Following last week's ECB, BoC, Riksbank and Norges Bank policy decisions, this week, the central bank torch will be passed to the BoJ and the BoE. As for the rest of the events, UK Chancellor Philip Hammond will deliver the Autumn budget to the Parliament on Monday, while on Wednesday, we have Eurozone’s preliminary CPIs for October. On Friday, the spotlight is likely to fall on the US employment data.

On Monday, UK Chancellor of the Exchequer Philip Hammond will deliver the Autumn budget to the Parliament. Hammond has been under pressure from PM Theresa May to end a decade of austerity, but despite a shrinking fiscal deficit, we doubt that such a decision will be taken before the official Brexit date. After all, May said that the government could consider any actions after the UK’s departure from the EU, and that the matter would be reviewed in next year’s Spring Statement. On Sunday, the Chancellor said that it would be hard for the Treasury to please the Prime Minister in case of a no-deal Brexit and thus, even if his speech includes hope and optimism on the matter, everything is likely to be conditioned upon of a smooth EU-UK divorce.

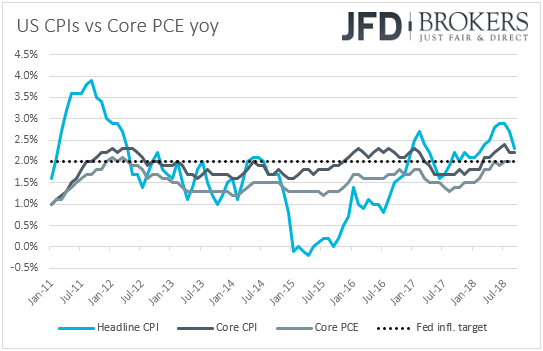

From the US, we get personal income and spending data for September, as well as the yearly core PCE rate for the month. Income is expected to have risen 0.3% mom, the same pace as in August, while spending is anticipated to have accelerated to +0.4% mom from +0.3%. The income forecast is supported by the monthly earnings rate for the month, which remained unchanged at 0.3%, while the steady 0.1% growth of retail sales suggests that the risks surrounding the spending forecast may be tilted somewhat to the downside, perhaps for an unchanged rate as well.

As for the yoy core PCE rate, the Fed’s favorite inflation metric, it is expected to have stayed at +2.0%, something supported by the core CPI rate for the month, which remained unchanged as well. The key takeaway we got from the latest FOMC meeting, as well as by the minutes of that gathering, is that Fed officials are willing to continue raising rates mainly guided by economic data, instead of how close to their neutral level interest rates are. What’s more, a number of policymakers believe that it would be necessary to raise rates above neutral for some time. Therefore, an unchanged core PCE rate could keep the Fed on track for more rate increases, with the next one most likely to come in December.

On Tuesday, in Asia, we get Japan’s unemployment rate for September, which is expected to have remained unchanged at 2.4%, and Australia’s building approvals for the same month, which are forecast to have risen 3.9% mom, after falling 9.4% in August.

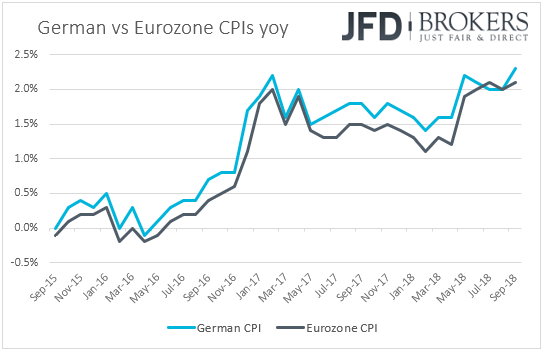

From Germany, we get the preliminary CPI for October, one day ahead of Eurozone’s preliminary inflation prints for the month. Expectations are for both the CPI and HICP rates to have risen to +2.4% yoy, from +2.3% and +2.2% respectively. Something like that could raise speculation that the bloc’s headline CPI rate may rise as well. Germany’s unemployment rate is also coming out and is expected to have remained unchanged at 5.1%.

From the Eurozone as a whole, we get the 1st estimate of the bloc’s GDP for Q3, and expectations are for the Euro area economy to have grown 0.4% qoq once again, the same pace as in the previous two quarters. That said, this could drive the yoy rate lower as the qoq rate of Q3 2017 that will drop out of the yearly calculation was 0.6%.

