Overnight, the main event was the BoJ decision. The Bank kept its monetary policy ultra-loose, but announced some minor tweaks including more flexibility in bond operation, as well as the introduction of forward guidance for policy rates. As for today, attention is likely to turn to Eurozone’s inflation and growth data, as well as the US core PCE index, the Fed’s favorite inflation measure.

Bank of Japan Keeps Policy Ultra-Loose; Announces Minor Tweaks

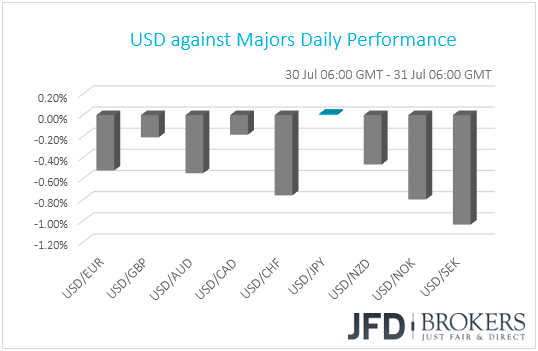

The dollar traded lower against all but one of the other G10 currencies on Monday. The only currency against which the greenback did not underperformed was JPY. USD/JPY traded virtually unchanged. The bigger winners against USD were SEK, NOK and CHF in that order.

The Swedish Krona came under massing buying interest yesterday after Sweden’s preliminary GDP data for Q2 beat estimates by a large margin. The Loonie, although it is found slightly higher against the dollar this morning, it tumbled overnight following reports that Canada’s request to take part in senior-level NAFTA talks later this week was rejected.

The yen has been also outperforming its US counterpart ahead of the BoJ policy decision but took a 180-degree turn as soon as we got the announcement. The Bank kept its short-term policy rate unchanged at -0.1% and repeated that it will purchase Japanese government bonds (JGBs) so that 10-year yields will remain at around 0%. However, it announced some minor tweaks including more flexibility in bond operation, as well as the introduction of forward guidance for policy rates. Officials also noted that the central bank will reduce the amount of bank reserves to which a negative interest rate is applied. According to the Bank, these adjustments aim at enhancing the sustainability of its “QQE with Yield Curve Control” policy and achieving the price stability target of 2% at the earliest possible time. At the same time, in its quarterly Outlook Report, it downgraded its inflation forecasts for this fiscal year, as well as 2019 and 2020.

The Japanese currency and Japan’s 10-year yields came under pressure as soon as the decision was published, perhaps as all this came as a disappointment to those expecting a concrete move towards normalization, a small increase in the long-term yield target for example. At the time of writing, Japan’s 10-year yields are almost 45% down. Remember that last week, a report noted that the Bank of Japan was discussing possible changes to its monetary policy, which raised speculation for such a move. Back then, we said that with all the Japanese inflation metrics well below the Bank’s 2% objective, it was unlikely for policymakers to proceed with a normalization step, in our view. Last week’s reports said that any changes would intend to make policy more sustainable, not tighter.

With the BoJ keeping its policy program ultra-loose, albeit more flexible, and with the Fed expected to continue raising rates, we maintain the view that USD/JPY could trade north in the foreseeable future. The risk to that view is any developments that could hurt the broader market sentiment. Due to its safe-haven status, the yen tends to get benefited in periods of turbulence and uncertainty.

USD/JPY – Technical Outlook

On a shorter-term picture, USD/JPY is stuck in a range between the 110.75 and 111.55 levels, where someone could say that the pair has not yet decided on its further direction. But, if we take a look at the upwards moving trendline, taken from the lows of the 29th of May, we can notice that USD/JPY got back above it quite quickly and the pair was not able to close below it over the past few days. This makes us believe that there could be a potential up-move building up.

For now, we remain somewhat positive over the near-term outlook, even though the pair is still within the short-term range. We could see USD/JPY traveling back up, towards the upper bound of the range at around 111.55 for a quick test. But if the pair is not going to stop there, a break of that level could open the path to the next potential area of resistance at around the 112.05 zone, marked by the inside swing low of the 19th of July. If the bulls remain in the driver’s seat, then further acceleration in the rate could lead to a test of the 112.65 hurdle, which acted as both resistance and support around mid-July.

Alternatively, if USD/JPY decides to move below the its upwards moving trendline, then this could open the way towards the lower side of the short-term range, which is sat at around the 110.75 level. For us to turn our view to a more negative one, we would need to see a clear break and a close below the lower bound of the range. This way, we could start examining lower support levels that might eventually get tested. The next potential area of support could be seen around the 110.30 mark, which acted as strong support on the 4th and the 5th of July. If a break of that line happens, the pair could make its way towards the 109.70 hurdle, or even the 109.35 level, marked by the low of the 25th of June.

