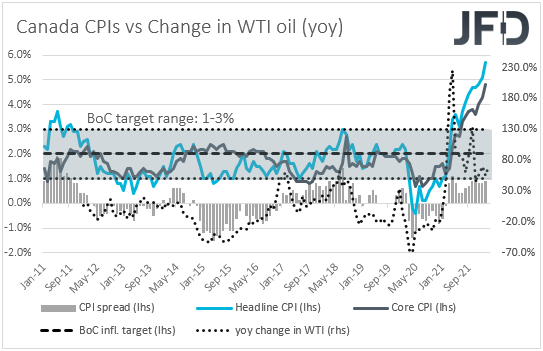

On Wednesday, the main item on the agenda is Canada’s CPIs for March. The headline rate is forecast to have risen to +6.1% yoy from +5.7% yoy, but the core one is forecast to have slid to 4.5% from 4.8%. This could mean that the rise in the headline rate may be due to temporary factors, like food and energy. However, a core rate at +4.5% is still well above the BoC’s objective of 2%, and it is unlikely to alter the BoC’s policy plans.

Remember that last week, the Bank hiked by 50bps, with Governor Macklem stressing the need for higher rates and adding that they are prepared to move more aggressively if the situation warrants so. Thus, even if the core CPI rate slides somewhat, we still see the case for the BoC to lift rates higher in the months to come. This is likely to keep the Loonie supported against currencies like the yen, the euro, and the Aussie, the central banks of which are not so hawkish. Yes, market expectations with regards to the RBA are very hawkish, but the Bank itself has not officially confirmed whether that’s realistic, at least not yet. On the other hand, a potential slide in Canada’s underlying inflation could bring the currency under some selling interest against the US dollar, as it could mean that, yes, the BoC could continue hiking rates, but not as aggressively as the Fed.

As for the rest of Wednesday’s events, Eurozone’s industrial production for February is coming out and the forecast points to a slowdown to +0.8% mom from +1.3%. Nonetheless, this is likely to drive the yoy rate up to +0.8% from -1.3%.

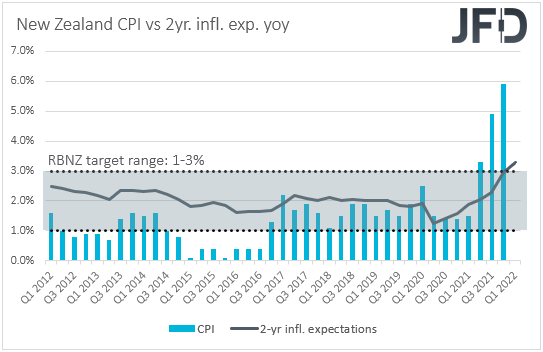

On Thursday, during the Asians session, we get more CPIs, this time from New Zealand and for the whole Q1 of 2022. The qoq rate is anticipated to have risen to +2.0% from +1.4%, something that would drive the yoy one up to +7.1% from 5.9%.

Last week, the RBNZ lifted its OCR by 50bps as well, but, although the Kiwi spiked higher initially, it was quick to give back those gains and trade even lower in the aftermath. In our view, this was because the RBNZ said that it remained comfortable with the outlook for the OCR as outlined in February, and that the larger move was intended to provide more policy flexibility. In other words, they hiked by more now, but they could slow down later. Nevertheless, further acceleration in inflation is unlikely to allow policymakers to calm down so easily. Expectations of more bold actions may increase, which could result in a corrective bounce in the Kiwi.

Later in the day, we get inflation data from the Eurozone for the month of March. However, this will be the final data for the month, and as it is always the case, both the headline and core rates are forecast to confirm their preliminary estimates. The euro is unlikely to respond to this set.

During the US session, Fed Chair Jerome Powell is scheduled to speak at the spring meeting of the International Monetary Fund, while later in the day, he is due to take part in a panel discussion along with ECB President Christine Lagarde.

