Following the BoE and the ECB decisions last week, the G10 central bank torch is now passed to the BoJ, the Norges Bank and the SNB. Only the Norges Bank is expected to act and hike rates, while the other two are anticipated to stand pat. In terms of data, we get inflation figures from the UK, Canada and Japan, as well as New Zealand’s GDP for Q2.

On Monday and Tuesday, the calendar appears relatively light. On Monday, the only noteworthy releases we get are Eurozone’s final CPIs for August and the US Empire State manufacturing index for September. As usual, Eurozone’s final inflation prints are expected to confirm their preliminary estimates, while the Empire State index is expected to have declined slightly. On Tuesday, we get the minutes from the latest RBA meeting, where once again no fireworks are expected, and Canada’s manufacturing sales for July.

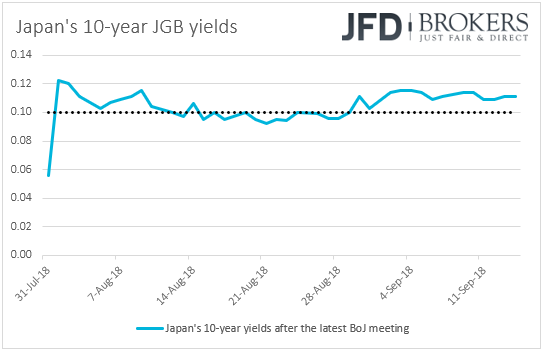

On Wednesday, the Bank of Japan concludes its two-day policy meeting. When they last met, back in July, Japanese policymakers kept their short-term policy rate unchanged at -0.1% and repeated that they will purchase Japanese government bonds (JGBs) so that 10-year yields will remain at around 0%. However, they announced some minor tweaks including more flexibility in bond operations, as well as the introduction of forward guidance for policy rates. What’s more, at the press conference following the decision, Governor Kuroda announced that the Bank will allow yields to fluctuate within a ±0.2% range.

Since then, Japan’s 10-year yields failed to move well above the 0.1% mark, and thus investors may be on the lookout for any clues whether the Bank could act again soon to boost trading. That said, with many officials attributing this to the summer-holiday season, we don’t expect any remarks on that front. We think that officials may prefer to wait for longer before evaluating the impact of their tweaks. What’s more, with all Japanese inflation metrics well below the Bank’s objective of 2%, we see it hard for policymakers proceeding with further changes so soon.

As for Wednesday’s economic indicators, during the Asian session, we get New Zealand’s current account data for Q2, and Japan’s trade balance for August.

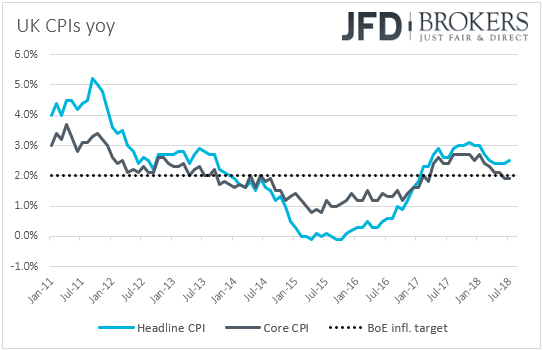

During the European morning, we get the UK CPIs for August. Expectations are for both the headline and core rates to have ticked down +2.4% yoy and +1.8% yoy, from +2.5% and +1.9% respectively. At last week’s policy meeting, the BoE kept rates unchanged at +0.75% and reiterated that an ongoing tightening of monetary policy over the forecast period would be appropriate, but any future rate increases are likely to be gradual and to a limited extend. In our view, the key takeaway from this decision is that the Bank’s plans remain more or less the same as in August. The Bank is probably done hiking for this year and according to UK OIS forward curve, the next rate increase is fully priced in for November 2019. Thus, even if inflation does not slow as the forecast suggest, we doubt that it would have a material impact on expectations over the next rate increase. We believe that market participants will keep paying more attention to Brexit developments and specifically an informal EU summit in Austria scheduled for Thursday and Friday.

Later in the day, the US building permits and housing starts, both for August, are coming out, as well as the nation’s current account balance for Q2.

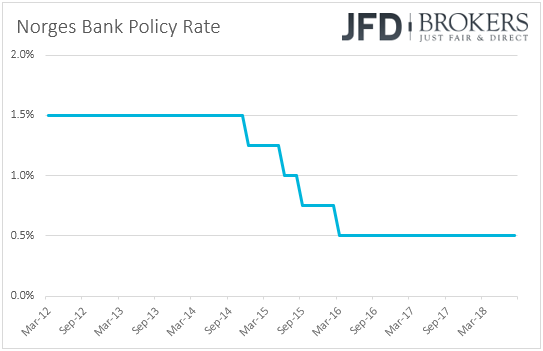

On Thursday, it is the turn of the Norges Bank to decide on interest rates. This will be one of the “bigger” meetings that are accompanied by the quarterly Monetary Policy Report. When they last met, Norwegian policymakers noted that the key policy rate would most likely be raised in September 2018, and this is what we expect them to do.

