This week appears to be a relatively busy one, with three major central banks deciding on monetary policy. On Wednesday, we have the BoC, which we expect to taper further its QE purchases, while no Thursday, we have the BoJ and the ECB, which we expect to maintain a dovish language. Besides those central bank meetings, we also have earnings results from big tech firms. We start today with Facebook, we continue tomorrow with Microsoft and Google, while on Thursday, it will be the turn of Amazon and Apple.

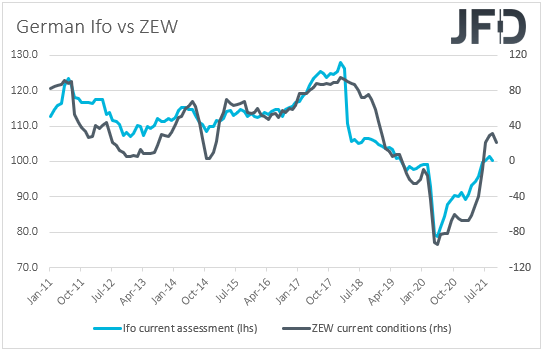

On Monday, the calendar appears relatively light, with the only release on the agenda worth mentioning being the German Ifo Survey for October. Both the current assessment and business expectations indices are forecast to have slid somewhat, something that will drive the business climate index down to 97.9 from 98.8. That said, bearing in mind that both the ZEW indices for the month fell by more than anticipated, we see the risks surrounding the Ifo survey as tilted to the downside. A negative surprise could confirm that the latest supply shortages have left their mark on Eurozone’s largest economy, and may weigh somewhat on the euro. In our view, any signs that the bloc’s economy has slowed somewhat recently will confirm the ECB’s stance to stay accommodative for longer than other major central banks, despite the rally in Euro-area inflation well above the Bank’s objective of 2%.

With no other top tier on the agenda, market participants may stay on the lookout for fresh developments surrounding the broader market sentiment. They could also pay extra attention to the earnings releases, with Facebook being the highlight of the day. The rest of the week is also packed with earnings, with Microsoft and Google reporting on Tuesday, and Amazon and Apple on Thursday. For the last couple of weeks, the broader market sentiment has been supported by better-than-expected earnings results, with several major indices around the globe breaking key technical resistance zones and inching closer to their all-time highs. A couple of them managed to even hit fresh records. Therefore, it would be interesting to see whether upbeat results from those tech giants will encourage investors to add to their risk exposures this week as well.

On Tuesday, the economic calendar remains light. The only relatively important data we get are the US Conference Board consumer confidence index for October and the new home sales for September. The CB index is expected to have slid fractionally, but new home sales are forecast to have increased somewhat.

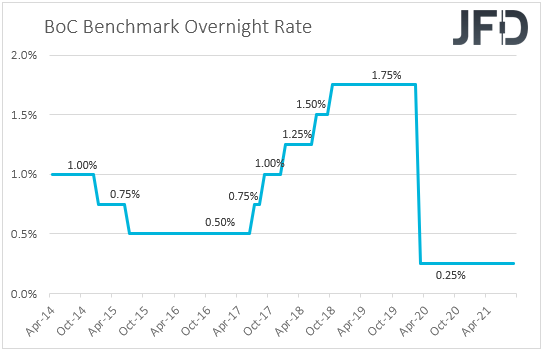

On Wednesday, the main event may be the BoC interest rate decision. At its prior gathering, the Bank left the door for further tapering wide open, despite some participants expecting a delay mainly due to the economic contraction in Q2. Even Governor Tiff Macklem said that he and his colleagues are moving closer to a time when continuing to add stimulus through QE won’t be necessary, adding more credence to the view that more policy withdrawal could be delivered at this gathering.

Since then, Canadian data have been coming in on the bright side, with the BoC’s Business Outlook Survey revealing that business sentiment hit a new record, the employment returning close to pre-crisis levels, and inflation accelerating even further in September. In our view, this makes the case for another tapering move this week nearly certain and suggests a relatively sanguine language in the statement accompanying the decision. With the QE tapering process expected to be over in December, anything suggesting that interest rates could start rising early next year could support further the Canadian dollar, which, recently, has been fueled by the rally in oil prices. Let’s not forget that Canada is the world’s fifth largest oil producing nation, while it holds the fourth place in terms of exports.

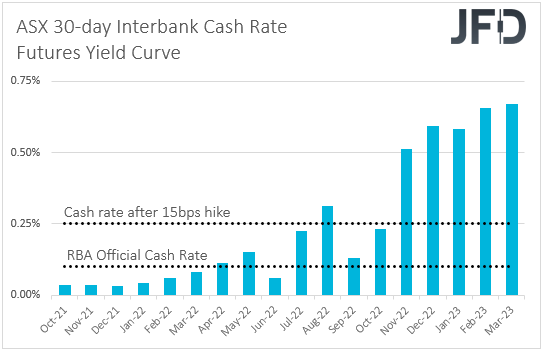

As for the rest of Wednesday’s data, during the Asian session, we have New Zealand’s trade balance for September and Australia’s CPIs for Q3. No forecast is available for New Zealand’s trade balance, while Australia’s CPI is expected to have slowed to +3.1% yoy from +3.8%. Both the trimmed mean and weighted mean rates are forecast to have inched slightly higher, but to have remained below the lower end of the RBA’s target range of 2-3%. This is likely to add credence to the RBA’s view that interest rates are unlikely to start rising before 2024, despite market participants seeing the official cash rate hitting 0.50% by the end of next year, at least according to the ASX 30-day Interbank Cash Rate Futures Yields Curve. As for the Aussie, slowing inflation could result in some selling, but bearing in mind that the currency is mostly driven by developments surrounding the broader market sentiment, we don’t expect a major trend reversal. As long as investors remain generally optimistic, this risk-linked currency could stay in an uptrend mode. Any CPI-related retreat could be just a temporary correction.

