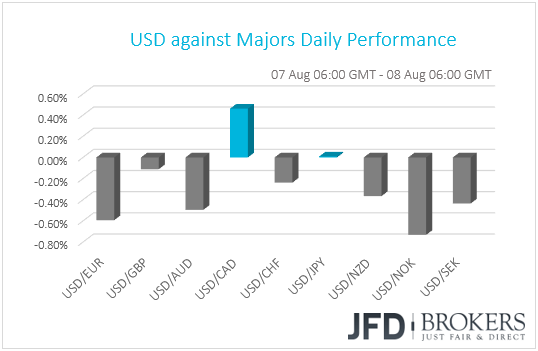

The Loonie was the main loser among the G10s yesterday, retreating from a near 2-month high against the dollar, perhaps due to the Saudi-Canada dispute. As for tonight, Kiwi traders will be sitting on the edge of their seats in anticipation of the RBNZ monetary policy decision.

Loonie Gets Hit by Saudi-Canada Dispute

The dollar traded lower against all but two of the other G10 currencies on Tuesday. It gained against CAD, while it traded virtually unchanged against JPY. The main winners against the greenback were NOK, EUR and AUD in that order.

The Canadian dollar was yesterday’s big loser, pulling back from an almost 2-month high against its US counterpart, perhaps due to the dispute between Saudi Arabia and Canada. On Sunday, the kingdom suspended diplomatic ties and new trade dealings with Canada after Canada called for the release of women’s rights activists. The tumble in the Loonie came as Canada’s equity market reopened on Tuesday following a holiday on Monday, with the S&P/TSX Composite index ending the trading session 0.82% down.

That said, the trade relationship between the two nations is worth less than USD 4bn a year, something that may not be enough to weigh further on the Canadian currency. Thus, we stick to our guns that the Loonie is likely to resume its latest uptrend, especially against the pound which got hit hard by BoE’s cautious stance as well as increasing fears over the faith of Brexit.

The Canadian dollar had been gaining ground recently, as the nation’s strong economic data may have bolstered market expectations with regards to another BoC rate hike by the end of the year. On Friday, Canada’s jobs data are due to be released and expectations are for a decent report. Following the rise in the headline inflation rate for June and the acceleration in May’s GDP, encouraging job numbers could strengthen further the case for another BoC rate increase in the months to come.

GBP/CAD – Technical Outlook

GBP/CAD continues to trade below it medium-term downwards moving resistance line, taken from the peak of the 26th of March. Also, the pair remains below the short-term downside resistance line, drawn from the high of the 22nd of June. Overall, this makes us believe that there could still be more weakness to come in the longer-term. But before that happens, judging by yesterday’s spur to the upside, GBP/CAD could be setting itself up for a small correction to the upside.

If GBP/CAD breaks the 1.6925 hurdle, this could invite more bulls into the game and we could see the pair getting lifted to the next potential area of resistance at 1.7025, which acted as good support on the 1st and the 2nd of August. Further acceleration in the rate could put not only the 1.7100 barrier on our radar, but also the aforementioned short-term downside resistance line, which could hold down the rate.

The RSI has bottomed near its 25 zone and now moved towards the 50 line, and also points to the upside. The MACD also bottomed and moved above its trigger line. Even though it still below zero, it is showing determination in a potential move higher. Both indicators are somewhat supporting the case for some more correction to the upside, for now.

Now, if the rate does not correct further to the upside and the bears take charge near the 1.6925 barrier, we could see a strong reversal back down to the 1.6790 level, marked by yesterday’s low. A break below that level could open the door to the 1.6705 zone, which was the low of the 15th of November last year. If that zone is not able to withhold the rate from dropping further, then this could set the stage for a test of the 1.6585 level, marked near the lowest point of November 2017.