Eurozone CPI and GDP Data, As Well As US core PCE on Today’s Agenda

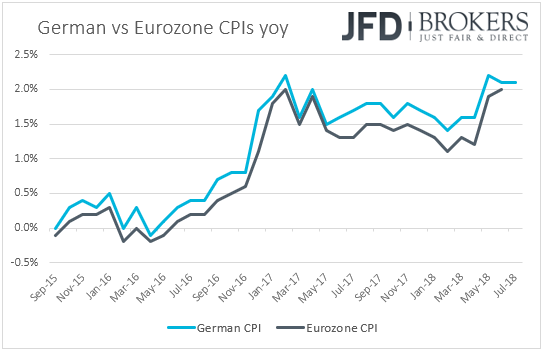

Today, during the European session, we get Eurozone’s preliminary inflation data for July and the bloc’s first estimate of the Q2 GDP. The forecast is for the headline CPI rate to have remained unchanged at +2.0% yoy, while the core rate is anticipated to have ticked up to +1.0% yoy from +0.9% yoy. Germany’s inflation rate for the month held steady yesterday, supporting the forecast of Eurozone’s headline print. As for first estimate of Q2 GDP, it is expected to show that the euro area economy grew 0.4% qoq, the same pace as in Q1.

At the press conference following last week’s ECB meeting, President Draghi maintained the view that the risks surrounding the Eurozone’s economic outlook remain broadly balanced and noted that market expectations on interest rates are well aligned with the anticipation of the Governing Council. Thus, if the forecasts of the aforementioned data are met, we see it unlikely for investors to change their expectations around the Bank’s future plans.

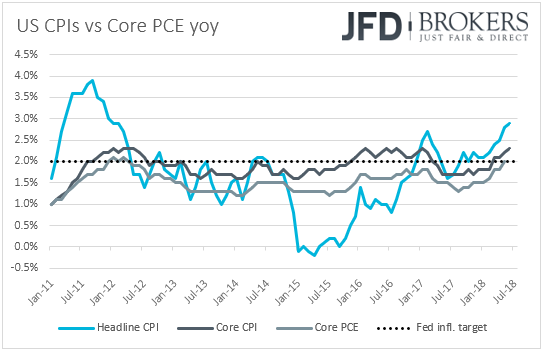

Later in the US, we have personal income and spending data for June, as well as the core PCE index for the month. Personal income is anticipated to have risen 0.4% mom, the same pace as in May. Spending is also expected to rise 0.4%, but this would be an acceleration from the previous monthly rate of +0.2%. That said, the slowdowns in the monthly earnings and retail sales prints for the month suggest that the risks surrounding both the income and spending forecasts are tilted to the downside.

As for the yoy core PCE rate, the Fed’s favorite inflation measure, it is expected to have remained unchanged at +2.0% yoy. However, bearing in mind that the core CPI accelerated during the month, we see the case for the core PCE index to have moved in a similar fashion. Just a day ahead of the FOMC decision, an acceleration of this inflation metric above the Fed’s 2% objective could increase bets that Fed officials will maintain an upbeat tone in the statement accompanying the decision, keeping the door open for two more rate increases until the end of the year.