With regards to politics, in the UK, Chancellor Rishi Sunak will present the Autumn Budget, and he is expected to set fairly tight limits for most areas of day-to-day public spending, as he seeks to lower public debt after a record surge in borrowing during the COVID-19 pandemic. That said, according to late Saturday comments by finance ministry officials, he still plans a GBP 5bn program to fund health research and GBP 3bn of extra funding for further education. So, although he may appear stricter this time around, we doubt that this could be the turning point for the pound. Combined with a BoE ready to hike rates in order to battle inflation, a small support to the economy, which may have suffered from the latest supply shortages, may allow the British currency to continue trending north for a while more.

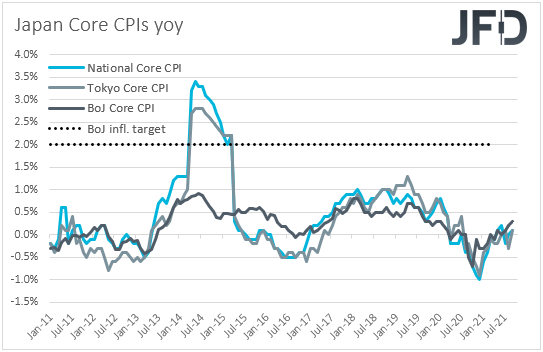

On Thursday, the central bank torch will be passed to the BoJ and the ECB. The first one will be the BoJ during the Asian morning, but with Japanese inflation near zero, well below the Bank’s target of 2%, we don’t expect any material changes, neither to the actual policy measures nor to the language in the accompanying statement. Once again, the yen may not react to the outcome and stay driven by the yield differentials between Japan and other major nations. With the global surge in inflation triggering a rally in global government bond yields, and the BoJ maintaining a ceiling to its own yields, we do see the case for the Japanese currency to continue underperforming its other major peers.

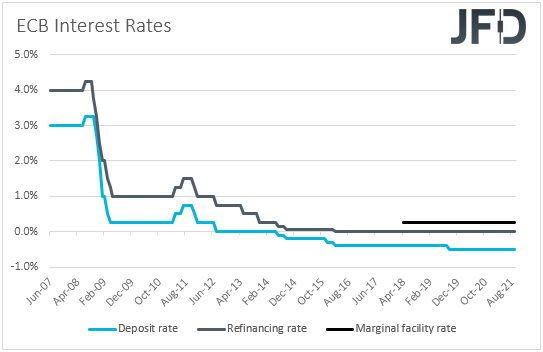

Now passing the ball to the ECB, we don’t expect any policy action from this Bank either. However, it will be interesting to see what policymakers have to say with regards to the continuous acceleration in inflation and the latest global supply shortages that have left their marks on the Eurozone economy.

At its previous meeting, the Bank announced a “moderately lower pace” of PEPP purchases, but President Lagarde made it clear that this was not a tapering move, and that when PEPP is over, they have all other tools available. In our view, this may have been a hint that when PEPP is over, they could compensate by buying more through other schemes, like the Asset Purchase Program (APP). So, with that in mind, we believe that they will stick to their dovish stance, noting once again that the surge in inflation will be transitory. We don’t expect them to risk sounding hawkish in the midst of economic risks, such as the aforementioned bottlenecks and the slowdown in China. Let’s not forget that China is Eurozone’s largest trading partner. Therefore, a dovish ECB is likely to bring the euro under renewed selling interest, even if Eurozone’s preliminary inflation, due out on Friday, accelerates further.

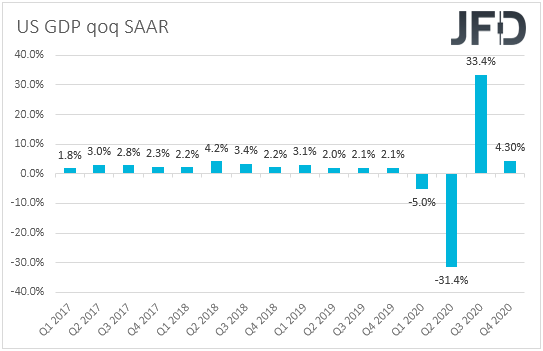

As for Thursday’s economic data, the most important one may be the 1st estimate of the US GDP for Q3. Expectations are for a slowdown to +2.8% qoq SAAR from +6.7%, but with the Atlanta Fed GDPNow model pointing to a +0.5% growth rate and the New York Nowcast model to a +3.8% rate, it’s hard to say where the risks of the actual forecast are tilted to. A negative surprise could raise some concerns as to whether the Fed could indeed start raising rates as early as next year and may weigh somewhat on the dollar. The opposite could be true if the actual number is better than the consensus, despite still indicating a slowdown.

Finally, on Friday, during the Asian morning, we have Japan’s employment data for September, the nation’s final industrial production for the same month, and the Tokyo CPIs for October. Later in the day, as we already noted, we get Eurozone’s preliminary CPIs for October, alongside the first estimate of the bloc’s GDP for Q3, but for which no forecast is available. In the US, personal income and spending for September are coming out, alongside the core PCE index for the month, while from Canada, we have the monthly GDP for August.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.90% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.