Central banks are back on the economic agenda this week, with the BoC the BoJ and the Riksbank holding their monetary policy meetings. None of the three Banks is expected to proceed with any policy changes and thus, investors will be looking for hints with regards to their future plans. As far as data releases are concerned, Australia’s inflation figures for Q1 are coming out, as well as the 1st estimated of the US GDP for the same quarter.

Monday is Easter Monday for most of the G10 nations and thus, most markets will be closed. Bourses are open only in China, Japan, Canada and the US. With regards to data, we only get the US existing home sales for March, which are expected to have declined 2.3% mom after rising 11.8% in February.

On Tuesday, the calendar is very light as well. The only release worth mentioning is the US new home sales for March and the forecast suggests that they declined 5.6% mom after a 4.9% increase in February.

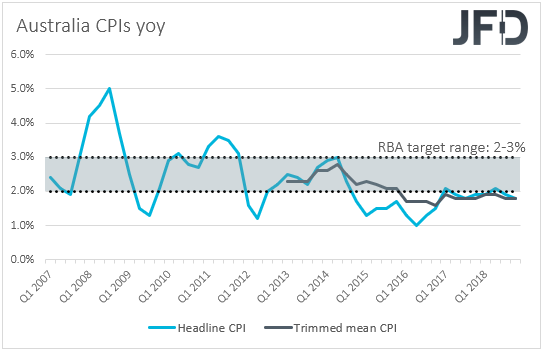

On Wednesday, during the Asian morning, Australia’s CPIs for Q1 are due to be released. The forecast is for headline inflation to have slowed to +1.5% yoy from +1.8% in Q4 2018, while the trimmed mean yoy rate is anticipated to have ticked down to +1.7% yoy from +1.8%. Both rates would still be below the lower end of the RBA’s 2-3% inflation target range, but they will be near its own projections for the first half of 2019, which are +1.4% for the headline CPI and 1.8% for the trimmed mean rate.

The statement from the latest RBA meeting had a softer tone than previously, with officials refraining from repeating that unchanged rates would be consistent with sustainable growth and achieving the inflation target. Instead, they said that they will set future policy in order to reach those goals. The message we got was that the current policy stance may not be consistent with the Bank’s goals and that a rate cut could be possible in the months to come.

The minutes of that meeting added more credence to how we interpreted the meeting statement. While previous minutes revealed that members saw scenarios where interest rates could go up or down, with the probabilities equally balanced, these ones showed that members agreed that the likelihood of a hike was low. Policymakers also noted that if inflation does not move higher and the unemployment trends up, a rate cut would be appropriate. According to the ASX 30-day interbank cash rate futures implied yield curve, investors now expect a cut in October, and slowing inflation could prompt them to bring that timing forward, especially if the CPI rates fall below the Bank’s own projections.

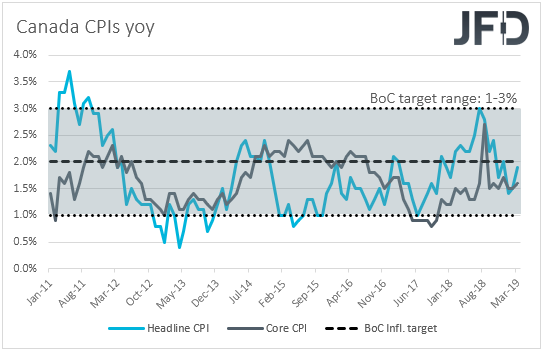

Later in the day, the spotlight is likely to turn to the BoC policy decision, where the forecast is for the Bank to keep interest rates unchanged at +1.75%. This will be one of the “bigger” meetings and thus, if rates are left untouched, the focus will turn to the meeting statement, the updated economic projections and the press conference by Governor Poloz.

When they last met, Canadian policymakers altered their interest-rate guidance. They removed the part saying that “the policy interest rate will need to rise over time into a neutral range to achieve the inflation target” and instead noted that “the outlook continues to warrant a policy interest rate that is below its neutral range”. They also highlighted the uncertainty surrounding the timing of future rate increases and said that they will be closely watching developments in household spending, oil markets, and global trade policy.

Latest inflation data showed that the headline CPI rate rose to +1.9% yoy from +1.5%, while the core one ticked up to +1.6% yoy from 1.5%. Most importantly, the median CPI rose from an upwardly revised +1.9% yoy to +2.0%, which is the BoC’s inflation aim. This may have been pleasant news for BoC policymakers but taking into account the disappointing BoC Business Survey for Q1, we believe that they are unlikely to appear confident with regards to future rate increases at this meeting. We believe that they may prefer to wait for more improvement in data, as well as in the global trade front, before they start examining whether the case for further hikes has strengthened again.

With regards to Wednesday’s economic indicators, Germany’s Ifo survey for April is scheduled to be released. Expectations are for the current assessment index to have declined slightly, to 103.6 from 103.8, while the business expectations one is anticipated to have risen to 96.0 from 95.6. This would drive the business climate index up to 99.9 from 99.6. The case for a declining current assessment index and a rise in the business expectations one is supported by the ZEW indices for the month, which moved in a similar fashion.