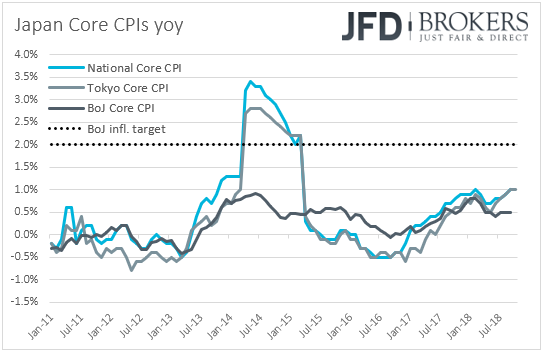

On Wednesday, during the Asian session, the BoJ concludes its two-day monetary policy gathering. The latest meeting passed unnoticed with the Bank keeping is policy framework unchanged via a 7-2 vote and maintaining the view that Japan’s economy is expanding moderately. What’s more, officials reiterated that they intend to maintain the current extremely low levels in interest rates for an extended period of time.

Latest inflation data showed that the nation’s headline CPI rate ticked down to +1.2% yoy from +1.3%, while the core print rose to +1.0% yoy from +0.9%. That said, the BoJ’s own core CPI metric stood unchanged at +0.5% yoy. Therefore, with all inflation metrics well below the Bank’s objective of 2%, we see it hard for policymakers proceeding with further policy changes after the tweaks announced in July.

From Australia, we get inflation data for Q3. The headline CPI rate is forecast to have slid to +1.9% yoy from +2.1% in Q2, while the trimmed mean rate is forecast to have remained untouched at +1.9% yoy. Both rates are expected to be above the RBA’s latest forecasts for the second half of the year, but below the lower end of the 2-3% inflation target range. Thus, we see it hard for investors to alter their view around the RBA’s policy plans. According to the Bank’s latest quarterly Statement on Monetary Policy, the cash rate is expected to increase around the end of next year.

During the European day, we get Eurozone’s preliminary CPI data for October. Expectations are for the headline rate to have remained unchanged at +2.1% yoy, while the core rate is anticipated to have ticked back up to +1.0% yoy from +0.9%. That said, given that Germany’s headline inflation is anticipated to have accelerated during the month, we see the risks surrounding Eurozone’s headline print as tilted to the upside. Following last week’s ECB meeting, where President Draghi maintained his fairly optimistic stance with regards to Euro area’s economic and inflation outlooks, accelerating inflation, combined with a GDP print suggesting that the economy did not slowed in Q3, may calm somewhat investors’ fears over the bloc’s economic performance. Eurozone’s unemployment rate for September is also coming out and is anticipated to have remained unchanged at 8.1%.

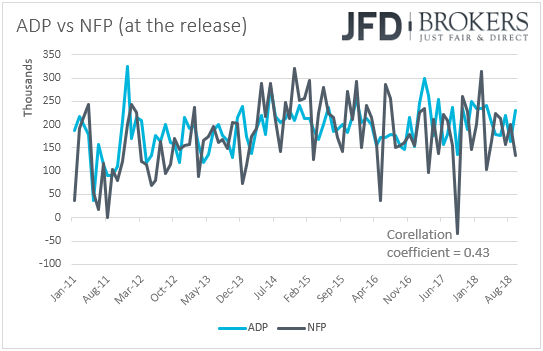

In the US, we have the ADP employment report for October. Expectations are for the private sector to have gained 190k jobs, less than the 230k in September, which could raise speculation that the NFP number, due out on Friday, could come near its forecast, which is 191k. That said, we repeat to the umpteenth time that, even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are taken into account) has been very low in recent years. Even last month, the ADP print rose to 230k, but the NFP number dropped to 134k.

From Canada, we have the monthly GDP for August, but no forecast is currently available.

On Thursday, the central bank torch will be passed to the Bank of England. Actually, it will be a “Super Thursday” for the Bank, as besides the rate decision and the meeting minutes, it also releases its quarterly Inflation Report, which will be presented by Governor Mark Carney at a press conference after the decision.

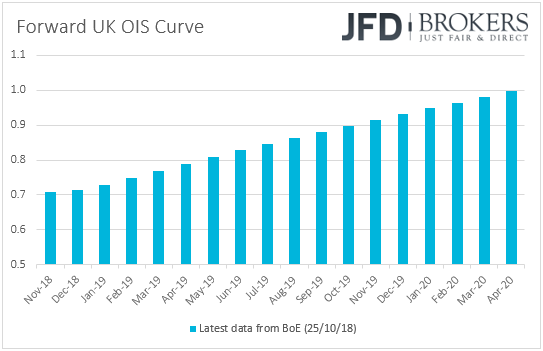

The Bank is widely anticipated to keep policy steady via a 9-0 vote, so if this is the case, market participants will quickly turn their attention to the minutes, the economic projections and Carney’s conference. When they last met, officials proceed with no surprises, keeping rates unchanged at +0.75%. The key takeaway since the August decision has been that the Bank is probably done hiking for this year, and according to the UK OIS forward curve, the next rate increase is now fully priced in for April 2020. Back in August, Governor Carney said that a hike per year for the next few years is a good rule of thumb, but with the caveat that it will depend on what happens with Brexit. Therefore, investors’ pessimistic pricing for the next hike may reflect their increasing concerns over the matter.

