This week, we have two major central banks deciding on interest rates: the BoE and the ECB. Both Banks are expected to keep their policies unchanged, while no major changes in their language is expected either. In emerging markets, the Turkish central bank meeting is likely to gather extra attention. We also get the UK employment data for July and the US CPIs for August.

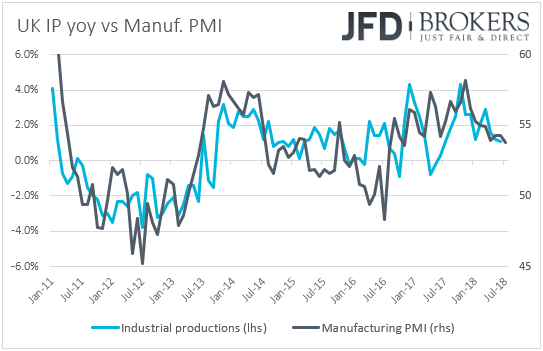

On Monday, we get the UK industrial and manufacturing production data for July. Expectations are for both the industrial and manufacturing production monthly rates to have declined to +0.2% mom from +0.4%. This could keep the yoy rates unchanged at +1.1% and +1.5% respectively. That said, bearing in mind that the manufacturing PMI for July declined to 53.8 from 554.3, we view the risks surrounding the yearly rates as somewhat tilted to the downside. The UK monthly GDP for July, as well as the trade balance for the same month are also coming out. The GDP data are expected to show that the economy accelerated somewhat, to +0.2% mom from 0.1%, while the nation’s trade deficit is anticipated to have slightly widened.

On Tuesday, during the European day, the German ZEW survey for September is coming out. The forecast is for the current conditions index to have declined to 72.0 from 72.6, while the expectations one is anticipated to have risen somewhat, but to have remained within the negative territory. Specifically, the expectations index is forecast to have increased to -13.4 from -13.7.

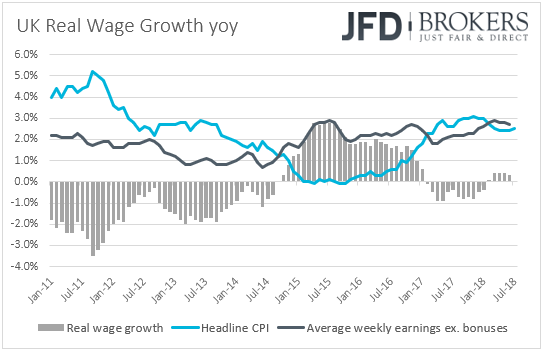

In the UK, we get employment data for July. Expectations are for the unemployment rate to have remained unchanged at its 43-year low of 4.0%, while average weekly earnings including bonuses are anticipated to have accelerated to +2.5% yoy from +2.4% in June. That said, the excluding-bonuses earnings rate is anticipated to have remained unchanged at +2.7% yoy.

According to the HIS Markit/REC Report on Jobs for the month, low candidate availability and strong demand for employees led to a further steep increase in starting salaries, while temporary pay accelerated close to April’s two-year record. In our view, this supports the case for accelerating earnings including bonuses, and suggests that the ex-bonuses wage growth rate may have risen as well.

Later in the day, we have the US JOLTs job openings for July and Canada’s housing starts for August.

On Wednesday, Eurozone’s employment change for Q2 and the bloc’s industrial production data for July are coming out. No forecast is available for the employment change, while industrial production is anticipated to have fallen 0.5% mom after a 0.7% slide in June.

From the US, we get the PPIs for August. Expectations are for the headline rate to have ticked down to +3.2% yoy from +3.3% in July, while the core rate is anticipated to have risen to +2.8% yoy from +2.7%.

On Thursday, during the Asian morning, Australia’s employment data for August are coming out. Expectations are for the unemployment rate to have held steady at 5.3%, while the net change in employment is forecast to show that the economy added 18.4k jobs after a 3.9k decline in July.

During the European day, we have two major central banks deciding on interest rates: The BoE and the ECB. From the emerging markets, the Turkish central bank meeting is likely to attract special attention.

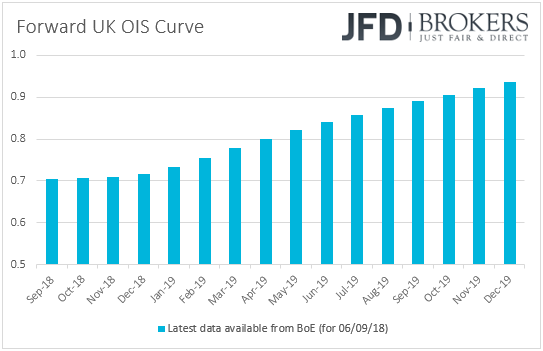

Getting the ball rolling with the Bank of England, expectations are for policymakers to keep interest rates unchanged at +0.75%. When they last met, they decided to raise rates by 25bps via a unanimous vote, but Governor Carney’s comments at the press conference, as well as in an interview after the conference, suggested that the BoE is probably done hiking for this year.