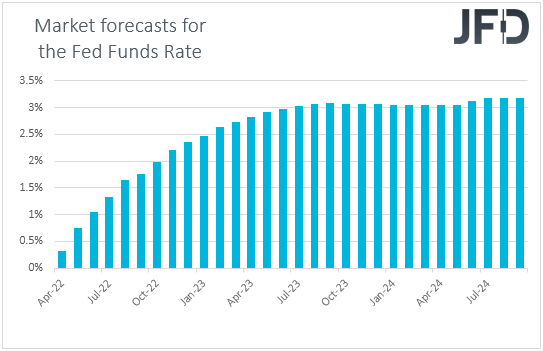

After raising interest rates at its latest gathering, the FOMC is now expected to deliver a double hike when it meets next, while there is a nearly 65% chance for another 50bps liftoff in June. Investors are even assigning a 30% chance for a triple hike in June. Thus, with that in mind, it will be interesting to see whether Powell will maintain an ultra-hawkish tone, something that could encourage some more dollar buying.

At the same time, following a cautious approach at last week’s ECB meeting, we don’t expect Lagarde to sound similarly aggressive. At the press conference following last week’s gathering, she said that they will only start raising rates “some time” after the end of the APP, which is expected in Q3. It could be weeks or even several months, she added. Therefore, we expect her to stick to her guns, something that could highlight again the divergence between the Fed and the ECB, and perhaps push the EUR/USD pair even lower.

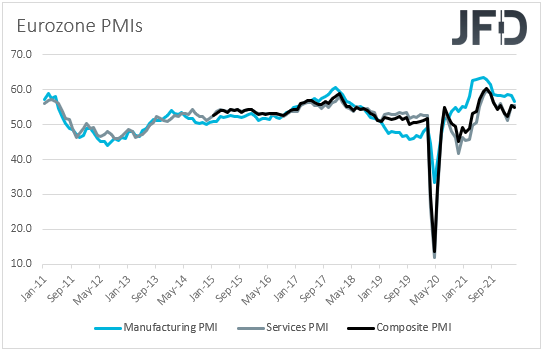

On Friday, most of the market attention is likely to fall on the preliminary PMIs for April from the Eurozone, the UK, and the US. Both Eurozone’s manufacturing and services indices are expected to have slid, but to have remained above the boom-or-bust zone of 50, which separates expansion from contraction. This is likely to take the composite PMI down to 54.0 from 54.9.

Further slowdown in Eurozone’s economic activity is likely to confirm the notion that the ECB may need to proceed more carefully with raising interest rates than some other major central banks, like the Fed, the BoE, and the BoC.

There are no forecasts for the UK PMIs, while in the US, expectations are for a fractional decline in the manufacturing index, and no change in the services one, with both indices staying near the 58 handle.

As for the rest of Friday’s events, during the Asian trading, Japan’s National CPIs for March are coming out, while later in the day, we get retail sales from the UK and Canada, for the months of March and February respectively.

Finally, on Sunday, we have the second round of the French Presidential Elections, with the final TV debate scheduled for Wednesday. The opinion polls suggest a 53% support for incumbent President Emmanuel Macron against 47% for challenger Marine Le Pen, suggesting a very tight fight on April 24th.

Le Pen is a Eurosceptic candidate, and, although she ditched past ambitions for a “Frexit” or getting out of the euro, a potential victory of hers could mean an 180-degree spin for France, from being a driving force for European integration to being more cautious on EU decisions and plans. With that in mind, we suspect that a Le Pen victory may be negative for the euro, while the opposite may be true in case Macron comes out victorious. However, we don’t believe that a potential rebound could also signal a trend reversal, as the common currency could continue feeling the heat of the uncertainty surrounding the war in Ukraine, the slowdown in Eurozone’s economic activity, and the divergence in monetary policy between the ECB and other major central banks, like the Fed and the BoE.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.82% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2022 JFD Group Ltd.