Latest inflation data showed that headline inflation accelerated to +3.4% yoy in August from +3.0% in July, well above the Bank’s estimate for the month, which is at +2.5% yoy, while the core rate rose to +1.9% yoy from +1.4%, which is also above the Bank’s forecast of +1.5% yoy for underlying inflation.The data support the case for a rate hike at this meeting and suggest that the Bank may maintain its hawkish stance. The headline inflation rate is well above the Bank’s target of 2.0%, while the core rate is now just a tick below that objective, which means that officials may remove from the statement the part saying that “underlying inflation was lower than the target” and perhaps note that it is now near the target. What’s more, in the quarterly monetary policy report, we see the case for the Bank to upgrade its inflation forecasts, and to revise up its projected rate path.

The SNB decides on interest rates as well, but this Bank is expected to keep borrowing costs unchanged at -0.75%. Latest CPI data showed that Switzerland’s inflation rate remained unchanged at +1.2% yoy in August, which is above the SNB’s inflation projections for Q3, but still distant of the Bank’s 2% objective. According to their latest projections, SNB policymakers expect inflation to exceed their target in Q1 2021, conditional upon interest rates staying at current levels over the entire forecast horizon. Thus, we don’t expect this meeting to paint a different picture than the previous one. Following the latest appreciation of the Swiss Franc, we expect officials to repeat that the franc remains highly valued, and to reiterate their readiness to intervene in the FX market if needed.

As for Thursday’s economic indicators, during the Asian morning, we get New Zealand’s GDP data for Q2. The forecast is for the qoq rate to have risen to +0.8% from +0.5%, but this could drive the yoy rate down to +2.5% from +2.7%. In any case, an acceleration to +0.8% in quarterly terms would be above the Bank’s latest estimate of +0.5% for the quarter and could ease some concerns with regards to a rate cut. At its August meeting, the Bank reiterated that the next move in interest rates could be up or down and pushed back the timing of when it expects rates to start rising, to September 2020 from 2019 previously.

From the UK, we have retail sales for August. Expectations are for headline sales to have declined 0.2% mom after rising 0.7% in July. This is likely to drag the yoy rate down to +2.3% from +3.5%. Core sales are also expected to have slid 0.2% mom, following a 0.9% rise, which could push the core yearly rate down to +2.4% from +3.7%. The case for a decline in the yearly rates is supported by the BRC retail sales monitor for the month, which also showed that retail sales slowed during the month on a yoy basis.

From the US, we get existing home sales for August, where expectations are for a rebound to +0.2% mom after a 0.7% slide in July.

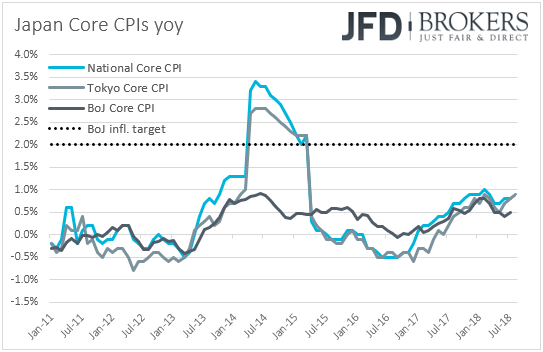

On Friday, during the Asian morning, we get Japan’s National CPI data for August. No forecast is currently available for the headline rate, while the core rate is anticipated to have ticked up to +0.9% yoy from +0.8%. Both the Tokyo headline and core rates for the month accelerated, suggesting that the National rates may have moved in a similar fashion. That said, even if inflation accelerates somewhat, it would still be distant from the BoJ’s inflation target. Even the latest print of the Bank’s own core CPI is at +0.5% yoy. Thus, we doubt that this data set will tempt policymakers to proceed with a meaningful normalization step in the near future.

During the European morning, we get the preliminary manufacturing and service-sector PMIs for September from several European nations and the Eurozone as a whole. Expectations are for the bloc’s manufacturing index to have declined to 54.4 from 54.6, while the services figure is anticipated to have remained unchanged at 54.4. This could drive the composite PMI down to 54.4 from 54.5.

We get preliminary PMI data for September from the US as well. Both the manufacturing and services PMIs are expected to have risen to 55.0, from 54.7 and 54.8 respectively.

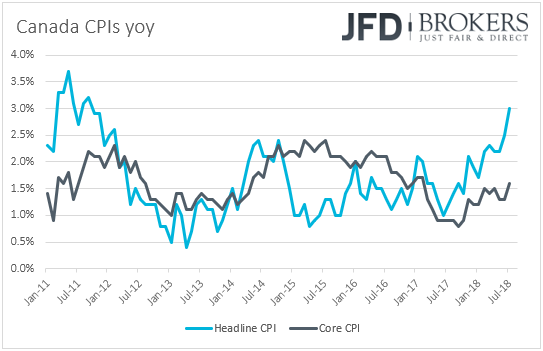

From Canada, we have the CPIs for August. Expectations are for the headline rate to have ticked down to +2.9% yoy after surging to +3.0% in July, while no forecast is available for the core rate. In our view, even if inflation slows somewhat, we don’t expect it to alter expectations with regards to an October rate increase by the BoC. After all, a tick down following the surge to +3.0% yoy in July from +2.5% appears more than normal to us. What’s more, at its latest meeting, the BoC remained willing to keep raising rates, while the following day, BoC Deputy Governor Carolyn Wilkins said that the Bank discussed dropping the “gradual approach” language on interest rates, and that they may raise rates even if NAFTA talks fall apart. The nation’s retail sales for July are also coming out. The forecasts suggest that both headline and core sales rebounded to +0.4% mom and +0.6% mom, after sliding 0.2% and 0.1% respectively.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.