So, having this in mind, and also taking into account that this is one of the “smaller” meetings that are not accompanied by a press conference and updated economic projections, we doubt that we will get any messages that could alter expectations around the Bank’s future plans. We expect the Bank to reiterate that an ongoing tightening of monetary policy over the forecast period would be appropriate, but any future rate increases are likely to be at a gradual pace and to a limited extent. According to the latest data available from the BoE for the forward OIS curve, the next rate increase is not even fully priced in for the end of 2019.

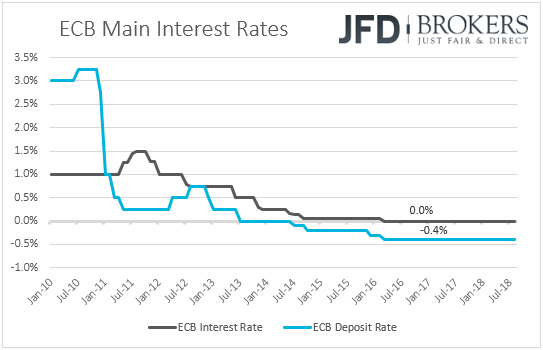

Passing the ball to the ECB, no change in policy is expected from this Bank either. We believe that officials will just confirm that after September, asset purchases will be reduced to EUR 15bn per month until the end of December, and they will repeat that interest rates are likely to stay at present levels “at least through the summer of 2019”.

Since the July policy meeting, Eurozone’s economic data showed that headline inflation ticked up to 2.1% yoy in July, but retreated back to 2.0% in August, while the core rate rose to +1.1% yoy in July from +0.9% in June and ticked down to +1.0% in August. Final GDP data confirmed that Eurozone’s economy grew 0.4% qoq in Q2, the same pace as in Q1, while the composite PMI for August rose to 54.5 from 54.3 in July. The data suggests that the bloc’s economic picture has not changed since the last meeting and that’s why we don’t expect this gathering to result in any surprises, and just the confirmation or the reduction in asset purchases. We will also get the Bank’s updated economic projections.

Now, let’s move to the emerging markets and the Turkish central bank meeting. The lira has been hit hard last month following the US-Turkey standoff over the imprisonment of an American pastor, as well as due to concerns about President Erdogan’s influence over monetary policy. Last week, Turkey’s Finance Minister said that the Bank is independent of government, while the Bank itself noted in a statement that it would adjust its monetary policy stance at this meeting in order to support price stability. The statement came after data showed that Turkish inflation surged to 17.9 in August from 15.85 in July. Therefore, investors will be on the lookout to see whether the Bank will indeed hike rates this time, and by how much.

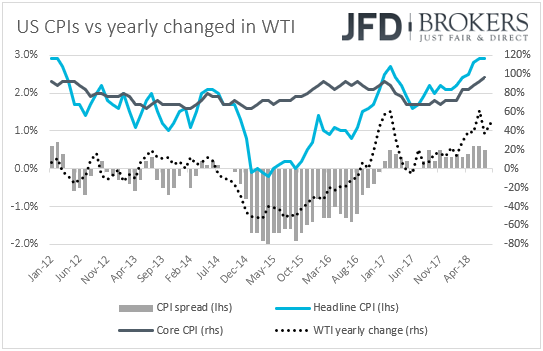

From the US, we get CPI data for August. Expectations are for the headline rate to have ticked down to +2.8% yoy from +2.9% in July, while the core rate is anticipated to have remained unchanged at +2.4% yoy. Taking into account the forecasts of the PPIs, they support the case for a tick down in the headline rate, but they also suggest that the core rate may have risen somewhat. Having said that though, if the core CPI rate was to move up, bearing in mind that the yearly change rate of WTI rose during the month, we would consider the risks of the headline rate to be tilted to the upside as well.

Although the Fed drives the monetary policy wheel based on the PCE inflation metrics, accelerating CPIs may increase the likelihood for the PCEs to follow suit and thereby, bolster further expectations that the Fed may end the year with a total of 4 rate hikes. According to the Fed fund futures, the market is almost certain that the Committee will push the hiking button at its upcoming gathering, while there is a 75% chance for another one to come in December.

Finally, on Friday, we get Sweden’s inflation data for August. Both the CPI and CPIF rates are expected to have remained unchanged at +2.1% yoy and +2.2% yoy respectively. However, once again we will focus on the core CPIF inflation metric, which excludes energy. At last week’s meeting, the Riksbank kept interest rates on hold and that it could delay raising them. Previously, the Bank has been advocating for slow repo-rate increases to start towards the end of the year, while now, it noted that rates will be held unchanged in October, and then raised either in December or February.

Thus, having that in mind, we believe that another slowdown in the core CPIF print could raise speculation that in October, policymakers may dismiss the December option and note that rates could be raised at the beginning of next year. That said, the October policy meeting is scheduled for the 23rd of the month, and up until then we have one more inflation data set, which comes out on the 11th. Thus, we prefer to wait for that release as well before we better assess how and whether the world’s oldest central bank could alter its communication.

In the US, we get retail sales and industrial production data for August. Starting with retail sales, expectations are for both headline and core sales to have slowed somewhat, to +0.4% mom and +0.5% mom, from +0.5% and 0.6% respectively. As for industrial production, it is anticipated to have accelerated to +0.3% from +0.1%. The preliminary UoM consumer sentiment index is also coming out, alongside the 1- and 5-year UoM inflation expectations.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.