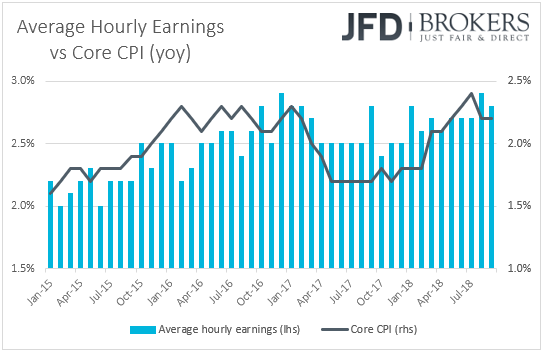

Latest data showed that wages accelerated in September, but inflation slowed in both headline and core terms, suggesting little urgency for any rate increase in the months to come, especially with five months to go before the official date of the UK’s departure from the EU. Thus, we expect officials to reiterate that further rate increases are likely to be gradual and to a limited extend, and we see no reason for a hawkish spin by Governor Carney at the press conference. The UK manufacturing PMI for October is also due to be released and expectations suggest a slide to 53.1 from 53.8. That said, we expect the release to be overshadowed by the BoE policy decision.

From the US, we get the final Markit manufacturing PMI for October, as well as the ISM manufacturing index for the month. The final Markit print is expected to confirm its preliminary estimate of 55.9, while the ISM index is anticipated to have declined to 59.0 from 59.8.

Finally, on Friday, the spotlight is likely to fall on the US employment report for October. Expectations are for non-farm payrolls to have increased 191k, after rising 134k in September. The unemployment rate is forecast to have stayed unchanged at 3.7%, its lowest since 1969, while average hourly earnings are expected to have slowed to +0.2% mom from +0.3%. Nevertheless, this could drive the yoy rate up to +3.1% from +2.8%.

Overall, the forecasts point to further tightening of the labor market, and barring any major deviations from the NFP forecast, we believe that most of the attention is likely to fall once again on wage growth. Accelerating earnings on a yearly basis could mean accelerating inflation in the months to come. Therefore, combined with a decent PCE print on Monday, this report could strengthen further the case for more hikes by the Fed. According to the Fed Funds, the market assigns a 70% to a December hike, and anticipates nearly two more for 2019, at a time when Fed officials expect three. This suggests that there is room for market participants to bring their estimates closer to the Fed’s if data continue to come on the positive side.

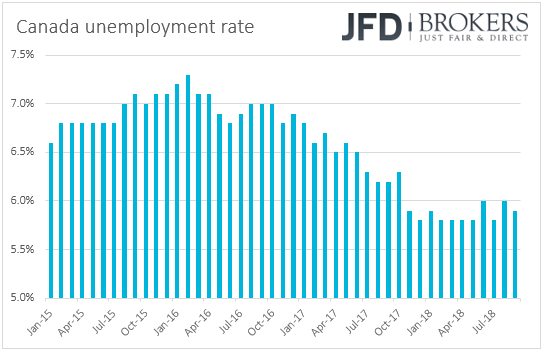

We get employment data for October from Canada as well. The forecasts suggest that the unemployment rate remained unchanged at 5.9% with the economy gaining 10k more jobs after the stellar 63.3k gain in August. At its policy meeting last week, the BoC raised rates by 25bps to +1.75% and removed the part saying that officials will “take a gradual approach” with regards to future rate increases. Instead, they simply noted that “In determining the appropriate pace of rate increases, Governing Council will continue to take into account how the economy is adjusting to higher interest rates”. Therefore, a decent employment report combined with a decent GDP number on Wednesday could keep bets for further and faster rate increases elevated.

As for the rest of Friday’s events, during the Asian morning, we get Australia’s PPI for Q3 and the nation’s retail sales for both September and Q3. The PPI is expected to have slowed somewhat on a qoq basis, to +0.2% from 0.3%, while retail sales are anticipated to have increased +0.3% mom in September, the same pace as in August. This could drive the qoq rate down to +0.4% from +1.2%. In Europe, we get the final manufacturing PMIs from several European nations and the Eurozone as a whole. As usual, the bloc’s final print is expected to confirm its preliminary estimate, which showed a slide to 52.1 from 53.2. In the UK, the construction PMI for October is anticipated to have ticked down to 52.0 from 52.1. From the US, besides the employment data, we get factory orders and trade data, both for September. We get trade data for September from Canada as well.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.