Today, all lights are likely to fall to monetary policy decisions by two major central banks: The BoE and the ECB. The former is expected to hike rates for the second time since the outbreak of the coronavirus, while the latter is widely anticipated to stand pat. However, we will closely monitor the outcome for clues and hints on its future course of action.

Investors Lock their Gaze on BoE and ECB Meeting Outcomes

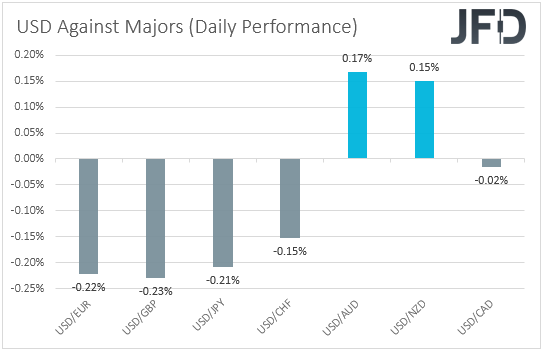

The US dollar continued trading lower against most of the other major currencies on Wednesday and during the Asian session Thursday. It gained ground only against AUD and NZD, while it was found virtually unchanged against CAD. The greenback lost the most ground versus GBP and EUR, the central banks of which decide on monetary policy today.

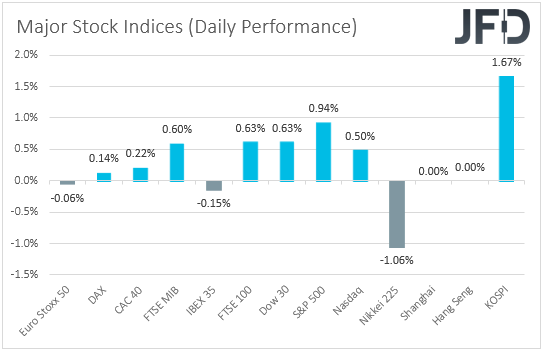

The weakening of the US dollar suggests that market participants may have continued to buy stocks, but the relative strength of the yen and the franc, and the weakening of the risk-linked Aussie and Kiwi point otherwise. Therefore, in order to clear things up, we prefer to turn our gaze to the equity world. There, most major EU and US indices traded in the green, with a only couple finishing virtually unchanged. However, today in Asia, Nikkei slid 1.06%, while, on its first trading session for the week, KOSPI jumped 1.67%, perhaps to catch up with the recovery seen in other indices the last few days.

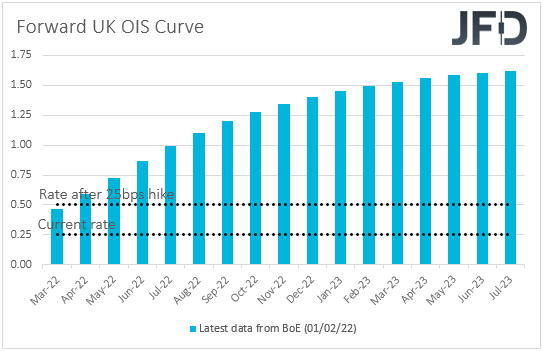

Now, today, as we already noted, we have two major central banks deciding on monetary policy, and those are the BoE and the ECB. First, we have the BoE, which, at its latest gathering, decided to push the hike button for the first time since the outbreak of the coronavirus, lifting interest rates to 0.25% from 0.10%, and adding that more modest tightening is underway. Recent UK data have been relatively supportive, with the unemployment rate declining further in November, the CPIs accelerating more than anticipated in December, and the preliminary PMIs revealing further economic expansion during the month of January, despite at a slower pace than in December.

Thus, we do see the case for a quarter-point increase at this gathering, and, actually, this is not only our own view, but the market consensus as well. According to the UK OIS (Overnight Index Swaps) forward yield curve, investors are fully pricing in such an action, while they see the case for nearly four more hikes by the end of the year. Thus, a 25bps hike by itself is unlikely to prove a major market mover. Market attention is likely to fall to clues and hints on how fast policymakers are planning to proceed with upcoming lift-offs. What’s more, remember that 0.5% is the level the Bank placed as a threshold for beginning to shrink its balance sheet. Therefore, we will look for references on that front as well, as well as on the updated economic projections. Let’s not forget that this will be a Super Thursday for the BoE. Anything suggesting an aggressive rate path, and a balance-sheet reduction, could support the British pound, which due to monetary policy divergencies could keep outperforming currencies like the Aussie and the euro.