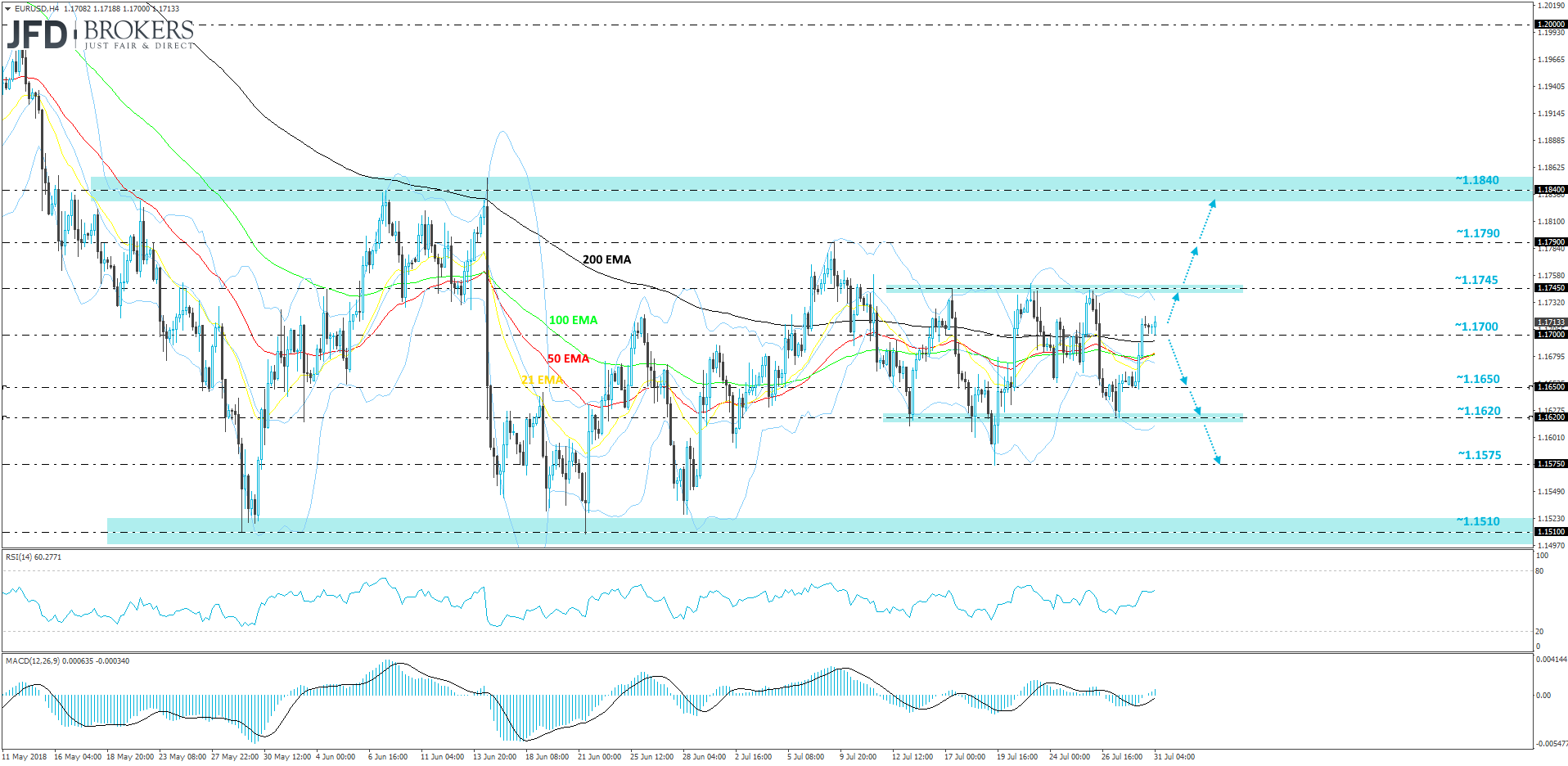

EUR/USD – Technical Outlook

Overall, EUR/USD is still within a wide range between the 1.1510 and 1.1840 levels and until it gets out of it, it would be difficult to speculate over the slightly longer-term outlook. From the short-term perspective, the pair is trying hard to make its way higher, but stays within another, shorter-term range, between 1.1620 and 1.1745.

On the upside, the pair could continue trading north for a while more, as the 1.1700 support level held the rate from falling yesterday and during the early European morning today, it acted as a bouncing ground. The next potential stop could be the 1.1745 barrier, which held the rate from moving higher a few times in the end of July. If this time the break of that barrier happens, we could see the pair traveling towards the 1.1790 level, marked by the highest point of July. But if that doesn’t stop it, then a test of the upper bound of the longer-term range could be possible.

On the downside, if EUR/USD drops below the 1.1700 line, this could interest the bears to pull the pair towards the next potential area of support at around 1.1650, or even slightly lower to the 1.1620 zone, which held the rate from dropping lower on the 27th of July. If the pair continues falling, then keep an eye on the 1.1575 mark that acted as strong support on the 19th of July.

As for the Rest of Today’s Events

From Canada, we get the monthly GDP print for May. The forecast is for the monthly rate to have risen to +0.3% mom from +0.1%, but this would drive the yoy rate down to +2.3% from +2.5%.

As for tonight, during the Asian morning Wednesday, we get New Zealand’s employment data for Q2. Expectations are for the unemployment rate to have remained unchanged at 4.4%, while the net change in employment is expected to have slowed to +0.4% qoq from +0.6% in Q1. In China, the Caixin manufacturing PMI for July is forecast to have ticked down to 50.9 from 51.0.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

FX and CFDs are leveraged products. They are not suitable for every investor, as they carry high risk of losing your capital. You should be aware of all the risks associated with trading on margin. Please read the full Risk Disclosure.