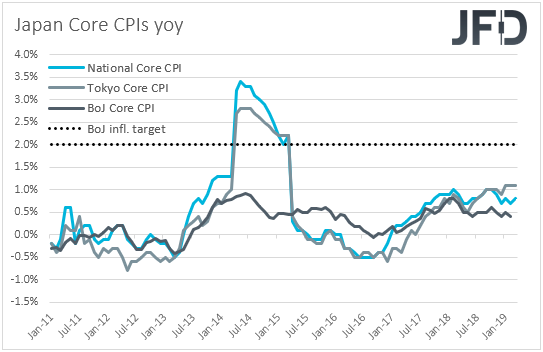

On Thursday, during the Asian morning, it’s the turn of the Bank of Japan to decide on monetary policy. At their previous meeting, BoJ officials kept their ultra-loose policy unchanged, maintaining short-term interest rates at -0.1% and the target of 10-year JGB yields around zero. They also repeated that that they intend to keep the current extremely low levels in interest rates for an extended period of time. That said, policymakers downgraded their economic assessment. They restated that the Japanese economy is expanding moderately, but they added that exports and production have been affected by the slowdown in overseas economies.

Latest inflation data showed that headline inflation rebounded to +0.5% yoy in March from +0.2%, while the core rate ticked up to +0.8% yoy from +0.7%. Although both rates moved in the desired direction, they remained well below the Bank’s objective of 2%. Even the Bank’s own core CPI for February ticked down to +0.4% yoy from +0.5%. We will get the March print of this rate on Tuesday, but we doubt that it could rebound to the Bank’s latest median forecast for the fiscal year of 2018, which is at +1.1%. Last week, Governor Kuroda said that there is still room for further monetary easing if needed, but he added that this is not necessary at this stage. Thus, we don’t expect the Bank to proceed with any policy changes at this gathering, but we see the case for downside revisions in the inflation forecasts.

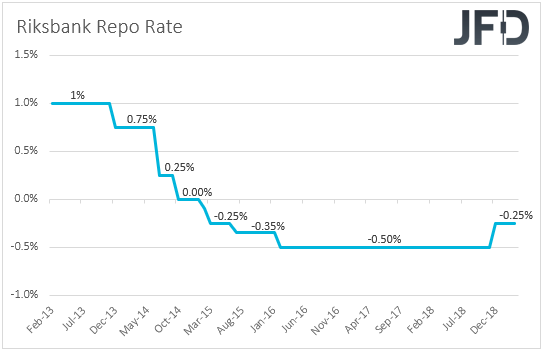

Later in the day, during the European session, the central bank torch will be passed to the Riksbank. When policymakers of the world’s oldest central bank last gathered, they decided to keep interest rates unchanged at -0.25%, reiterating that the next increase is likely to come during the second half of 2019.

The somewhat better than expected inflation data for March may have heightened market participants’ expectations on that front, but, given that in previous years the Riksbank has been usually following the footsteps of the ECB, last week’s disappointing Euro-area PMIs for April, may have prompted investors to scale back some hike bets. Yes, on March 5th, Riksbank Deputy Governor Cecilia Skingsley noted that the plan remains for higher rates later this year, but this was two days before the ECB gathering, at which Draghi and co. decided to abandon plans for a 2019 hike. Therefore, it would be interesting to see whether officials are still willing to bring Swedish rates to zero later this year, or not.

From the US, we get durable goods orders for March. The consensus is for the headline rate to have rebounded to +0.7% mom from -1.6%, while the core one is forecast to have ticked up to +0.2% mom from +0.1%.

Finally, on Friday, during the Asian morning, we get the usual end-of-month data dump from Japan. Getting the ball rolling with the employment numbers, the unemployment rate is expected to have risen to 2.4% in March from 2.3% in February, while the jobs-to-applications ratio is forecast to have ticked up to 1.64 from 1.63. The preliminary industrial production for the month is expected to show a slowdown to +0.1% mom from +0.7%, but retail sales are anticipated to have accelerated to +0.8% yoy from +0.6%. We also have the Tokyo CPIs for April. The headline rate is expected to have risen to +1.1% yoy from +0.9%, while the core one is forecast to have held steady at +1.1% yoy.

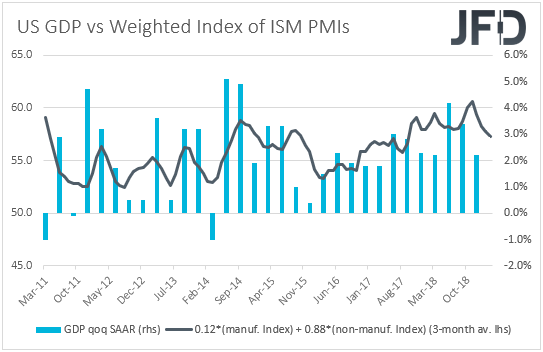

Later in the day, we get the first estimate of the US GDP for Q1. Ahead of last week’s retail sales for March, the forecast was pointing to further slowdown in economic activity, with the qoq SAAR rate expected to have declined to +1.8% from +2.2%. That said, the strong retail sails prints led to upside revisions in estimates and now the consensus is for the US economy to have grown 2.2%, the same pace as in the last three months of 2018. The Atlanta Fed GDPNow forecast was revised up to +2.8% after the retail sales data, but the New York Nowcast still points to a +1.4% growth rate. The case for a slowdown is also supported by the slide in the 3-month rolling average of a weighted composite index we built based on the ISM PMIs. So, having all that in mind, it’s hard to say where the risks of this release are tilted to.

Anything below the Fed’s latest projection for 2019, which is at +2.1%, may raise speculation that Fed officials could sound even more dovish at their upcoming gathering, which concludes on May 1st, and therefore, is likely heighten again speculation with regards to lower interest rates by year-end. On the other hand, a growth rate above +2.1% could ease further concerns with regards to the performance of the US economy and may allow investors to take some more rate-cut bets off the table. According to the Fed funds futures, market participants are 56% confident that the FOMC will not act this year, while there is a 44% for rates to be lower.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

76% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.