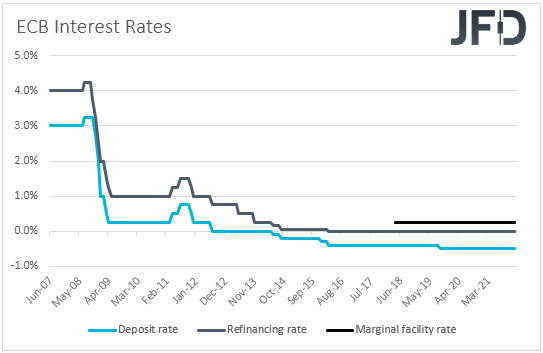

Soon after the BoE, we have the ECB deciding on monetary policy, but no action is expected from this Bank. Despite market participants pricing in a small rate increase by the end of this year, the Governing Council has been holding the view that something like that is unlikely. ECB President Christine Lagarde expressed that view several times in the past, while a couple of weeks ago, she said that inflation in the Eurozone will decrease gradually over the course of the year and that the ECB does not need to act as boldly as the Fed, due to a different economic situation. That said, with both Eurozone’s inflation rates coming in higher than expected, it would be interesting to see whether Lagarde and her colleagues will repeat the view that interest rates are unlikely to be lifted this year. Due to the slowdown in economic activity for Q4, we believe that there is a decent chance for such an outcome, something that could come as a disappointment to those expecting a small lift-off, and thus, the euro may come under renewed selling interest.

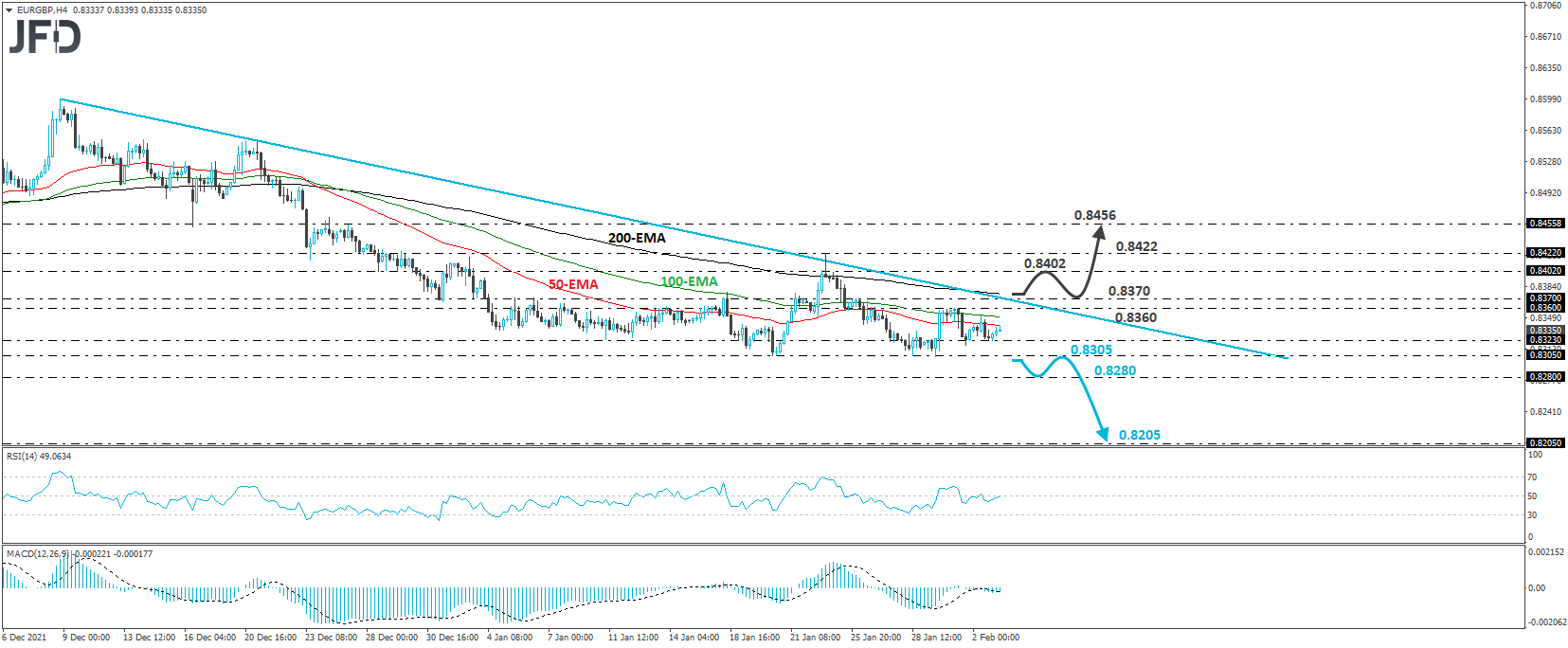

EUR/GBP – Technical Outlook

EUR/GBP traded in a consolidative manner yesterday, staying slightly above the 0.8323 barrier. However, overall, the pair is trading below the downside resistance line drawn from the high of December 8th, and thus, we would consider the short-term outlook to still be negative.

A break below the key barrier of 0.8305, which has been providing support since January 20th, would confirm a forthcoming lower low on the daily chart and may initially target the 0.8280 zone, marked by the low of February 18th. If the bears are not willing to stop there, then, the rate will enter territories last seen back in 2016, and the next territory to consider as a support may be the low of June 29th of that year, at around 0.8205.