![]()

Kiwi Traders Lock Gaze on RBNZ

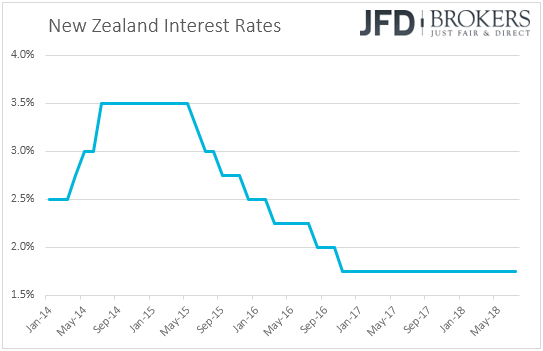

Tonight, during the early Asian morning, the RBNZ decides on monetary policy, but no change in interest rates is expected. At its previous meeting, the Bank kept interest rates unchanged at +1.75%, while the accompanying statement was slightly more dovish than the previous one. Governor Adrian Orr reiterated that interest rates could move in either direction, keeping the prospect of a rate cut on the table, while he appeared more concerned with regards to the global and domestic economic outlooks.

Since then, data showed that New Zealand’s inflation accelerated to 1.5% yoy in Q2 from 1.1%, which is in line with the Banks projections in its latest quarterly Monetary Policy Statement. The unemployment rate ticked up to 4.5% from 4.4%, its lowest since Q3 2009, while the net change in employment accelerated somewhat during the quarter. So, these in mind, we don’t expect any major changes in the Bank’s view. We expect the Bank to reiterate that interest rates could equally move up or down.

Alongside the policy decision, we will get the new quarterly Monetary Policy Statement, which includes the Bank’s updated economic projections, as well as a press conference by Governor Adrian Orr. Given the Bank’s concerns over the economic outlook, especially after the slowdown in Q1 GDP below its latest projections, we believe that officials may downgrade their growth forecasts in the new quarterly statement, which could weigh on the Kiwi.

The slide in the in the currency could intensify in the Bank also decides to push further back the timing of when it expects interest rates to start rising. According to the latest quarterly Report, rates are expected to start rising in September 2019. That said, although we see a decent chance for policymakers to revise down their growth forecasts, we see the case for a change in the rate-timing as less likely. The only major release that disappointed was the GDP data. We believe that inflation and employment figures were decent enough to convince officials keeping that timing unchanged.

NZD/USD – Technical Outlook

Since the beginning of July, NZD/USD continues to trade in a wide range between 0.6715 and 0.6855 levels. Recently the pair got closer to the lower side of that range but didn’t actually touch it. As we can see from the 4-hour chart, NZD/USD made a strong push back up during today’s Asian morning and is now testing a key resistance area, which could get broken, if the buying activity remains.

Given that NZD/USD showed some good strength this morning, we will stick to the upside, at least for until tonight’s RBNZ decision. Further acceleration of the rate above the 0.6755 zone could clear the path towards the 0.6810, marked by the high of the 1st of August. If that zone does not hold, then we could see NZD/USD traveling all the way towards the upper bound of the abovementioned range at the 0.6855 hurdle, which could potentially slow down the rise.

The RSI and MACD are somewhat in support of the upside scenario. The RSI bottomed and just managed to move above 50, which is a bullish indication. The MACD also is giving hope for the bulls, as it is above its trigger line and continues to move higher, despite being below its zero line.

Alternatively, a strong reversal back down to the 0.6715 barrier, could raise concerns over the possible upside scenario. This could be the case if the RBNZ maintains a dovish stance tonight and downgrades its growth projections. If the bears take control and drive NZD/USD below the lower bound of the range, this could open the way to the 0.6690 support area, marked by the low of the 2nd and 3rd of July. But if that area is not able to withhold the rate from falling, then we will start examining lower levels.

![]()

As for the Rest of Today’s Events

The calendar appears to be very light during the European and US sessions. The only indicators worth mentioning are Canada’s building permits for June and the Energy Information Administration (EIA) weekly crude oil inventories. Canada’s building permits are expected to have slowed to +1.0% from +4.7%, while inventories are expected to have declined 3.3mn barrels after rising 3.8mn the week before.

We also have one speaker on the agenda: Richmond Fed President Thomas Barkin.

As for tonight, besides the RBNZ decision, we get China’s CPI and PPI, both for July. The CPI rate is expected to have remained unchanged at +1.9% yoy, while the PPI is anticipated to have slowed to 4.6% yoy from 4.7%.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.