Following last week’s turmoil in the UK political scene, market participants are likely to keep their gaze locked on the Brexit front. On Sunday, an extraordinary EU summit is set to take place, but ahead of that, focus is likely to be on whether a no-confidence vote in PM May will be triggered. On Wednesday, the EU Commission will announce its decision on Italy’s resubmitted budget plan, with another rejection being the most likely outcome. The RBA and ECB minutes, as well as Japan’s and Canada’s CPIs for October are also due to be released.

Monday appears to be a relatively light day with no major economic releases on the economic calendar.

On Tuesday, during the Asian morning, the RBA releases the minutes of its latest meeting. At that meeting the Bank kept interest rates unchanged once again and proceeded with some positive changes in the accompanying statement. That said, the Aussie strengthened only 10 pips at the time of the release, a move suggesting that the changes were not significant enough for market participants to bring forth their expectations with regards to the RBA’s future plans. According to the Bank’s latest quarterly Statement on Monetary Policy, financial market prices imply that the cash rate is expected to increase in 2020. So, having all these in mind, we don’t expect the minutes to result in any fireworks.

During the European morning, in the UK, BoE Governor Mark Carney and several other MPC members will testify on the November Inflation Report before the Parliament’s Treasury Committee. At the conference following the November meeting, Carney said that the nature of the UK’s departure from the EU is not known and that the Bank’s response will not be automatic. It could be in either direction, the Governor said, signaling that rates could go up even in case of a no-deal Brexit. Following last week’s turmoil surrounding the Brexit landscape, it would be interesting to see whether he will stick to his guns.

As for the economic indicators, the UK CBI industrial trends orders for November are coming out, while from the US, we have building permits and housing starts, both for October.

On Wednesday, during the US session, we get durable goods orders for October. Expectations are for headline orders to have declined 2.5% mom after rising 0.7% in September, while core orders, which exclude to volatile items of transportation, are forecast to have accelerated to +0.4% mom from +0.1%. That said, such prints will drive both the headline and core yoy rates lower, something supported by the slide in the New Orders sub-index of the ISM manufacturing PMI for the month. Existing home sales for October, as well as the final UoM consumer sentiment index for November, are also due to be released.

On the political front, the EU Commission will announce its decision over Italy’s resubmitted budget plan. Last week, Italy submitted its plans, keeping the growth and deficit forecasts untouched, something that makes another rejection by the Commission the most likely outcome. The question now is whether the EU will indeed proceed with imposing sanctions to the nation.

On Thursday, during the Asian session, Japan’s national CPIs for October are coming out. The headline CPI is forecast to have risen to +1.4% yoy from +1.2%, while the core rate is anticipated to have held steady at +1.0% yoy. The forecasts are supported by the Tokyo CPIs for the month, where the headline CPI accelerated to +1.5% yoy from +1.3%, while the core Tokyo rate remained unchanged at +1.0% yoy.

That said, even if the headline national CPI accelerates somewhat, Japan’s inflation measures, and especially the ones of underlying inflation, would still be below the Bank’s objective of 2%, with the Bank’s own core CPI resting at just +0.5% yoy. This combined with the nation’s preliminary GDP data, which showed that the economy contracted 0.3% qoq in Q3, enhance our longstanding view that BoJ policymakers have a long way to go before they start considering a meaningful step towards normalization.

During the European morning, we get the minutes from the latest ECB policy gathering. At that gathering, the Bank kept its policy unchanged as was widely expected, reiterating, but not confirming, that asset purchases are likely to end in December. At the press conference, Draghi downplayed the softness in economic data, repeating that the risks surrounding Eurozone’s economic outlook remain broadly balanced. Thus, investors may be eager to find out whether other officials, besides Draghi, were also upbeat on the bloc’s economic outlook.

The rest of the day appears relatively empty, with the US markets closed due to the Thanksgiving Day.

On Friday, we get preliminary PMIs for November from several European nations and the Eurozone as a whole. Expectations are for the bloc’s manufacturing and services indices to have declined to 51.9 and 53.5, from 52.0 and 53.7 respectively, something that is likely to drag the composite PMI down for the fourth consecutive month. Specifically, the composite index is forecast to have declined to 53.0 from 53.1. Coming on top of the preliminary GDP data for Q3, which showed that the Euro area economy slowed to +0.2% qoq from +0.4%, another slide in the composite PMI could increase concerns that the loss in economic momentum dragged into the last quarter of the year as well. This was also acknowledged by ECB President Draghi last week. However, Draghi repeated once again that the overall risks to the growth outlook remain broadly balanced, suggesting that the ECB is unlikely to alter is policy plans any time soon.

We get preliminary Markit PMIs from the US as well. The manufacturing index is expected to have remained unchanged, while the services index is expected to have increase somewhat. This is likely to drive the composite PMI slightly higher. However, we repeat that the market tends to pay more attention to the ISM indices, due out on the 3rd and 5th of December.

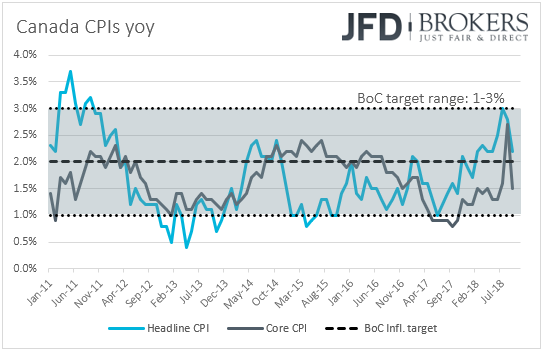

Later in the day, Canada’s CPIs for October are due to be released. Expectations are for Canada’s headline inflation rate to have remained unchanged at +2.2% yoy, while no forecast is currently available for the core rate. At its latest gathering, the BoC raised interest rates by 25bps and removed the part saying that officials will “take a gradual approach” with regards to future rate increases. Instead, they simply noted that “In determining the appropriate pace of rate increases, Governing Council will continue to take into account how the economy is adjusting to higher interest rates”. In our view, the removal of the “gradual approach” means that interest rates can now rise faster than previously anticipated if data suggest so. Thus, an upside surprise in the inflation prints may allow investors to increase bets that the next rate increase could come at the Bank’s 1st gathering for 2019. Canada’s retail sales for September are also scheduled to be released.

Finally, on Sunday, an extraordinary EU summit is set to take place in order to finalize and sign off the draft deal agreed by the UK and the EU over their divorce terms. However, ahead of the summit, focus is likely to be on whether Theresa May will be able to keep her position as UK Prime Minister. As we noted on Friday, for a leadership challenge to be triggered, 48 Conservative MPs have to submit letters of no confidence in May. According to a BBC report, at least 25 lawmakers said that they have submitted such letters, but bearing that MPs are not obligated to say openly whether they have done so, that number could be even higher. If the challenge is triggered, May would need to secure a simple majority of all Conservative MPs in order to stay in office. If she survives, we expect EU leaders to seal the deal on Sunday, but the big question would still be whether she can get the accord passed through the UK Parliament. With MPs from all sides opposing the draft agreed with the EU, we stick to our guns that this is likely to be a hard task.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.