On the upside, we would like to see a clear break above 0.8370, the high of January 26th, before we start examining a bullish reversal. This could confirm the break above the aforementioned downside line and may pave the way towards the 0.8402 level, or the 0.8422 barrier, marked by the highs of January 25th and 24th respectively. If neither hurdle is able to stop the bulls, then, a break higher could see scope for advances towards the peak of December 27th, at 0.8456.

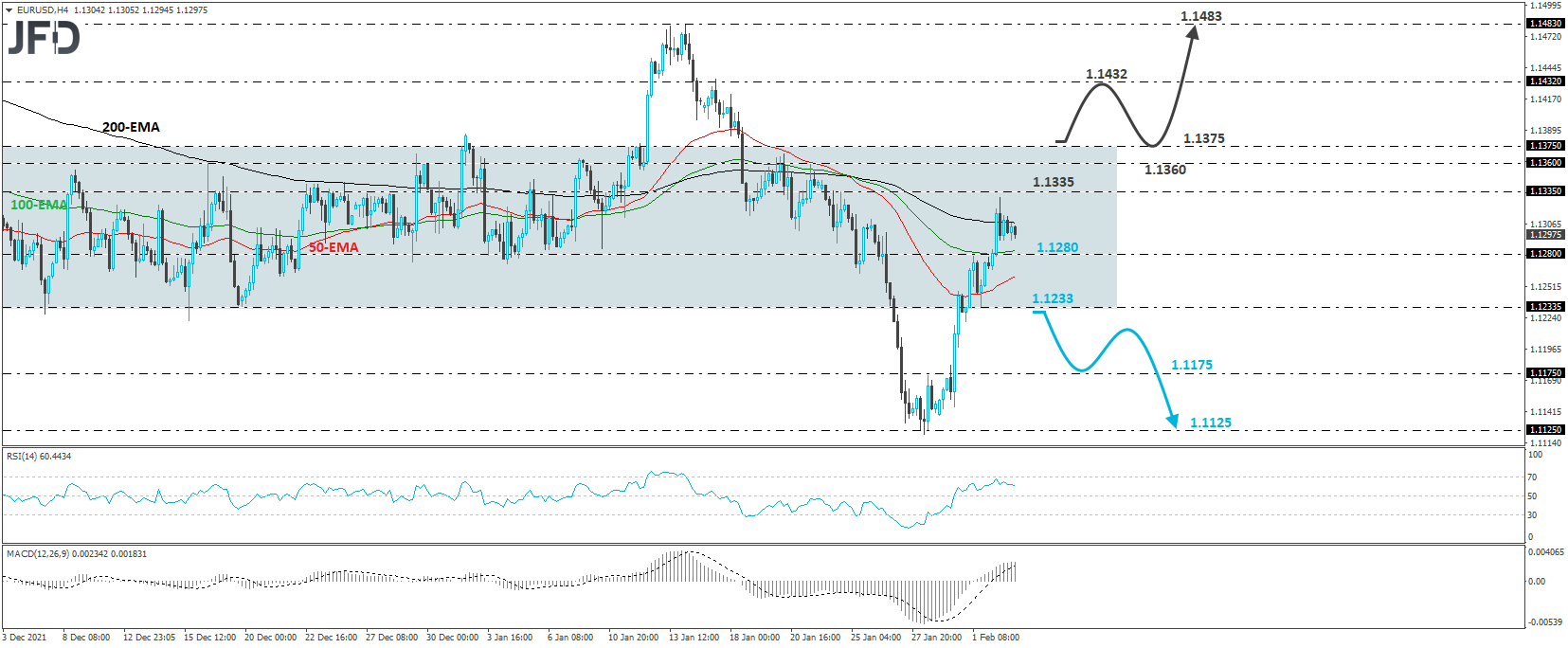

EUR/USD – Technical Outlook

EUR/USD recovered strongly lately, entering back into the sideways range that had been containing most of the price action between November 26th and January 26th. In our view, this has turned the short-term outlook back to neutral, and even if we see a slide triggered by the ECB outcome, we would like to see a clear dip back below 1.1234 before we start examining the bearish case again.

If, indeed, we doo see that break soon, we believe that the bears will get encouraged to push the action down to the inside swing high of January 28th, at 1.1175, the break of which could carry extensions towards the low of the same day, at around 1.1125, or even the rounder figure of 1.1100.

In our view, the outlook could turn to bullish upon a break above the upper bound of the range, at around 1.1375. This could initially result in advances towards the peak of January 17th, at 1.1432, the break of which could extend the gains towards the peak of January 14ht, at 1.1483.

As for the Rest of Today’s Events

We have the final Markit services and composite PMIs for January from the Eurozone, the UK, and the US, as well as the ISM non-manufacturing index for the month. As it is usually the case, the final Markit prints are expected to confirm their initial forecasts, while the ISM index is anticipated to have declined somewhat, to 59.3 from 62.3. As every Thursday, we also get the US initial jobless claims for the prior week.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68.02% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2022 JFD Group Ltd.